Exhibit 99.3

Management’s Discussion and Analysis

|

TABLE OF CONTENTS

|

|

| EXECUTIVE SUMMARY | 4 |

| 6 |

|

| 6 |

|

| BRANDS | 8 |

| 12 |

|

| 12 |

|

| 13 |

|

| 18 |

|

| 44 |

|

| RISK FACTORS | 53 |

| CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS | 59 |

2

Management’s Discussion and Analysis

INTRODUCTION

IM Cannabis Corp. (“IM Cannabis” or the “Company”) is a British Columbia company operating in the international

medical cannabis industry. The Company’s common shares (the “Common Shares”) trade under the ticker symbol “IMCC” on both the NASDAQ Capital Market (“NASDAQ”) and the

Canadian Securities Exchange (“CSE”) as of March 1, 2021 and November 5, 2019, respectively.

This Management’s Discussion and Analysis (“MD&A”) reports on the consolidated financial condition and operating results of IM Cannabis for the three

months ended March 31, 2024. Throughout this MD&A, unless otherwise specified, references to “we”, “us”, “our” or similar terms, as well as the “Company” and “IM Cannabis” refer to IM Cannabis Corp., together with its subsidiaries, on a

consolidated basis, and the “Group” refers to the Company, its subsidiaries, and Focus Medical Herbs Ltd.

This MD&A should be read in conjunction with the interim condensed consolidated financial statements of the Company and the notes thereto for the three months ended March 31, 2024 (the "Interim Financial Statements") and with the Company's audited annual consolidated financial statements and the notes thereto for the years ended December 31, 2023 and 2022 (the “Annual

Financial Statements”). References herein to “Q1 2024” and “Q1 2023” refer to the three months ended March 31, 2024 and March 31, 2023, respectively, and references to “2023” refer to the year ended December 31, 2023.

The Interim Financial Statements have been prepared by management in accordance with the International Financial Reporting Standards (“IFRS”) as issued by

the International Accounting Standards Board (“IASB”). IFRS requires management to make certain judgments, estimates and assumptions that affect the reported amount of assets and liabilities at the date of

the Interim Financial Statements and the amount of revenue and expenses incurred during the reporting period. The results of operations for the periods reflected herein are not necessarily indicative of results that may be expected for future

periods. The Interim Financial Statements for the three months ended March 31, 2024, include the accounts of the Group, which includes, among others, the following entities:

|

Legal Entity

|

Jurisdiction

|

Relationship with the Company

|

|

I.M.C. Holdings Ltd. (“IMC Holdings”)

|

Israel

|

Wholly-owned subsidiary

|

|

I.M.C. Pharma Ltd. (“IMC Pharma”)

|

Israel

|

Wholly-owned subsidiary of IMC Holdings

|

|

I.M.C. Farms Israel Ltd. (“IMC Farms”)

|

Israel

|

Wholly-owned subsidiary of IMC Holdings

|

|

Focus Medical Herbs Ltd. (“Focus”)

|

Israel

|

Subsidiary of IMC Holdings *

|

|

R.A. Yarok Pharm Ltd. (“Pharm Yarok”)

|

Israel

|

Wholly-owned subsidiary of IMC Holdings

|

|

Rosen High Way Ltd. (“Rosen High Way”)

|

Israel

|

Wholly-owned subsidiary of IMC Holdings

|

|

Revoly Trading and Marketing Ltd. dba Vironna Pharm (“Vironna”)

|

Israel

|

Subsidiary of IMC Holdings

|

|

Oranim Plus Pharm Ltd. (“Oranim Plus”)

|

Israel

|

Subsidiary of IMC Holdings

|

|

Trichome Financial Corp. (“Trichome”)**

|

Canada

|

Wholly-owned subsidiary

|

* Effective February 26, 2024, IMC Holdings exercised its option to acquire a 74% ownership stake in Focus.

3

Management’s Discussion and Analysis

In this MD&A, unless otherwise indicated, all references: (i) “Company Subsidiaries” are to the Israeli Subsidiaries and Adjupharm, (ii) “Israeli Operations” are to IMC Holdings and the Israeli Subsidiaries and (iii) “Trichome” are to Trichome Financial Corp. and its subsidiaries.

All dollar figures in this MD&A are expressed in thousands of Canadian Dollars ($), except per share data and unless otherwise noted. All references to “NIS” are to New Israeli Shekels. All

references to “€” or to “Euros” are to Euros. All references to “US$” or to “U.S. Dollars” are to United States Dollars. The Company’s shares, options, units and warrants are not expressed in thousands. Prices are not expressed in thousands.

NON-IFRS FINANCIAL MEASURES

Certain non-IFRS financial measures are referenced in this MD&A that do not have any standardized meaning under IFRS, including “Gross Margin”, “EBITDA” and “Adjusted EBITDA”. The Company

believes that these non-IFRS financial measures and operational performance measures, in addition to conventional measures prepared in accordance with IFRS, enable readers to evaluate the Company’s operating results, underlying performance and

prospects in a similar manner to the Company’s management. For a reconciliation of these non-IFRS financial measures to the most comparable IFRS financial measures, as applicable, see the “Metrics and Non-IFRS

Financial Measures” section of the MD&A.

NOTE REGARDING THE COMPANY’S ACCOUNTING PRACTICES

The Company complies with IFRS 10 to consolidate the financial results of Focus, a holder of an Israeli Medical Cannabis Agency (the “IMCA”) license which

allows it to import and supply cannabis products, on the basis of which IMC Holdings exercises “de facto control”. For a full explanation of the Company’s application of IFRS 10, see “Legal and Regulatory –

Restructuring” and “Legal and Regulatory – Risk Factors”. As of February 26, 2024, IMC Holdings holds 74% of Focus shares.

OVERVIEW – CURRENT OPERATIONS IN ISRAEL AND GERMANY

IM Cannabis is an international cannabis company that is currently focused on providing premium cannabis products to medical patients in Israel and Germany, two of the world’s largest federally

legal cannabis markets. Until recently, the Company was also actively servicing adult-use recreational consumers in Canada, however the Company has exited operations in Canada and considers these operations discontinued. The Company leverages a

transnational ecosystem powered by a unique data-driven approach and a globally sourced product supply chain. With an unwavering commitment to responsible growth and compliance with the strictest regulatory environments, the Company strives to

amplify its commercial and brand power to become a global high-quality cannabis player.

On November 7, 2022, the Company has exited its operations in Canada, deconsolidated Trichome pursuant to IFRS10 and announced that it is pivoting its focus and resources to achieve sustainable and

profitable growth in its highest value markets, Israel and Germany, while also commencing its exit from the Canadian cannabis market. The Canadian operations was wound-down under the Canadian Companies’ Creditors Arrangement Act (“CCAA”) under the supervision of the Ontario Superior Court of Justice (Commercial List) (the “Court”) (the “CCAA Proceedings”). The

Company has exited operations in Canada Pursuant to an Order of the Court made on April 6, 2023, in which the Court approved a share purchase agreement, selling certain of the Trichome and certain of Trichome's wholly owned subsidiaries

(collectively, the "Trichome Group") to a party that is not related to the Company.

4

Management’s Discussion and Analysis

In the context of the deconsolidation of the Canadian operations, there are no remaining liabilities to the Company or any of its consolidated subsidiaries related to the Canadian entities, except

tax obligation of $839 related to debt settlement with L5 Capital Inc. (“L5 Capital”). The CCAA Proceedings were solely in respect of the Trichome Group. As such, the Company’s other assets or subsidiaries,

including those in Israel and Germany, were not parties to the CCAA Proceedings. Court materials filed in connection with Trichome's CCAA Proceedings can be found at: https://www.ksvadvisory.com/insolvency-cases/case/trichome.

In Israel, the Company imports, distributes and sells cannabis to local medical patients by operating medical cannabis retail pharmacies, online platforms, distribution center and logistical hubs

operating through IMC Holdings’ subsidiaries and Focus, leveraging proprietary data and patient insights. The Company also preserves its existing proprietary genetics with third-party cultures facilities in Israel.

In Germany, the IM Cannabis ecosystem operates through Adjupharm, importing and distributing cannabis to pharmacies for patients, and acting as the Company’s entry point for potential Europe-wide

distribution in the future.

With the recent regulatory changes in both Israel and in Germany, the market dynamics are changing.

Germany legalized cannabis on April 1, 2024, facilitating the access to medical cannabis prescriptions for patients and legalizing non-profit social clubs starting July 1, 2024. The change in

regulation has already led to rapid expansion within the first month, driven by the number of new patients entering into the market, highlighting the importance of a stable supply chain able to respond quickly to increases in demand.

The proposed Israeli medical cannabis regulatory reform entered into vigor on April 1, 2024, as well. The reform is also expected to facilitate the access to medical cannabis for many new patient

groups. While the impact in Germany was reflected immediately in the market, the Israeli reform is starting slowly and will take time for the impact to be reflected in the market.

For further information regarding the Germany new legislation and the Israeli Reform, please see sections "Regulatory Framework in Israel" and " Regulatory Framework in Germany" below.

OUR GOAL – DRIVE PROFITABLE REVENUE GROWTH

Our primary goal is to sustainably increase revenue in each of our core markets, to accelerate our path to profitability and long-term shareholder value while actively managing costs and margins.

HOW WE PLAN TO ACHIEVE OUR GOAL – CORE STRATEGIES

Our strategy of sustainable and profitable growth consists of:

| • |

Continue building on the increasing demand and positive momentum in Israel and Germany, supported by strategic alliances with Canadian suppliers and a highly skilled sourcing team, to cement its leadership position in markets where the

Company operates.

|

| • |

Develop and execute a long-term growth plan in Germany, based on the strong sourcing infrastructure in Israel which is powered by advanced product knowledge and regulatory expertise establishing, in the Company’s view, a competitive

advantage following the April 1, 2024 legalization in Germany.

|

| • |

Properly position brands with respect to target-market, price, potency and quality, such as our IMC brand in Israel and Germany.

|

| • |

Strong focus on efficiencies and synergies as a global organization with domestic expertise in Israel and Germany.

|

| • |

High-quality, reliable supply to our customers and patients, leading to recurring sales.

|

| • |

Ongoing introduction of new Stock Keeping Unit (“SKUs”) to keep consumers and patients engaged.

|

5

Management’s Discussion and Analysis

RESULTS – REVENUE GROWTH IN Q1 2024

The Company operates in the Israeli and German medical cannabis markets. The Company was also actively servicing adult-use recreational consumers in Canada, however these operations were

discontinued and deconsolidated, effective November 7, 2022, pursuant to IFRS10. The Company announced that it is pivoting its focus and resources to achieve sustainable and profitable growth in its highest value markets, Israel, Germany and Europe

implementing a leaner organization strategy with the primary focus on achieving profitability in 2024.

Israel

In Israel, we continue to expand IMC brand recognition and supply the growing Israeli medical cannabis market with our branded products. The Company offers medical cannabis patients a rich variety

of high-end medical cannabis products through strategic alliances with Canadian suppliers supported by a highly skilled sourcing team. In addition to the benefits of the Group’s long-term presence in Israel, we believe that with our strong sourcing

infrastructure in Israel, and advanced product knowledge, regulatory expertise and strong commercial partnerships, the Company is well-positioned to address the ongoing needs and preferences of medical cannabis patients in Israel.

The Company is also operating in the retail segment. The Company, through IMC Holdings, holds three licensed pharmacies, each selling medical cannabis products to patients: (i) Oranim Plus, a

pharmacy in Jerusalem Israel, (ii) Vironna, a leading pharmacy in the Arab sector, and (iii) Pharm Yarok, the largest pharmacy in the Sharon plain area and the biggest call center in the country (Oranim Plus, Vironna, and Pharm Yarok collectively,

the “Israeli Pharmacies”).

On April 16, 2024, the Company announced that following a reconciliation between the parties regarding all remaining unpaid installments (i.e. NIS 5,363K or 1,930K CAD) by IMC Holdings, relating to

the Oranim Pharmacy Acquisition completed on March 28, 2022, the parties have mutually agreed to revoke the transaction. As a result, IMC Holdings Ltd. shares (51%) will be transferred back to the seller.

6

Management’s Discussion and Analysis

The Company has also acquired home-delivery services and an online retail footprint, operating under the name “Panaxia-to-the-Home”, which includes a

customer service center and an Israeli medical cannabis distribution licensed center (the “Panaxia Transaction”), from Panaxia Pharmaceutical Industries Israel Ltd. and Panaxia Logistics Ltd., part of the

Panaxia Labs Israel, Ltd. group of companies (collectively, “Panaxia”). On June 30, 2023, IMC Pharma, the entity responsible for operating the trading house that was acquired within the Panaxia Transaction,

ceased its operations at the aforementioned licensed center located in Lod, Israel. Consequently, the Company transitioned the operation that was conducted through IMC Pharma to third-party entities and to its own trading house currently being

operated by Rosen High Way and there are no material obligations remained open following closure of the trading house.

The operation in the retail segment in Israel positions IM Cannabis as a large distributor of medical cannabis in Israel. We are strategically focused on establishing and reinforcing a direct

connection with medical cannabis patients, providing direct access to IM Cannabis products, obtaining and leveraging market data and gaining a deeper understanding of consumer preferences. The operation of the Israeli Pharmacies allows the Company

to increase purchasing power with third-party product suppliers, offers potential synergies with our established call center and online operations, achieves higher margins on direct sales to patient and creates the opportunity for up-sales across a

growing range of products.

Germany

In Europe, the Company operates in Germany through Adjupharm, its German subsidiary and EU-GMP certified medical cannabis producer and distributor. We continue to lay our foundation in Germany,

which is currently the European market with the largest number of medical cannabis patients.1 Leveraging our global supply

chain, IM Cannabis continues to focus on growing its business in Germany to be well-positioned through brand recognition in preparation for future regulatory reforms.

Similar to Israel, the Company’s focus in Germany is to import dried cannabis from its supply partners, which we believe will satisfy the rapid growth in demand for high-THC cannabis across a

variety of strains and qualities. In addition, Adjupharm sells cannabis extracts to meet the existing demand in the German market.

In the Company’s view, the strong sourcing infrastructure in Israel, powered by advanced product knowledge and regulatory expertise, will establish a competitive advantage in Germany after the

April 1, 2024, legalization.. This is based on the premise that the German and Israeli markets share a number of common attributes such as robust commercial infrastructure, highly developed digital capabilities, favourable demographics and customer

preferences.

While the Company does not currently distribute products in other European countries, the Company intends to leverage the foundation established by Adjupharm, its state-of-the-art warehouse and

EU-GMP production facility in Germany (the “Logistics Center”), its vast knowledge in the cannabis market and costumers’ preferences and its network of distribution partners to expand into other jurisdictions

across the continent.

Adjupharm has an EU-GMP license that permits it to engage in additional production, cannabis testing and release activities. It allows Adjupharm to repackage bulk cannabis, to perform stability

studies and offer such services to third parties.

1 The European Cannabis Report – Edition 7 https://prohibitionpartners.com/2022/03/31/launching-today-the-european-cannabis-report-7th-edition/

and Visual Capitalist website, A Bird’s Eye View of the World’s Largest Cannabis Markets

https://www.visualcapitalist.com/sp/a-birds-eye-view-of-the-worlds-largest-cannabis-markets/

7

Management’s Discussion and Analysis

The IMC brand is well-known in the Israeli medical cannabis market, with reputable brands highly popular among Israeli consumers.

Israeli Medical Cannabis Business

The IMC brand has established its reputation in Israel for quality and consistency over the past 10 years and more recently with new high-end, ultra-premium strains that have made it to the

top-sellers list in pharmacies across the country.

The Group maintains a portfolio of strains sold under the IMC umbrella from which popular medical cannabis dried flowers and full-spectrum cannabis extracts are produced.

The IMC brand offers four different product lines, leading with the Craft Collection which offers the highest quality Canadian craft cannabis flower and has established IMC as the leader of the

super-premium segment in Israel.

The Craft Collection – The IMC brand’s premium product line with indoor-grown, hand-dried and hand-trimmed high-THC cannabis flowers. The Craft Collection

includes exotic and unique cannabis strains such as Cherry Crasher, Wedding Crasher, Peanut Butter MAC and Watermelon Zkittlez. During the year ended December 31, 2023, the Company was selling products under the Craft Collection, however, In Q4 the

Craft Collection was temporarily unavailable for sale by the Company and as a result, the Company did not generate any sales under the Craft Collection brand during that time. During Q1 2024 the Company relaunched sales under the Craft Collection.

|

The Top-Shelf Collection – IMC’s premium product line, which offers indoor-grown, high-THC cannabis flowers with strains

such as Lemon Rocket, Diesel Drift, Tropicana Gold, Lucy Dreamz, Santa Cruz, Or'enoz and Banjo. Inspired by the 1970’s cannabis culture in America, the Top-Shelf Collection targets the growing segment of medical patients who are cannabis

culture enthusiasts.

|

|

8

Management’s Discussion and Analysis

The Signature Collection – The IMC brand’s high-quality product line with greenhouse-grown or indoor grown, high-THC cannabis flowers. The Signature

Collection currently includes well known proprietary cannabis dried flowers such as Roma® Chemchew, Karmalada, Rockabye, Silver haze, all an indoor-grown flowers.

The Full Spectrum Extracts – The IMC brand’s full spectrum, strain-specific cannabis extracts, includes high-THC Roma®T20 oil.

As part of its recent rebranding the Company expanded its Roma® product portfolio to include also oils. IMC’s Roma® strain is a high-THC medical cannabis

flower that offers a therapeutic continuum and is known for its strength and longevity of effect.

9

Management’s Discussion and Analysis

| The WAGNERS™ brand launched in Israel in Q1 2022, with indoor-grown cannabis imported from Canada. The WAGNERS™ brand was the first international premium, indoor-grown brand introduced to the Israel cannabis market, at a competitive price point. The WAGNERS™ brand includes Cherry Jam re-launched in Q3 2023, Pink Bubba, Golden Ghost, Tiki Rain, Rain, Forest Crunch and Silverback#4. |

|

|

BLKMKT™, the Company’s second Canadian brand, super-premium product line with indoor-grown, hand-dried and hand-trimmed high-THC cannabis flowers.

The BLKMKT™ includes JEALOUSY, BACIO GLTO, PNPL P, PARK FIRE OG, UPSIDE DOWN C. In Q4 2023 the Company re-launched JEALOUSY and BACIO GLTO.

|

10

Management’s Discussion and Analysis

|

LOT420 brand launched in Israel in Q2 2023, with super-premium indoor-grown

cannabis imported from Canada with high-THC. The LOT420 includes ICY C, GLTO 33, Atomic APP and as of Q3 2023 also Glto 33 and Xeno. The Company ceased from

selling Atomic APP.

|

|

The PICO collection (minis)- Under the BLKMKT™ and LOT420 brands, the Company launched in 2023 a new type of products (small flowers), a super-premium

indoor-grown cannabis imported from Canada with high-THC. In Q4 2023 the Company re-launched PICO JEALOUSY #1 and PICO BACIO GLTO #4 T20i. In addition, the Company launched in Q4 2023 a new cannabis strain called Pico Upside Down #05 T20H.

For more information, see “Strategy in Detail – Brands – New Product Offerings” section of the MD&A.

11

Management’s Discussion and Analysis

German Medical Cannabis Business

In Germany, the company sells IMC-branded dried flower products and full spectrum extracts. The medical cannabis products are branded generically as IMC to increase the brand awareness and build

brand heritage among the German healthcare professionals.

After launching the first high THC strain in 2020, the portfolio has been carefully curated to include 5 high THC flowers, 1 high CBD flower and 3 full spectrum extracts with the goal of providing

German physicians and patients with a more complete portfolio.

Since 2023, the company has been number one in sales per SKU within the entire German flower market. The company is the sixth largest cannabis company in Germany. The Group’s competitive advantage

in Germany lies in its track record, experience and brand reputation in Israel, as well as the proprietary data supporting the potential effectiveness of medical cannabis for the treatment of a variety of conditions.

Between our various geographies, the strategy for new products varies given that each market is at a different stage of development with respect to regulatory regimes, patient and customer

preferences and adoption rates.

Israel

In Q1 2024, the Company launched new cannabis strains in Israel, namely "PURPLE RAIN T 15", "YA HEMI" and "BACIO GELATO" by BLKMKT™, "SUPER SATIVA" by TENZO

AVANT, "GELATO 33" by LOT420, "MOTORBRTH", "B F LMO" and "FLO OG" by SNDL.

Israel

The company is concentrating on leveraging its skilled sourcing team and strategic alliances with Canadian suppliers as well as the import of medical cannabis from its Canadian Facilities. The

Company continues to import cannabis products and supply medical cannabis to patients through licensed pharmacies. To supplement growing demand, the Company continue its relationships with third-party cultivation facilities in Israel for the

propagation and cultivation of the Company’s existing proprietary genetics and for the development of new products.

12

Management’s Discussion and Analysis

In addition, the Company is operating through its subsidiaries who obtained a license from the IMCA to, among others, import cannabis products and supply medical cannabis to patients.

Pursuant to the applicable Israeli cannabis regulations, following the import of medical cannabis, medical cannabis products are then packaged by contracted GMP licensed producers of medical

cannabis. The packaged medical cannabis products are then sold by the Group under the Company’s brands to local Israeli pharmacies directly or through contracted distributors.

Germany

The Company continues to expand its presence in the German market by forging partnerships with pharmacies and distributors across the country and developing Adjupharm and its Logistics Center as

the Company’s European hub. Adjupharm sources its supply of medical cannabis for the German market and from various EU-GMP certified European and Canadian suppliers. The Logistics Center is EU-GMP certified, upgrading Adjupharm’s production

technology and increasing its storage capacity to accommodate its anticipated growth. Adjupharm has a certification for primary repackaging, making it one of a handful of companies in Germany fully licenced to repack bulk.

Adjupharm currently holds wholesale, narcotics handling, manufacturing, procurement, storage, distribution, and import/export licenses granted to it by the applicable German regulatory authorities

(the “Adjupharm Licenses”).

KEY HIGHLIGHTS FOR THE FIRST QUARTER OF 2024

In the first quarter of 2024, the Company continued to focus on its efforts and resources on growth in the Israeli and German cannabis markets with a goal of reaching profitability during 2024. The

Company’s key highlights and events for the first quarter ended March 31, 2024, include:

Loan from ADI

On October 11, 2022, IMC Holdings entered into a loan agreement with A.D.I. Car Alarms Stereo Systems Ltd (“ADI” and the “ADI Agreement”),

to borrow a principal amount of NIS 10,500 thousand (approximately $4 million) at an annual interest of 15% (the “ADI Loan”), which is to be repaid within 12 months of the date of the ADI Agreement. The ADI

Loan is secured by a second rank land charge on the Logistics Center of Adjupharm. In addition, CEO and Director of the Company, provided a personal guarantee to ADI should the security not be sufficient to cover the repayment of the ADI Loan.

On October 25, 2023, IMC Holdings and ADI signed an amendment to the ADI Agreement, extending the loan period by an additional 3 months. During this extended period, the interest rate will be 15%,

with associated fees and commissions of 3% per annum for the application fee and an origination fee of 3% per annum.

13

Management’s Discussion and Analysis

On February 26, 2024, IMC Holdings and ADI signed an additional amendment to the ADI Agreement, extending the loan period until April 15, 2024, with the same terms as the first amendment, as

specified above.

IMC Holdings and ADI are negotiating a repayment plan of the ADI Loan.

Acquisition of Jerusalem’s Leading Medical Cannabis Pharmacy – Oranim Pharm

On January 12, 2024, the Company announced that the final sixth payment of the Oranim Pharmacy Acquisition and the reconciliation between the parties regarding the remaining transaction payments

are being rescheduled to April 15, 2024.

Through the transaction, completed on March 28, 2022, IMC Holdings Ltd. acquired 51% of the rights in Oranim Pharm Partnership through the acquisition of Oranim Plus. As part of the transaction

consideration, NIS 5,363K or 1,930K CAD were supposed to be paid in six installments throughout 2023, with the final payment due February 15, 2024.

Through a new amendment signed January 10, 2024, the sixth (6) payment as well as the reconciliation between the parties regarding all remaining unpaid installments has been postponed to April 15,

2024. All six installments (that remain unpaid) will incur a 15% interest charge. Failure to meet the remaining payments will result in the transfer of IMC Holdings Ltd. shares (51%) back to the seller, along with the revocation of the transaction.

On April 16, 2024, the Company announced that further to the news release dated January 12, 2024, the Company has decided not to make remaining installment payments installments (i.e. NIS

5,873K including interest or 2,154K CAD) by IMC Holdings, and as such will transfer the 51% shares held by IMC Holdings back to the seller.

NASDAQ Compliance Notice

On January 31, 2024, the Company received an extension a 180-calendar day extension, until July 29, 2024, from Nasdaq staff to regain compliance with the Minimum Share Price Listing Requirements

(the “Extension”). As at the date of this MD&A, the Company continues to monitor the closing bid price of its Common Shares and plans to pursue available options to regain compliance with the Minimum

Share Price Listing Requirement, including potentially pursuing a reverse stock split. If the Company authorizes a reverse stock split, it will plan to effectuate the split no later than ten business days prior to the end of the Extension.

Potential Reverse Merger with Kadimastem

On February 28, 2024, the Company announced that it has entered into a non-binding term sheet dated February 13, 2024, as amended (the “Term Sheet”), and a

Loan Agreement (as defined below) with Holding Company (as defined below), with Israel-based Kadimastem Ltd a clinical cell therapy public company traded on the Tel Aviv Stock Exchange under the symbol (TASE:KDST) (“Kadimastem”), whereby the parties will complete a business combination that will constitute a reverse merger into the Company by Kadimastem (the “Proposed Transaction”).

The Proposed Transaction will be effected by way of a plan of arrangement involving a newly created wholly-owned subsidiary of IMC and Kadimastem (the “Arrangement”).

The resulting issuer that will exist upon completion of the Proposed Transaction (the “Resulting Issuer”) will change its business from medical cannabis to biotechnology and, at the closing of the Proposed

Transactions (the "Closing"), Kadimastem shareholders will hold 88% of the common shares of the Resulting Issuer (the “Resulting Issuer Shares”) and the shareholders of the Company will hold 12% of the

Resulting Issuer Share. Parties may agree, in the Definitive Agreement, on a different structure of equity in lieu of the warrants (as described below) with a similar result. The Proposed Transaction is an arm’s length transaction.

14

Management’s Discussion and Analysis

Prior to Closing, IMC's existing medical cannabis operation and other current activities in Israel and Germany (the "Legacy Business") will be restructured

(the “Spin-Out”) as a contingent value right (the "CVR"). The CVR will entitle the holders thereof to receive net cash, equity, or other net value upon the sale of the

Legacy Business following the Closing, subject to the terms of the Loan Agreement.

To facilitate the sale of the Legacy Business, a special committee of IMC's Board was formed, which will oversee the potential sale in collaboration with legal and financial advisors.

The Legacy Business will be made available for potential sale to a third party for a period of up to 12 months from Closing (the "Record Date"). After the

Record Date, any remaining Legacy Business in the CVR will be offered for sale through a tender process, subject to the terms of the best offer. The proceeds from the sale of the Legacy Business will be utilized to settle debts and distribute the

remaining balance, if any, to CVR holders.

As a condition of Closing, Kadimastem will have approximately $5 million in gross funds, at Closing including capital raised concurrently with the completion of the Proposed Transaction from

existing shareholders and additional investors.

In addition to the foregoing, subject to compliance with applicable law, the Company shall grant shareholders of the Company as of Closing, with warrant(s) equal their pro rata portion, of 2% of

the Resulting Issuer’s issued and outstanding common share capital (the "IMC Shares") prior to the Closing Date (in the aggregate), with an exercise price per share equal to the 10 day volume-weighted average

price of the Resulting Issuer’s shares calculated on the NASDAQ Capital Market (“Nasdaq”), ending 2 trading days prior to Closing, the warrants will be for a period of 24 months following Closing.

In accordance with the terms of the Proposed Transaction, the holders of the issued and outstanding shares in the capital of Kadimastem (the “Kadimastem Shares”)

will be issued such number of IMC Shares in exchange for every one (1) Kadimastem Share held immediately prior to the completion of the Proposed Transaction that reflects the ratio outlined above (the “Exchange

Ratio”). Outstanding convertible securities of Kadimastem (the “Kadimastem Convertible Securities”) will be treated through customary mechanics as shall be determined in the definitive agreement,

which may include, the assumption of the Kadimastem Convertible Securities by IMC subject to customary adjustments to reflect the Exchange Ratio and exercise price.

Pursuant to the terms of the Term Sheet, a loan agreement dated February 28, 2024 (the "Loan Agreement") was entered between IMC Holdings Ltd. a wholly-owned

subsidiary of IMC (the "Holding Company") and Kadimastem. Pursuant to the Loan Agreement, Kadimastem will provide a loan of up to US$650,000 to the Holding Company, funded in two installments: US$300,000 upon

signing the Loan Agreement and US$350,000 upon the execution of the definitive agreement regarding the Proposed Transaction (the "Loan").

15

Management’s Discussion and Analysis

The Loan accrues interest at a rate of 9.00% per annum, compounding annually and is secured by the following collaterals and guarantees: (a) 10% of the proceeds derived from any operation sale

under the CVR (“Charged Rights”), limited to the outstanding Loan Amount and expenses according to the Loan Agreement, accordingly Holding Company may, at its sole discretion, to record a second-ranked fixed charge over the Charged Rights or,

alternatively, in case the existing pledges over the Charged Rights at the date of signing this Loan Agreement are subsequently discharged or removed, then the Borrower shall promptly record a first-ranking fixed charge over the Charged Assets with

all applicable public records; provided that Holding Company shall not impose any new lien, mortgage, charge or pledge over the Charged Rights that did not exist on the date hereof, or any other liens, subject to customary exclusions; (b) the

Holding Company shall use its best efforts to record a first-ranking fixed charge over the assets of its subsidiary, A.R Yarok Pharm Ltd, in due course when applicable and as deemed appropriate; and (c) a personal guarantee by Mr. Oren Shuster,

IMC’s CEO.

Prior to the completion of the Proposed Transaction, IMC will call a meeting of its shareholders for the purpose of approving, among other matters:

| • |

approve the Proposed Transaction;

|

| • |

approve the Spin-Out;

|

| • |

a change of name of the Company as directed by Kadimastem and acceptable to the applicable regulatory authorities effective upon Closing; and

|

| • |

reconstitution of the Company’s Board.

|

Upon closing of the Proposed Transaction, all of IMC’s current directors and executive officers will resign and the board of directors of the Resulting Issuer will, subject to the approval of

governing regulatory bodies, consist of nominees of Kadimastem. All of the executive officers shall be replaced by nominees of Kadimastem, all in a manner that complies with the requirements of governing regulatory bodies and applicable securities

and corporate laws.

Details of insiders and proposed directors and officers of the Resulting Issuer will be disclosed in a further news release.

The completion of the Proposed Transaction is subject to a number of conditions, including but not limited to the following:

| • |

the execution of a definitive agreement;

|

| • |

completion of mutually satisfactory due diligence;

|

| • |

completion of the Share Consolidation; and

|

| • |

receipt of all required regulatory, corporate and third party approvals, including approvals by governing regulatory bodies, the shareholders of IMC and Kadimastem, applicable Israeli governmental authorities, and the fulfilment of all

applicable regulatory requirements and conditions necessary to complete the Proposed Transaction.

|

The parties are committed to seeking a successful completion of the Proposed Transaction as soon as practicable, but there can be no absolute certainty that the Proposed Transaction will take place.

Option to re-acquire the sold interest in Focus

On November 30, 2023, IMC Holdings acted to exercise its option to purchase the 74% interest in Focus held by Oren Shuster and Rafael Gabay by submitting a request to the IMCA which approved the transaction on February

25, 2024. As of February 26, 2024, IMC Holdings holds 74% of Focus shares.

16

Management’s Discussion and Analysis

SUBSEQUENT EVENTS

The new Israeli cannabis regulation

On April 1, 2024, the Company announced the implementation of the medical cannabis regulatory reform in Israel starting as of April 1, 2024.

The reform, announced by the Israeli ministry of health on August 7, 2023, underwent a three-month delay due to the Israel-Hamas war following its initial announcement (the "Reform").

The Reform will be implemented in phases, as approved, and announced by the Israeli Ministry of Health. The key aspects of the initial phase, commencing today, April 1st, are as follows:

1. Change in the prescription process: patients with a wide range of diseases and medical conditions from Oncology to Parkinsons will no longer be required to obtain a license to receive medical

cannabis. Patients will receive a prescription similar to those for other prescription medications. Pain and PTSD are not included in the Reform yet.

2. Medical cannabis will now be prescribed through the HMO's, Israel's public healthcare system: until the Reform, cannabis could not be prescribed through the HMO's which cover the majority of the

Israeli population.

3. The number of prescribing physicians is expected to increase: as of today, HMO physicians, who are dully trained and certified within their field of expertise, can prescribe medical cannabis as

a first line treatment, as opposed to a last resort, based on medical discretion for the approved indications. 4. The cost for prescription is anticipated to be reduced: the Ministry of Health limited the cost for a medical cannabis prescription.

For the full report published by the Ministry of Health see (in Hebrew)- https://www.health.gov.il/hozer/mmk152_2016.pdf

Trademark Licensing Agreement

On April 4, 2024, the Company and Avant Brands Inc. (TSX: AVNT) (OTCQX: AVTBF) (FRA: 1BU0) ("Avant") a leading producer of innovative cannabis products,

jointly announce the signing of an international trademark licensing agreement (the "Licensing Agreement") granting Adjupharm the exclusive right to launch the BLK MKT™ brand in the German medical cannabis

market. The Licensing Agreement constitutes another major milestone with respect to the relationship between the two cannabis companies.

Under the terms of the Trademark License Agreement, Avant's subsidiary will grant Adjupharm the license to utilize Avant's BLK MKT TM cannabis brand for use on their medical cannabis products. All

such products will contain cannabis cultivated exclusively by Avant and subsequently exported to Germany. The collaboration between the two companies anticipates a positive outcome in the emerging German medical cannabis market, especially

following the recent legalization by the government on April 1, 2024.

The Licensing Agreement signals the Company's commitment to implementing a premium strategy in Germany as well as in Israel and acts as another step to establish Avant's position in the

ultra-premium segment in Israel and Germany. The Company and Avant have had a productive partnership so far, combining Avant's premium cannabis products with the Company's sales, marketing and distribution expertise in Israel. Both companies

believe the Licensing Agreement will enhance the companies' capabilities to meet the demands of the German market.

Avant's three largest cultivation facilities all hold ICANN-GAP and GACP certifications; thus, Avant is positioned to potentially distribute its premium cannabis flower into international markets.

Adjupharm is the 6th largest distributor of medical cannabis flowers in Germany and is number 1 in sales per SKU, growing +180% in 20232.

2 Insight Health December 2023

17

Management’s Discussion and Analysis

Partnership with Flora Growth

On April 9, 2024, the Company announced that it has entered, through its subsidiary, a strategic distribution agreement with Vessel Brand Inc, a subsidiary of Flora Growth Corp. ("Flora"), a global consumer-packaged goods leader and pharmaceutical distributor, headquartered in Carlsbad, CA.

The Company's brands are well known in the premium Israeli cannabis market, facilitating the import and wholesale of premium medical cannabis through retail pharmacies, online platform, and

distribution center. Vessel is a premium cannabis accessories brand with a wide range of products.

Short-term Loan Agreement

On October 17, 2023, IMC Holdings entered into a short-term loan agreement with a non-financial institute in the amount of NIS 1,800 thousand (approximately $610). Such loan bear interest at an

annual rate of 18% and mature six months from the date of issuance along with the associated fees and commissions of 4% per annum for application fee and an origination fee of 4% per annum. On April 17, 2024, IMC Holdings and the lender signed an

amendment to extend the loan period until April 18, 2025, with an annual interest rate of 17% with no additional fees associated as in the initial loan period.

Loan Agreement

On April 17, 2024 R.A Yarok Pharm entered into a loan agreement with a non-financial institute in the amount of NIS 3,000 thousand (approximately $1,082). Such loan bear interest at an annual rate

of 15% and mature 12 months from the date of issuance (the "Loan"). The Loan is secured by the following collaterals and guarantees: (a) a first-ranking floating charge over the assets of A.R Yarok Pharm (b)

a first-ranking fixed charge over the holdings (23.3%) of its subsidiary, IMC Holdings, of Xinteza; (c) a personal guarantee by Mr. Oren Shuster, IMC’s CEO and (D) a guarantee by the Company.

FINANCIAL HIGHLIGHTS

Below is the analysis of the changes that occurred for the three months ended March 31, 2024, with further commentary provided below.

18

Management’s Discussion and Analysis

|

For the three months

ended March 31

|

For the year ended

December 31

|

|||||||||||

|

2024

|

2023(1)

|

2023

|

||||||||||

|

Net Revenues

|

$

|

12,063

|

$

|

12,529

|

$

|

48,804

|

||||||

|

Gross profit before fair value impacts in cost of sales

|

$

|

1,789

|

$

|

3,243

|

$

|

10,830

|

||||||

|

Gross margin before fair value impacts in cost of sales (%)

|

15

|

%

|

26

|

%

|

22

|

%

|

||||||

|

Operating Loss

|

$

|

(5,630

|

)

|

$

|

(3,617

|

)

|

$

|

(12,792

|

)

|

|||

|

Net loss

|

$

|

(6,020

|

)

|

$

|

(866

|

)

|

$

|

(10,228

|

)

|

|||

|

Loss per share attributable to equity holders of the Company – Basic (in CAD)

|

$

|

(0.42

|

)

|

$

|

(0.05

|

)

|

$

|

(0.74

|

)

|

|||

|

Loss per share attributable to equity holders of the Company - Diluted (in CAD)

|

$

|

(0.42

|

)

|

$

|

(0.05

|

)

|

$

|

(0.74

|

)

|

|||

|

For the three months

ended March 31

|

For the year ended

December 31

|

|||||||||||

|

2024

|

2023

|

2023

|

||||||||||

|

Average net selling price of dried flower (per Gram)

|

$

|

5.68

|

$

|

6.59

|

$

|

5.14

|

||||||

|

Quantity of dried flower sold (in Kilograms)

|

1,873

|

1,842

|

8,609

|

|||||||||

Notes:

|

1.

|

The figures disclosed here for the three months ended March 31, 2023, encompass updates and adjustments made during Q2 2023 to the Company’s previously filed unaudited interim financial statements. The

adjustments and updates were immaterial. .

|

The Overview of Financial Performance includes reference to “Gross Margin”, which is a non-IFRS financial measure that the Company defines as the difference between revenue and cost of revenues

divided by revenue (expressed as a percentage), prior to the effect of a fair value adjustment for inventory and biological assets. For more information on non-IFRS financial measures, see the “Non-IFRS Financial

Measures” and “Metrics and Non-IFRS Financial Measures” sections of the MD&A.

OPERATIONAL RESULTS

In each of the markets in which the Company operates, the Company must navigate evolving customer and patient trends in order to continue to be competitive with other suppliers of medical cannabis

products.

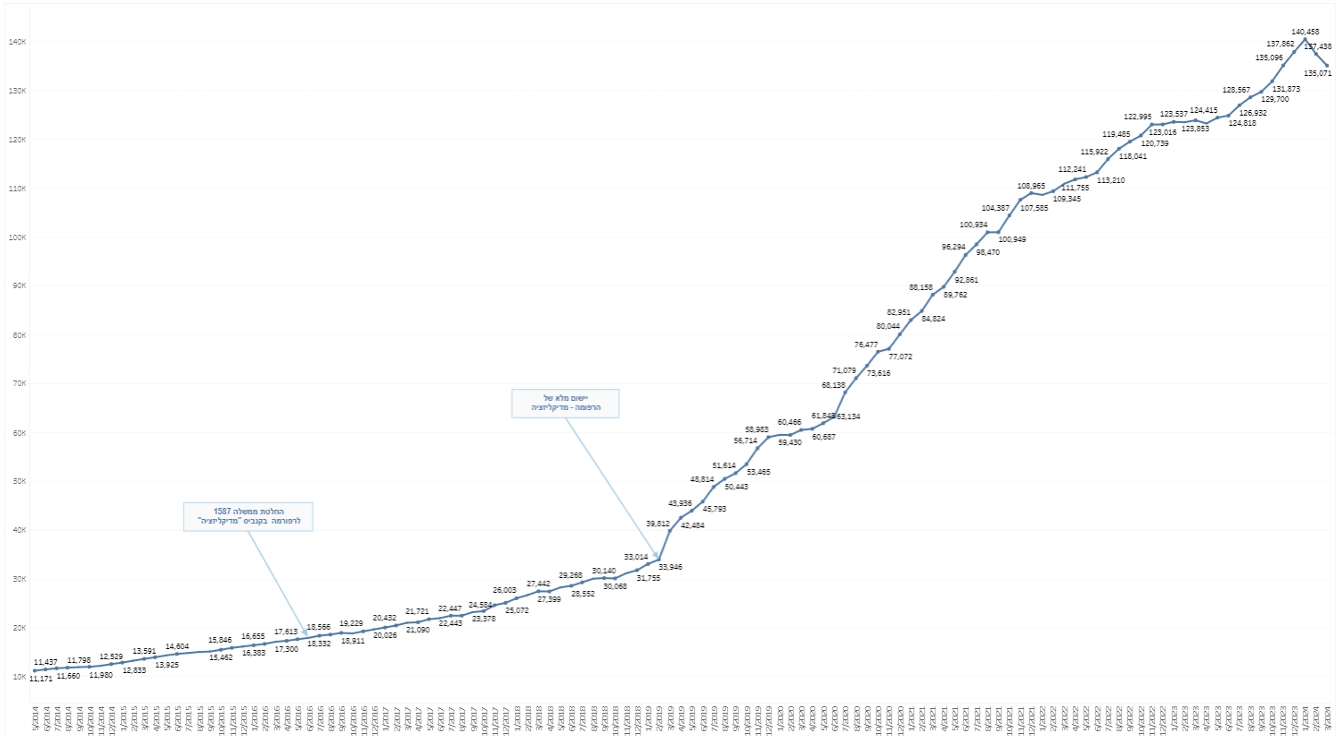

The Company believes that there are several key factors creating tailwinds to facilitate further industry growth. In Israel, the number of licensed medical patients currently stands at 135,071 as

of March 2024. This figure is expected to grow in the coming years and may further benefit from regulatory change liberalizing the cannabis market in Israel IM Cannabis is a large distributor of medical cannabis in Israel. As the Israeli cannabis

market has become increasingly competitive, the ability to import premium cannabis from Canada is a key determinant of the Company’s success in Israel.

The German medical cannabis market has been slower over the past few years to develop mainly due to the difficulty in medical patients accessing prescriptions and insurance reimbursements. Starting

Year 2024 after the legalization was officially approved by the Bundestag (Germany Parliament) on March 1st 2024, The Company which has already seen an increase in the

number of patients paying out-of-pocket for medical cannabis products in Germany during the past few years, is expecting a change which will lead to increase in the market. Starting April 2024, the Company through its subsidiary Adjupharm is

experiencing a significant increase in demands in Germany for its products.

19

Management’s Discussion and Analysis

REVENUES AND GROSS MARGINS

REVENUES

The revenues of the Group are primarily generated from sales of medical cannabis products to customers in Israel and Germany. The reportable geographical segments in which the Company operates are Israel and Germany.

For the three months ended March 31:

|

Israel

|

Germany

|

Adjustments

|

Total

|

|||||||||||||||||||||||||||||

|

2024

|

2023(*)

|

2024

|

2023(*)

|

2024

|

2023(*)

|

2024

|

2023(*)

|

|||||||||||||||||||||||||

|

Revenues

|

$

|

10,911

|

$

|

11,437

|

$

|

1,152

|

$

|

1,092

|

$

|

-

|

$

|

-

|

$

|

12,063

|

$

|

12,529

|

||||||||||||||||

|

Segment loss

|

$

|

(4,508

|

)

|

$

|

(1,618

|

)

|

$

|

(316

|

)

|

$

|

(557

|

)

|

$

|

-

|

$

|

-

|

$

|

(4,824

|

)

|

$

|

(2,175

|

)

|

||||||||||

|

Unallocated corporate expenses

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

(806

|

)

|

$

|

(1,442

|

)

|

$

|

(806

|

)

|

$

|

(1,442

|

)

|

||||||||||||

|

Total operating (loss)

|

$

|

(4,508

|

)

|

$

|

(1,618

|

)

|

$

|

(316

|

)

|

$

|

(557

|

)

|

$

|

(806

|

)

|

$

|

(1,442

|

)

|

$

|

(5,630

|

)

|

$

|

(3,617

|

)

|

||||||||

|

Depreciation, amortization

|

$

|

655

|

$

|

780

|

$

|

25

|

$

|

29

|

$

|

-

|

$

|

-

|

$

|

680

|

$

|

809

|

||||||||||||||||

* See Note 1 under “Review of Financial Performance – Financial Highlights” section of the MD&A.

The consolidated revenues of the Group for the three months ended March 31, 2024, were attributed to the sale of medical cannabis products in Israel and Germany.

| ● |

Revenues for the three months ended March 31, 2024 and 2023 were $12,063 and $12,529, respectively, representing a decrease of $466 or 4%. The decrease is mainly due to Exchange rate effect of about $0.2 and decrease in Avg. price per

sale due to increased competition.

|

| ● |

Revenues from the Israeli operation were attributed to the sale of medical cannabis through the Company’s agreement with Focus Medical and the revenues from the Israeli Pharmacies the Company owns, mostly from cannabis products.

|

| ● |

In Germany, Company revenues were attributed to the sale of medical cannabis through Adjupharm.

|

| ● |

Total dried flower sold for the three months ended March 31, 2024, was 1,873kg at an average selling price of $5.68 per gram compared to 1,842kg for the same period in 2023 at an average selling price of

$6.59 per gram, mainly attributed to the inventory life cycle, discounts given and increased competition in the segment.

|

| ● |

Cost of Revenues

|

Cost of revenues is comprised of purchase of raw materials and finished goods, import costs, production costs, product laboratory testing, shipping and salary expenses. Inventory

is later expensed to the cost of sales when sold. Direct production costs are expensed through the cost of sales.

The cost of revenues for the three months ended March 31, 2024 and 2023 were $10,274 and $9,286, respectively, representing an increase of $988 or 11%. This is mainly due

to clearing of old inventory of approximately $140K and accrued for slow inventory of approximately $500K.

20

Management’s Discussion and Analysis

GROSS PROFIT

Gross profit for the three months ended March 31, 2024, and 2023 was $1,779 and $2,904, respectively, representing a decrease of $1,125 or 39%.

Gross profit included losses from unrealized changes in fair value of biological assets and realized fair value adjustments on inventory sold of $(10) and $(339) for the three months ended March

31, 2024, and 2023, respectively.

EXPENSES

GENERAL AND ADMINISTRATIVE

General and administrative expenses for the three months ended March 31, 2024, and 2023 were $2,332 and $3,175, respectively, representing a decrease of $843 or 27%.

The decrease in the general and administrative expense is attributable mainly to the restructuring plan published March 8, 2023, which aimed for reorganization of the company's management and

operations to strengthen its focus on core activities and drive efficiencies to realize sustainable profitability. The Company reduced its workforce in Israel across all functions. The general and administrative expenses are comprised mainly from

salaries to employees in the amount of $572, professional fees in the amount of $699, depreciation and amortization in the amount of $121 and insurance costs in the amount of $326.

PROVISION FOR REVOKING ORANIM TRANSACTION

Due to the revocation of the Oranim agreement on April 16, 2024, the Company recorded $2,753 other operating expenses for losses expected on Q2 2024 due to the clearing of Oranim assets and

liabilities from the consolidated balances. The total expense for the 3 months ended March 31, 2024 is $2,753.

SELLING AND MARKETING

Selling and marketing expenses for the three months ended March 31, 2024, and 2023 were $2,292 and $2,805, respectively, representing a decrease of $513 or 18%. The decrease in the selling and marketing expenses was

due mainly to decrease salaries to employees of $429 due to the saving plan executed in H2 2023.

SHARE-BASED COMPENSATION

Share-based compensation expense for the three months ended March 31, 2024, and 2023 was $32 and $258, respectively, representing a decrease $226 or 88%. The decrease was mainly attributed to the cancellation of

incentive stock options (“Options”) held by employees who no longer worked for the Company.

FINANCING

Financing income (expense) net for the three months ended March 31, 2024, and 2023 was $(501) and $2,735, respectively, representing a decrease of $3,236 or 118% in the financing income.

21

Management’s Discussion and Analysis

NET INCOME/LOSS

Net loss for the three months ended March 31, 2024, and 2023 was $6,020 and $866, respectively, representing a net loss decrease of $5,154 or 595%. The net loss decrease related to factors impacting net income

described above.

NET INCOME (LOSS) PER SHARE BASIC AND DILUTED

Basic loss per share is calculated by dividing the net profit attributable to holders of Common Shares by the weighted average number of Common Shares outstanding during the period. Diluted profit per Common Share is

calculated by adjusting the earnings and number of Common Shares for the effects of dilutive warrants and other potentially dilutive securities. The weighted average number of Common Shares used as the denominator in calculating diluted profit

per Common Share excludes unissued Common Shares related to Options as they are antidilutive. Basic and diluted Income (Loss) per Common Share for the three months ended March 31, 2024, and 2023 were $(0.42) and $(0.05) per Common Share,

respectively.

TOTAL ASSETS

Total assets as at March 31, 2024 were $41,109, compared to $48,813 as at December 31, 2023, representing a decrease of $7,704 or 16%. This decrease was primarily due to the reduction of cash and cash equivalents in

the amount of $765 and inventory reduction of $2,075, decrease of $1,145 in trade receivables and $2,653 in Goodwill.

TOTAL LIABILITIES

Total liabilities at March 31, 2024, were $32,765, compared to $35,113 at December 31, 2023, representing a decrease of $2,348 or 7%. The decrease was mainly due to a decrease in PUT option

liability in the amount of $730, a decrease in advances from customers in the amount of $711 and a decrease in accrued expenses of $558.

LIQUIDITY AND CAPITAL RESOURCES

For the three months ended March 31, 2024, the Company recorded revenues of $12,063.

The Company can face liquidity fluctuations from time to time, resulting from delays in sales and slow inventory movements.

In January 2022, Focus entered into a revolving credit facility with an Israeli bank, Bank Mizrahi (the “Mizrahi Facility”). The Mizrahi Facility is

guaranteed by Focus assets. Advances from the Mizrahi Facility will be used for working capital needs. The Mizrahi Facility has a total commitment of up to NIS 15 million (approximately $6,000) and has a one-year term for on-going needs and 6

months term for imports and purchases needs. The Mizrahi Facility is renewable upon mutual agreement by the parties. The borrowing base is available for draw at any time throughout the Mizrahi Facility and is subject to several covenants to be

measured on a quarterly basis (the “Mizrahi Facility Covenants”).

The Mizrahi Facility bears interest at the Israeli Prime interest rate plus 1.5%.

On May 17, 2023, the Company and Bank Mizrahi entered to new credit facility with total commitment of up to NIS 10,000 (approximately $3,600) (the “New Mizrahi

Facility”). The New Mizrahi Facility consists of NIS 5,000 credit line and NIS 5,000 loan to be settled with 24 monthly installments from May 17, 2023. This loan bears interest at the Israeli Prime interest rate plus 2.9%. As of Marcg 31,

2024 Focus has drawn down $3,111 in respect of the new Mizrahi facility (comprised of approx. $1,845 credit line and $1,266 loan). The New Credit facility is also subject to several covenants to be measured on a quarterly basis which are not met as

of March 31, 2024, therefore the loan is classified as short-term loan.

22

Management’s Discussion and Analysis

The Company's CEO and director, provided to the bank a personal guarantee in the amount of the outstanding borrowed amount, allowing the New Mizrahi Facility to remain effective.

As of March 31, 2024, the Group's cash and cash equivalents totaled $1,048 and the Group's working capital deficit (current assets less current liabilities) amounted to ($10,518). In the three months ended March 31,

2024, the Group had an operating loss of ($5,630) and negative cash flows from continuing operating activities of ($662).

As of March 31, 2024, the Group’s financial liabilities consisted of accounts payable which have contractual maturity dates within one year. The Group manages its liquidity risk by reviewing its

capital requirements on an ongoing basis. Based on the Group’s working capital position on March 31, 2024, management considers liquidity risk to be high.

As of March 31, 2024, the Group has identified the following liquidity risks related to financial liabilities (undiscounted):

|

Less than one year

|

1 to 5 years

|

6 to 10 years

|

> 10 years

|

|||||||||||||

|

Contractual Obligations

|

$

|

12,446

|

$

|

1,222

|

-

|

-

|

||||||||||

The maturity profile of the Company’s other financial liabilities (trade payables, other account payable and accrued expenses, and warrants) as of March 31, 2024, are less than one year.

|

Payments Due by Period

|

||||||||||||||||||||

|

Contractual Obligations

|

Total

|

Less than one year

|

1 to 3 years

|

4 to 5 years

|

After 5 years

|

|||||||||||||||

|

Debt

|

$

|

12,342

|

$

|

11,941

|

$

|

401

|

$

|

-

|

$

|

-

|

||||||||||

|

Finance Lease Obligations

|

$

|

1,326

|

$

|

505

|

$

|

778

|

$

|

43

|

$

|

-

|

||||||||||

|

Total Contractual Obligations

|

$

|

13,668

|

$

|

12,446

|

$

|

1,179

|

$

|

43

|

$

|

-

|

||||||||||

The Group’s current operating budget includes various assumptions concerning the level and timing of cash receipts from sales and cash outflows for operating expenses and capital expenditures, including cost saving

plans. In 2023 The Company’s board of directors approved a cost saving plan, to allow the Company to continue its operations and meet its cash obligations. The cost saving plan entailed reducing costs through efficiencies and synergies primarily

involving the following measures: discontinuing loss-making activities, reducing payroll and headcount, reduction in compensation paid to key management personnel (including layoffs of key executives), operational efficiencies and reduced capital

expenditures. These actions are expected to result in cost savings in 2024 and the company will continue its efforts for efficiency operations.

Despite the cost savings plan and restructuring as described above, the projected cash flows for 2024 indicates that it is uncertain that the Group will generate sufficient funds to continue its

operations and meet its obligations as they become due. The Group continues to evaluate additional sources of capital and financing. However, there is no assurance that additional capital and or financing will be available to the Group, and even if

available, whether it will be on terms acceptable to the Group or in amounts required.

23

Management’s Discussion and Analysis

These conditions raise substantial doubt about the Company’s ability to continue as a going concern. The consolidated financial statements do not include any adjustments relating to the

recoverability and classification of assets or liabilities that might be necessary should the Company be unable to continue as a going concern. The Interim Financial Statements have been prepared on the basis of accounting principles applicable to

a going concern, which assumes that the Company will continue in operation for the foreseeable future and will be able to realize its assets and discharge its liabilities in the normal course of operations. The Interim Financial Statements do not

include any adjustments to the amounts and classification of assets and liabilities that would be necessary should the Company be unable to continue as a going concern. Such adjustments could be material.

SHARE CAPITAL

The Company’s authorized share capital consists of an unlimited number of Common Shares without par value 13,394,136 of which were issued and outstanding as at the date hereof. The Common Shares

confer upon their holders the right to participate in the general meeting with each Common Share carrying the right to one vote on all matters. The Common Shares also allow holders to receive dividends if and when declared and to participate in the

distribution of surplus assets in the case of liquidation of the Company.

OTHER SECURITIES

As of March 31, 2024, the Company also has the following outstanding securities which are convertible into, or exercisable or exchangeable for, voting or equity securities of the Company: 270,452

Options, 18,261 2019 Broker Compensation Options (as defined below), 294,348 Offered Warrants (as defined below) and 5,769,611 2023 LIFE Offering Warrants.

FINANCIAL BACKGROUND

On October 11, 2019, the Company completed the Reverse Takeover Transaction, effected by way of a “triangular merger” between the Company, IMC Holdings and a wholly owned subsidiary of the Company

pursuant to Israeli statutory law.

In connection with the Reverse Takeover Transaction, the Company completed a private placement offering of 19,460,527 subscription receipts (each a “Subscription

Receipt”) on a pre-2021 Share Consolidation basis (as defined below) of a wholly owned subsidiary of the Company at a price of $1.05 per Subscription Receipt for aggregate gross proceeds of $20,433. Upon completion of the Reverse Takeover

Transaction, each Subscription Receipt was exchanged for one unit comprised of one (1) common share and one-half of one (1/2) warrant (each whole warrant, a “2019 Listed Warrant”). Each 2019 Listed Warrant

was exercisable for one Common Share at an exercise price of $1.30 until October 11, 2021. A total of 9,730,258 2019 Listed Warrants were issued and listed for trading on the CSE under the ticker “IMCC.WT”. The 2019 Listed Warrants expired on

October 11, 2021.

The Company also issued to the agent who acted on its behalf in connection with the Reverse Takeover Transaction, a total of 1,199,326 2019 Broker Compensation Options (the “2019 Broker Compensation Options”). Following the 2021 Share Consolidation, the 2019 Broker Compensation Options were adjusted to require four 2019 Broker Compensation Options to be exercised for one underlying

unit at an adjusted exercise price of $4.20, with each unit exercisable into one Common Share and one-half of one Common Share purchase warrant (the “2019 Unlisted Warrants”). Following the 2021 Share

Consolidation, the 2019 Unlisted Warrants were adjusted to require four 2019 Unlisted Warrants to be exercised for one Common Share at an adjusted exercise price of $5.20. The 2019 Broker Compensation Options and the 2019 Unlisted Warrants expired

on August 2022.

24

Management’s Discussion and Analysis

On February 12, 2021, the Company consolidated all of its issued and outstanding Common Shares on the basis of one (1) post-consolidation Common Share for each four (4) pre-consolidation Common

Shares (the “2021 Share Consolidation”) to meet the NASDAQ minimum share price requirement.

On November 17, 2022, the Company completed a second share consolidation (the “2022 Share Consolidation”) by consolidating all its issued and outstanding

Common Shares on the basis of one (1) post-Consolidation Common Share for each ten (10) pre-Consolidation Common Shares.

On May 7, 2021, the Company completed an offering (the “2021 Offering”) for a total of 6,086,956 Common Shares and 3,043,478 Common Share purchase warrants

(the “2021 Offered Warrants”). Following the 2022 Share Consolidation, the 2021 Offered Warrant were adjusted to require the (10) 2021 Offered Warrant to be exercised for one (1) Common Share at an adjusted

exercise price of US$72 for a term of 5 years from the date of closing of the 2021 Offering.

The Company also issued a total of 182,609 broker compensation options (the “2021 Broker Compensation Options”) to the agents who acted on its behalf in

connection with the 2021 Offering. Following the 2022 Share Consolidation, the 2021 Broker Compensation Option were adjusted to require the (10) 2021 Broker Compensation Options for one (1) Common Share at an adjusted exercise price of US$66.1, at

any time following November 5, 2021 until November 5, 2024. There are 182,609 2021 Broker Compensation Options outstanding.

As of March 31, 2024, and December 31, 2023, there were 6,063,960 and 6,063,960 warrants outstanding, respectively, re-measured by the Company, using the Black-Scholes pricing model, in the amount of $137 and $38,

respectively. For the three months ended March 31, 2024, and 2023, the Company recognized a revaluation gain (loss) in the consolidated statement of profit or loss and other comprehensive income, of $(99) and $3,371, respectively, in which the

unrealized gain is included in finance income (expense).

25

Management’s Discussion and Analysis

OPERATING, FINANCING AND INVESTING ACTIVITIES

The following table highlights the Company’s cash flow activities for the three months ended March 31, 2024 and 2023:

|

For the three months ended March 31,

|

For the year ended December 31,

|

|||||||||||

|

Net cash provided by (used in):

|

2024

|

2023

|

2023

|

|||||||||

|

Operating activities

|

$

|

(662

|

)

|

$

|

(6,061

|

)

|

$

|

(8,075

|

)

|

|||

|

Investing activities

|

$

|

(2

|

)

|

$

|

(467

|

)

|

$

|

(1,182

|

)

|

|||

|

Financing activities

|

$

|

(852

|

)

|

$

|

6,557

|

$

|

9,417

|

|||||

|

Effect of foreign exchange

|

$

|

751

|

$

|

(1,059

|

)

|

$

|

(796

|

)

|

||||

|

Increase (Decrease) in cash

|

$

|

(765

|

)

|

$

|

(1,030

|

)

|

$

|

(636

|

)

|

|||

Operating activities used cash of $662 and $6,061 for the three months ended March 31, 2024, and 2023, respectively. This variance is primarily due to business activities of the Company including corporate expenses

for salaries, professional fees, and marketing expenses in Israel and, Germany.

Investing activities used cash of $2 and $467 for the three months ended March 31, 2024, and 2023, respectively. Decrease derived mainly from a decrease in purchase of property, plant and equipment in the amount of

$409.

Financing activities used cash of $852 and provided cash of $6,557 for the three months ended March 31, 2024, and 2023, respectively. This decrease is primarily due to the reduction of proceeds from issuance of

warrants and share capital by $7,203 and $649 respectively and set-off by an increase in proceeds from discounted checks in the amount of $2,581 and an increase of repayment of bank loan and credit facilities in the amount of $1,810.

SELECTED INTERIM INFORMATION – CONTINUING OPERATIONS

|

For the year ended

|

December 31,

2023 |

December 31,

2022

|

December 31,

2021

|

|||||||||

|

Revenues

|

$

|

48,804

|

$

|

54,335

|

$

|

34,053

|

||||||

|

Net Loss

|

$

|

(10,228

|

)

|

$

|

(24,922

|

)

|

$

|

(664

|

)

|

|||

|

Basic net income (Loss) per share:

|

$

|

(0.74

|

)

|

$

|

(3.13

|

)

|

$

|

0.02

|

||||

|

Diluted net income (Loss) per share:

|

$

|

(0.74

|

)

|

$

|

(3.81

|

)

|

$

|

(3.62

|

)

|

|||

|

Total assets

|

$

|

48,813

|

$

|

60,676

|

$

|

129,066

|

||||||

|

Total non-current liabilities

|

$

|

2,305

|

$

|

3,060

|

$

|

21,354

|

||||||

26

Management’s Discussion and Analysis

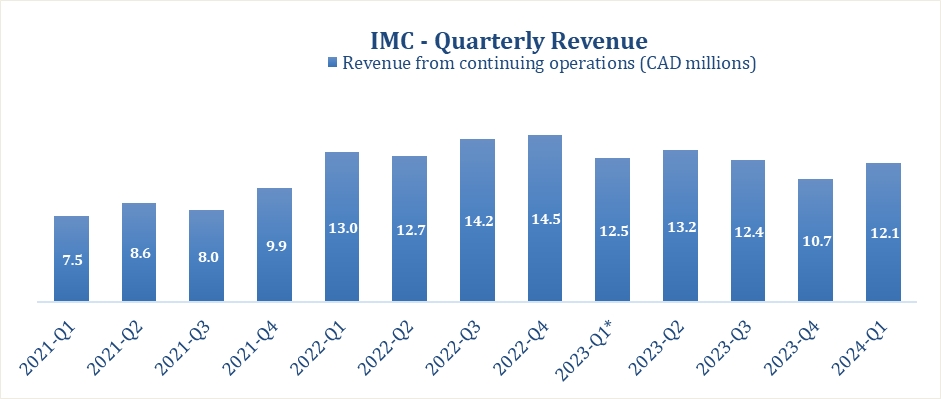

SUMMARY OF QUARTERLY RESULTS

|

For the three months ended

|

March 31, 2024

|

December 31, 2023

|

September 30, 2023

|

June 30, 2023

|

||||||||||||

|

Revenues

|

$

|

12,063

|

$

|

10,698

|

$

|

12,370

|

$

|

13,207

|

||||||||

|

Net Loss

|

$

|

(6,020

|

)

|

$

|

(3,520

|

)

|

$

|

(2,136

|

)

|

$ |

(3,706

|

)

|

||||

|

Basic net income (Loss) per share:

|

$

|

(0.42

|

)

|

$

|

(0.25

|

)

|

$

|

(0.16

|

)

|

$

|

(0.26

|

)

|

||||

|

Diluted net loss per share:

|

$

|

(0.42

|

)

|

$

|

(0.25

|

)

|

$

|

(0.16

|

)

|

$

|

(0.26

|

)

|

||||

|

For the three months ended

|

March 31, 2023 (1)

|

December 31, 2022

|

September 30, 2022

|

June 30, 2022

|

||||||||||||

|

Revenues

|

$

|

12,529

|

$

|

14,461

|

$

|

14,170

|

$

|

12,703

|

||||||||

|

Net income (Loss)

|

$

|

(866

|

)

|

$

|

(9,650

|

)

|

$

|

(4,532

|

)

|

$

|

(3,736

|

)

|

||||

|

Basic net income (Loss) per share:

|

$

|

(0.05

|

)

|

$

|

(1.32

|

)

|

$

|

(0.06

|

)

|

$

|

(0.27

|

)

|

||||

|

Diluted net income (Loss) per share:

|

$

|

(0.05

|

)

|

$

|

(1.28

|

)

|

$

|

(0.06

|

)

|

$

|

(0.30

|

)

|

||||

Note 1 - The figures disclosed here for the three months ended March 31, 2023, encompass updates and adjustments made during Q2 2023 to the Company’s previously filed unaudited interim financial

statements. The adjustments and updates were immaterial..

METRICS AND NON-IFRS FINANCIAL MEASURES

This MD&A makes reference to “Gross Margin”, “EBITDA”, and “Adjusted EBITDA”. These financial measures are not recognized measures under IFRS and do not have a standardized meaning prescribed

by IFRS and are therefore unlikely to be comparable to similar measures presented by other companies. Rather, these measures are provided as additional information to complement those IFRS measures by providing further understanding of our results

of operations from management’s perspective. Accordingly, these measures should neither be considered in isolation nor as a substitute for analysis of our financial information reported under IFRS.

Management defines Gross Margin as the difference between revenue and cost of goods sold divided by revenue (expressed as a percentage), prior to the effect of a fair value adjustment for inventory

and biological assets. Management defines EBITDA as income earned or lost from operations, as reported, before interest, tax, depreciation and amortization. Adjusted EBITDA is defined as EBITDA, adjusted by removing other non-recurring or non-cash

items, including the unrealized change in fair value of biological assets, realized fair value adjustments on inventory sold in the period, share-based compensation expenses, and revaluation adjustments of financial assets and liabilities measured

on a fair value basis. Management believes that Adjusted EBITDA is a useful financial metric to assess its operating performance on a cash adjusted basis before the impact of non-recurring or non-cash items. The closest IFRS metric to EBITDA and

Adjusted EBITDA is “operating loss”.

27

Management’s Discussion and Analysis

The non-IFRS financial measures can provide investors with supplemental measures of our operating performance and thus highlight trends in our core business that may not otherwise be apparent when

relying solely on IFRS measures. We also believe that securities analysts, investors and other interested parties frequently use non-IFRS financial measures in the evaluation of issuers. These financial measures are metrics that have been adjusted

from the IFRS statements in an effort to provide readers with a normalized metric in making comparisons more meaningful across the cannabis industry. However, other companies in our industry may calculate this measure differently, limiting their

usefulness as comparative measures.