Exhibit 15.4

Item 5. Operating and Financial Review and Prospects

| A. |

Operating Results

|

The following discussion and analysis of IM Cannabis Corp.’s (the “Company”) results of operations and financial condition should be read in conjunction with the Company’s consolidated financial

statements and the related notes included elsewhere in the Annual Report on Form 20-F for the year ended December 31, 2025 (the “Annual Report”), of which this exhibit constitutes a part. The discussion below contains forward-looking statements

that are based upon the Company’s current expectations and are subject to uncertainty and changes in circumstances. Actual results may differ materially from these expectations due to inaccurate assumptions and known or unknown risks and

uncertainties, including those identified in “Cautionary Note Regarding Forward-Looking Statements” and “Item 3.D. Risk Factors” elsewhere in this Annual Report. The Company’s discussion and analysis for the year ended December 31, 2024 compared to

the year ended December 31, 2023 can be found in the Company’s Annual Report on Form 20-F for the fiscal year ended December 31, 2024, filed with the Securities and Exchange Commission on March 31, 2025.

Overview

Current Operations in Israel and Germany

The Company operates in the medical cannabis sector in Israel and Germany. The Company’s activities in these jurisdictions include sourcing, importation, distribution and sale of medical cannabis

products in compliance with applicable regulatory requirements.

Israel

In Israel, the Company operates through IMC Holdings and its consolidated subsidiary Focus, which holds an IMCA license permitting the importation and supply of medical cannabis products. The

Company’s operations in Israel primarily consist of importing medical cannabis products from approved suppliers and distributing those products to pharmacies and patients in accordance with Israeli regulations. The Company does not currently operate

large-scale cultivation facilities in Israel and relies primarily on imported products that meet applicable quality and regulatory standards.

The Company’s Israeli operations include brand management, regulatory compliance, logistics coordination and relationships with pharmacies and prescribing physicians. Revenue in Israel is generated

from the sale of medical cannabis products to pharmacies and other authorized distributors.

Germany

In Germany, the Company operates through its German subsidiaries, which are authorized to import and distribute medical cannabis products under applicable German and European Union regulations. The

Company’s German operations focus on sourcing EU-GMP compliant medical cannabis products from approved suppliers and distributing such products to licensed pharmacies throughout Germany.

The German market is regulated by the BfArM, and the Company’s import volumes are subject to regulatory requirements, including compliance with applicable pharmaceutical standards. Revenue in Germany is generated from

the sale of imported medical cannabis products to pharmacies and other authorized customers.

The Company’s operations in both jurisdictions are subject to evolving regulatory frameworks, including changes in prescribing practices, import authorizations, product specifications and

distribution models, which may affect its revenues, margins and operating results.

Results of Operations

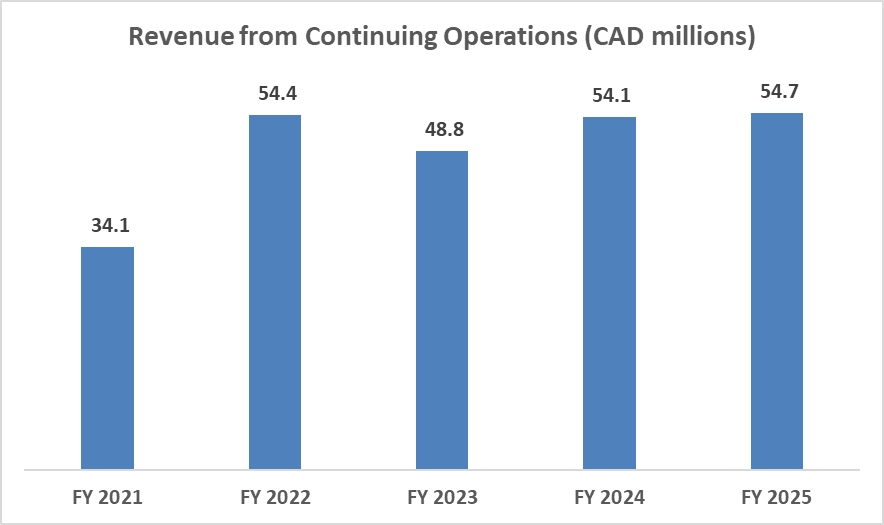

The following chart presents the Company’s annual revenue from continuing operations for the fiscal years indicated (in millions of Canadian dollars):

As reflected above, revenue fluctuated during the fiscal years presented. In 2025, the annual revenue reflects changes compared to 2024, primarily driven by product mix, pricing, regulatory developments and inventory

levels.

Components of Operating Results

Revenues

The Company’s revenues are primarily generated from sales of medical cannabis products to customers in Israel and Germany. The reportable geographic segments in which the Company operates are Israel

and Germany.

Revenue from the Company’s Israeli operations is primarily derived from the sale of medical cannabis products through its subsidiaries, including sales through pharmacies that the Company owns or

controls.

Revenue from the Company’s German operations is primarily derived from the sale and distribution of medical cannabis products through Adjupharm GmbH.

Cost of Revenues

Cost of revenues consists primarily of the purchase of finished goods and raw materials, importation costs, production and processing costs, laboratory testing, logistics and shipping expenses, and

certain personnel costs directly attributable to production and distribution activities. Inventory costs are recognized in cost of revenues upon sale of the related products.

General and Administrative Expenses

The Company’s general and administrative expenses consist primarily of salaries and related personnel expenses for executive, finance, regulatory and administrative personnel, professional fees

(including legal and accounting), insurance, public company expenses, rent and office expenses.

Sales and Marketing Expenses

The Company’s sales and marketing expenses consist primarily of salaries and commissions for sales personnel, promotional and marketing activities.

Other Operating Expenses

The Company’s other operating expenses consist primarily of non-recurring items, such as goodwill and intangible asset impairment, deconsolidation of a subsidiary and other non-recurring operational

items.

Financial Income and Expenses

Financial income and expenses consist primarily of interest expense on debt and convertible instruments, changes in fair value of financial instruments, foreign exchange gains and losses, and other

financing-related costs.

Results of Operations - Comparison

The following table summarizes the Company’s results of operations for the periods presented.

|

|

For the Year Ended

December 31,

|

|||||||

|

CAD in thousands

|

2025

|

2024

|

||||||

|

Revenue

|

$

|

54,731

|

$

|

54,031

|

||||

|

Gross profit

|

$

|

9,686

|

$

|

8,451

|

||||

|

Gross margin (%)

|

18

|

%

|

16

|

%

|

||||

|

Operating income (Loss)

|

$

|

(11,587

|

)

|

$

|

(10,234

|

)

|

||

|

Net income (Loss)

|

$

|

(11,750

|

)

|

$

|

(11,771

|

)

|

||

|

Loss per share attributable to equity holders of the Company - Basic (in CAD) *

|

$

|

(2.67

|

)

|

$

|

(4.51

|

)

|

||

|

Loss per share attributable to equity holders of the Company - Diluted (in CAD) *

|

$

|

(2.67

|

)

|

$

|

(4.51

|

)

|

||

Revenues

The following table summarizes the Company’s revenues for the periods presented. The period-to-period comparison of results is not necessarily indicative of results for future periods.

|

CAD in thousands

|

Israel

|

Germany

|

Adjustments

|

Total

|

||||||||||||||||||||||||||||

|

For the Year Ended

December 31,

|

For the Year Ended

December 31,

|

For the Year Ended

December 31,

|

For the Year Ended

December 31,

|

|||||||||||||||||||||||||||||

|

2025

|

2024

|

2025

|

2024

|

2025

|

2024

|

2025

|

2024

|

|||||||||||||||||||||||||

|

Revenue

|

$

|

18,383

|

$

|

38,523

|

$

|

36,348

|

$

|

15,508

|

$

|

-

|

$

|

-

|

$

|

54,731

|

$

|

54,031

|

||||||||||||||||

|

Segment income (loss)

|

$

|

(6,839

|

)

|

$

|

(9,314

|

)

|

$

|

(1,674

|

)

|

$

|

942

|

$

|

-

|

$

|

-

|

$

|

(8,513

|

)

|

$

|

(8,372

|

)

|

|||||||||||

|

Unallocated corporate expenses

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

(3,074

|

)

|

$

|

(1,862

|

)

|

$

|

(3,074

|

)

|

$

|

(1,862

|

)

|

||||||||||||

|

Total operating income (loss)

|

$

|

(6,839

|

)

|

$

|

(9,314

|

)

|

$

|

(1,674

|

)

|

$

|

942

|

$

|

(3,074

|

)

|

$

|

(1,862

|

)

|

$

|

(11,587

|

)

|

$

|

(10,234

|

)

|

|||||||||

|

Depreciation, amortization and impairment

|

$

|

7,175

|

$

|

2,014

|

$

|

1,168

|

$

|

170

|

$ | - |

$

|

-

|

$

|

8,343

|

$

|

2,184

|

||||||||||||||||

The Company’s consolidated revenues for the year ended December 31, 2025, were attributed mostly to the sale of medical cannabis products in Israel and Germany. Revenue in Germany reflects demand

trends, product availability and import volumes during the periods presented.

Revenues for the years ended December 31, 2025, and 2024 were $54,731 and $54,031, respectively, representing an increase of $700 or 1%. The increase was primarily attributable to an increase in

revenue in Germany of $20,840 following legalization, and a decrease of $20,140 in revenue in Israel, reflecting variations in product mix, pricing and volume as well as reduced imports driven in part by cash flow constraints, which negatively

impacted sales volumes.

Cost of Revenues and Gross Profit

The cost of revenues for the years ended December 31, 2025, and 2024 were $45,045 and $45,580, respectively, representing a decrease of $535 or 1%. The decrease was primarily attributable to changes

in material costs, inventory write-down in 2024, partially offset by changes in logistics and other production-related expenses.

Gross profit for the years ended December 31, 2025, and 2024 was $9,686 and $8,451, respectively, representing an increase of $1,235 or 15%. The increase was primarily due to an inventory write-off

of $3,878 in 2024, attributable to old material.

Iron Swords War and other conflicts’ Effect on Gross Profit

On October 7, 2023, the State of Israel was attacked by the terrorist organization Hamas, and as a result, the State of Israel declared a state of war and a large-scale mobilization of reserves (the

“War”). At the same time, a front of fighting also developed in the northern border against the terrorist organization Hezbollah, which led to extensive evacuation of residents. The War is an exceptional event with security and economic implications

whose extent and outcomes are unpredictable. In response to the War, the State of Israel has taken significant steps to ensure the security of its residents, which have a considerable impact on economic and business activities in the country. The

events of the War have led to a reduction in business activity in the economy and a significant slowdown in economic activity, affecting the business operations of entities in various circles of influence, among others due to the closure of factories

in the south and north of the country, damage to infrastructure, long-term mobilization of reservists, and more. Potential fluctuations in commodity prices, foreign exchange rates, availability of materials, availability of manpower, local services,

and difficulties in accessing local resources have affected and are expected to continue to affect entities whose main operations are in Israel. In addition, the state of warfare also affects the activities of entities that rely on foreign workers or

on workers recruited for the purposes of the fighting, international trade, foreign companies in Israel, civil aviation, and more. As a result, the War has significant implications for the economy and imposes a considerable burden on the continuation

of business activity and the functional and operational continuity of the entities.

In November 2024, a ceasefire was reached with the terrorist organization Hezbollah in the north of the country, but the War continued in other areas.

On June 13, 2025, the State of Israel launched operation “Rising Lion” against military targets in Iran, with a focus on the Iranian nuclear project. As a result, a state of emergency was declared in Israel, causing

repercussions and restrictions on the Israeli economy, which included, inter alia, partial or complete closure of businesses, restrictions on gatherings in workplaces and in the education system, as well as a decrease in workforce due to reserve

enlistment and a reduction in number of foreign workers. During the operation, a targeted American strike was carried out against Iran, after which, on June 24, 2025, a ceasefire was reached between the parties.

Following the above, in October 2025 a ceasefire agreement was signed with terrorist organization Hamas in Gaza and as a result, the fighting subsided on most fronts.

Subsequent to reported date, on February 28, 2026, Israel and the United States launched a joint attack against Iranian government targets, following which Iran responded with missile fire towards Israel and other

countries in the region. As a result of the aforementioned, the Israeli government declared a special situation on the home front across the entire country, including restrictions on gatherings and a reduction in economic activity except for

essential workplaces until March 26, 2026.

The Company's management is continuously monitoring the developments regarding the War and is acting in accordance with the guidelines of the various authorities. The Company suffered a negative impact from the War

commencing the last quarter of 2023. The Company has experienced damage to its ability to function, affecting various aspects, including employees, supplies, imports, sales, and more.

Expenses

General and Administrative Expenses

General and administrative expenses for the years ended December 31, 2025, and 2024 were $9,516 and $8,018, respectively, representing an increase of $1,498 or 19%.

The increase in general and administrative expenses for the year ended December 31, 2025 was primarily attributable to (i) an increase in salaries and related expenses of $220 ($2,438 in 2025

compared to $2,218 in 2024), (ii) an increase in professional fees of $1,449 ($3,471 in 2025 compared to $2,022 in 2024), (iii) an increase in other expenses of $147 ($2,055 in 2025 compared to $1,907 in 2024), (iv) a decrease in depreciation and

amortization of $27 ($523 in 2025 compared to $550 in 2024) and (v) a decrease in insurance costs of $291 ($1,030 in 2025 compared to $1,321 in 2024).

Sales and Marketing Expenses

Sales and marketing expenses for the years ended December 31, 2025, and 2024 were $5,356 and $7,069, respectively, representing a decrease of $1,713 or 24%.

The decrease in sales and marketing expenses for the year ended December 31, 2025 was primarily attributable to (i) the revocation of the Oranim agreement, which resulted in lower marketing-related costs of $0 in 2025

compared to $918 in 2024, and (ii) mainly due to the closing of the Rosen highway trade-house at the end of 2024.

Other Operating Expenses

Other operating expenses for the years ended December 31, 2025, and 2024 were $6,387 and $3,229, respectively.

The increase in other operating expenses was primarily attributable to goodwill impairment in Israel and intangible asset impairment in Germany.

Finance income (expense), net

Financing income (expense), net for the years ended December 31, 2025, and 2024 was $(71) and $(2,560), respectively, representing an increase of $2,489. The increase was mainly attributable to a

loss from the effect of foreign exchange of $2,850 during 2025.

Net Loss

Net loss for the years ended December 31, 2025, and 2024 was $11,750 and $11,771, respectively, representing a net loss decrease of $21 or 0%. The change in net loss primarily reflects the factors

discussed above, including changes in revenue, gross profit and operating expenses, as well as changes in finance income (expense), net.

Total Assets

Total assets as of December 31, 2025 and 2024 were $31,736 and $39,188, respectively, representing a decrease of 19%. The decrease is mainly attributed to goodwill and intangible assets impairment at

a total amount of $3,484, and to a decrease of $2,711 in advances to suppliers.

Total assets as of December 31, 2024 were $39,188, compared to $48,813 as of December 31, 2023, representing a decrease of $9,625 or 20%. The decline is mainly attributed to the following:

| • |

Oranim agreement revocation of $9,494, of which is mainly attributed to $3,499 goodwill, $1,414 intangible assets, $837 Inventory, $1,324 trade receivables, $783 Property plant and equipment and $346 reduction of Cash and cash

equivalents;

|

| • |

current assets increase* of $2,365, mainly due to an increase of $7,476 in trade receivables, offset by a $5,924 reduction in Inventory and an increase of $813 in other current assets; and

|

| • |

non-current assets decrease* of $2,496 mainly due to $1,056 reduction of intangible asset, $654 reduction of Investment in affiliates and $545 decrease in Property, plant, and equipment.

|

*Net effect after Oranim revocation effect.

Summary of Quarterly Results

The following tables set out certain financial information for each of the Company’s prior quarterly reporting periods:

|

For the quarters ended

|

December 31,

2025 |

September 30,

2025 |

June 30,

2025 |

March 31,

2025 |

||||||||||||

|

Revenues

|

$

|

15,684

|

$

|

13,851

|

$

|

12,696

|

$

|

12,500

|

||||||||

|

Net Profit (loss)

|

$

|

(7,866

|

)

|

$

|

(3,865

|

)

|

$

|

(194

|

)

|

$

|

175

|

|||||

|

Basic net income (loss) per share:

|

$

|

(1.20

|

)

|

$

|

(0.75

|

)

|

$

|

(0.09

|

)

|

$

|

0.09

|

|||||

|

Diluted net income (loss) per share:

|

$

|

(1.20

|

)

|

$

|

(0.75

|

)

|

$

|

(0.09

|

)

|

$

|

0.09

|

|||||

|

For the quarters ended

|

|

December 31,

2024 |

|

|

September 30,

2024 |

|

|

June 30,

2024 |

|

|

March 31,

2024 |

|

||||

|

Revenues

|

|

$

|

13,335

|

|

|

$

|

13,883

|

|

|

$

|

14,750

|

|

|

$

|

12,063

|

|

|

Net income (loss)

|

|

$

|

(1,213

|

)

|

|

$

|

(1,082

|

)

|

|

$

|

(3,456

|

)

|

|

$

|

(6,020

|

)

|

|

Basic net income (loss) per share:

|

|

$

|

(0.32

|

)

|

|

$

|

(0.41

|

)

|

|

$

|

(1.36

|

)

|

|

$

|

(2.52

|

)

|

|

Diluted net income (loss) per share:

|

|

$

|

(0.32

|

)

|

|

$

|

(0.41

|

)

|

|

$

|

(1.36

|

)

|

|

$

|

(2.52

|

)

|

Non-IFRS Financial Measures

Certain non-IFRS financial measures are referenced in this Management Discussion and Analysis, including “Gross Margin,” “EBITDA” and “Adjusted EBITDA.” These measures are not recognized measures

under IFRS and do not have standardized meanings prescribed by IFRS. Accordingly, they may not be comparable to similarly titled measures presented by other companies.

The Company presents these measures as supplemental information because management uses them to evaluate operating performance, assess underlying trends in its business and facilitate

period-to-period comparisons. These measures should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS.

Reconciliations of these non-IFRS financial measures to the most directly comparable IFRS measures are provided below.

Operating Efficiency and Operating Ratio

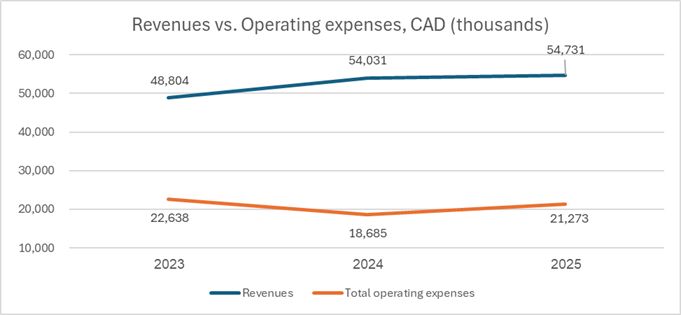

The following chart presents the Company’s revenues and total operating expenses for the fiscal years indicated:

The operating expense ratio for the year ended December 31, 2025, was 39%, compared to 35% for the year ended December 31, 2024, representing a decrease in efficiency of approximately 12%. The

efficiency ratio decline results from increased operational costs, mainly due to other operating expenses.

Gross Margin

Gross Margin is a non-IFRS financial measure that the Company defines as revenue less cost of revenues, divided by revenue (expressed as a percentage). Management uses Gross Margin to evaluate

operating performance and pricing dynamics across reporting periods.

The Company’s definition of Gross Margin may be different from those used by other companies, and therefore, may not be comparable. Thus, Gross Margin should be considered in addition to, not as a

substitute for, or in isolation from, measures prepared in accordance with IFRS.

The Company has included Gross Margin in this Annual Report because it is a key measure used by its management and board of directors to evaluate its operating performance and the efficiency of the

Company’s revenue-generating activities. Accordingly, the Company believes that Gross Margin provides useful information to investors and others in understanding and evaluating the Company’s operating results in the same manner as the Company’s

management and board of directors. The following table presents a computation of gross profit and gross margin for each of the periods indicated:

|

For the Twelve Months Ended

December 31,

|

||||||||

|

|

2025

|

2024

|

||||||

|

Net revenue

|

$

|

54,731

|

$

|

54,031

|

||||

|

Cost of sales

|

$

|

(45,045

|

)

|

$

|

(45,580

|

)

|

||

|

Gross profit

|

$

|

9,686

|

$

|

8,451

|

||||

|

Gross margin

|

18

|

%

|

16

|

%

|

||||

EBITDA and Adjusted EBITDA

Adjusted earnings before interest, taxes, depreciation, and amortization (“EBITDA”) is a non-IFRS financial measure calculated as earnings or loss for the year, adjusted to exclude the following

items which the Company does not believe are reflective of its operating performance:

| • |

depreciation and amortization;

|

| • |

share-based payments;

|

| • |

and other non-recurring costs.

|

The Company’s definition of adjusted EBITDA may be different from those used by other companies, and therefore, may not be comparable. Furthermore, the Company’s definition of adjusted EBITDA does not include the

impact of certain expenses that are reflected in its consolidated financial statements. Thus, adjusted EBITDA should be considered in addition to, not as a substitute for, or in isolation from, measures prepared in accordance with IFRS.

The Company has included adjusted EBITDA in this Annual Report because it is a key measure used by its management and board of directors to evaluate its operating performance and profitability

excluding certain non-operational or non-recurring items. Accordingly, the Company believes that adjusted EBITDA provides useful information to investors and others in understanding and evaluating its operating results in a manner consistent with how

its management and board of directors evaluate its performance.

The Company compensates for these limitations by providing a reconciliation of adjusted EBITDA to the most directly comparable IFRS financial measure, which is loss for the fiscal year. The Company

encourages readers, investors and others to review its financial information in its entirety, not to rely on any single financial measure and to view its adjusted EBITDA in conjunction with its related IFRS financial measure.

Adjusted EBITDA has limitations as a financial measure, and as such should be considered as supplemental in nature. It is not meant as a substitute for the related financial information prepared in

accordance with IFRS. Some of these limitations include the following:

(i)Adjusted EBITDA excludes depreciation of property and equipment, and although these are non-cash charges, the assets being depreciated may have to be replaced in the future.

Adjusted EBITDA does not reflect all cash capital expenditure requirements for such replacements or for new capital expenditure requirements. Adjusted EBITDA also excludes depreciation of right-of-use assets, which contains a cash component;

(ii)Adjusted EBITDA excludes amortization of intangible assets;

(iii)Adjusted EBITDA excludes fair values of employee share compensation payment charges, which have been, and will continue to be for the foreseeable future, a recurring expense in the Company’s business and an

important part of its compensation strategy; and

(iv)Adjusted EBITDA does not reflect impairment of financial assets and impairment of assets as recognized in the consolidated statement of comprehensive loss.

Reconciliation from (loss)/ profit for the year to adjusted EBITDA

|

|

For the Twelve Months

Ended December 31,

|

|||||||

|

|

2025

|

2024

|

||||||

|

Operating loss

|

$

|

(11,587

|

)

|

$

|

(10,234

|

)

|

||

|

Depreciation & amortization

|

$

|

1,956

|

$

|

2,184

|

||||

|

EBITDA

|

$

|

(9,631

|

)

|

$

|

(8,050

|

)

|

||

|

Share-based payments

|

$

|

14

|

$

|

369

|

||||

|

Other non-recurring costs 1

|

$

|

6,387

|

$

|

6,612

|

||||

|

Adjusted EBITDA (non-IFRS)

|

$

|

(3,230

|

)

|

$

|

(1,069

|

)

|

||

|

1.

|

Due to goodwill and intangible asset impairment for the twelve months ended December 31, 2025, and revocation of the Oranim transaction dated April 16, 2024, and inventory clearance for the twelve months ended

December 31, 2024.

|

The Company’s Adjusted EBITDA loss increased by 202% in 2025 compared to 2024, primarily reflects the goodwill and intangible asset impairment.

| B. |

Liquidity and Capital Resources

|

Overview

Since the Company’s inception through December 31, 2025, the Company has funded its operations through raising capital, inter alia, through public offering, non-broker private placement transactions

and credits from bank institutions and others.

The Company’s liquidity is affected by the timing of customer collections, inventory turnover and payment terms with suppliers.

As of December 31, 2025, the Company’s cash and restricted cash totaled $3,309 and the Company’s working capital deficit (current assets minus current liabilities) amounted to $11,265. For the year

ended December 31, 2025, the Company had an operating loss of ($11,587) and cash flows provided by operating activities of $4,716.

As of December 31, 2025, the Company’s financial liabilities were $35,351, which included trade payables, other payables and accrued expenses, borrowings and other financial liabilities, a

substantial portion of which had contractual maturities of less than one year.

The Company manages its liquidity risk by reviewing its capital requirements on an ongoing basis. Based on the Company’s working capital position on December 31, 2025, management considers

liquidity risk to be high. As of December 31, 2025, the Company has identified the following liquidity risks related to financial liabilities:

|

Less than one year

|

1 to 5 years

|

6 to 10 years

|

> 10 years

|

|||||||||||||

|

Contractual Obligations

|

$

|

14,674

|

$

|

1,050

|

$

|

-

|

$

|

-

|

||||||||

The maturity profile of the Company’s other financial liabilities (trade payables, other account payable and accrued expenses, and warrants) as of December 31, 2025, are less than one year.

|

|

Payments Due by Period

|

|||||||||||||||||||

|

Contractual Obligations

|

Total

|

Less than one year

|

1 to 3 years

|

4 to 5 years

|

After 5 years

|

|||||||||||||||

|

Debt

|

$

|

15,269

|

$

|

14,333

|

$

|

936

|

$

|

-

|

$

|

-

|

||||||||||

|

Finance Lease Obligations

|

$

|

455

|

$

|

341

|

$

|

114

|

$

|

-

|

$

|

-

|

||||||||||

|

Total Contractual Obligations

|

$

|

15,724

|

$

|

14,674

|

$

|

1,050

|

$

|

-

|

$

|

-

|

||||||||||

As of December 31, 2024 and 2023, the Company’s financial liabilities were 34,069 and 33,563, respectively.

As of December 31, 2025, 2024, and 2023, we have not had any distributions or cash dividends declared per-share for the outstanding Common Shares.

Based on the Company’s working capital position as of December 31, 2025 and the significant portion of the Company’s obligations maturing within the next twelve months, management considers liquidity risk to be

high.

The Company’s current operating budget includes various assumptions concerning the level and timing of cash receipts from sales and cash outflows for operating expenses and capital expenditures, including cost

saving plans. In 2023, the Board approved a cost saving plan, to allow the Company to continue its operations and meet its cash obligations. The cost saving plan entailed reducing costs through efficiencies and synergies primarily involving the

following measures: discontinuing loss-making activities, reducing payroll and headcount, reduction in compensation paid to key management personnel (including layoffs of key executives), operational efficiencies and reduced capital

expenditures. These actions resulted in cost savings during 2024 and 2025, and the Company will continue its efforts for efficiency operations also during 2026.

These conditions raise substantial doubt about the Company’s ability to continue as a going concern. The consolidated financial statements do not include any adjustments relating to the recoverability and

classification of assets or liabilities that might be necessary should the Company be unable to continue as a going concern.

The Annual Financial Statements have been prepared on the basis of accounting principles applicable to a going concern, which assumes that the Company will continue in operation for the foreseeable future and will be

able to realize its assets and discharge its liabilities in the normal course of operations. The Annual Financial Statements do not include any adjustments to the amounts and classification of assets and liabilities that would be necessary should

the Company be unable to continue as a going concern. Such adjustments could be material.

Working Capital and Balance Sheet Position

Total assets as of December 31, 2025 were $31,736, compared to $39,188 as of December 31, 2024. The change was primarily attributable to the impact of the revocation of the Oranim transaction and changes in working

capital balances, including trade receivables and inventory, as well as changes in intangible assets and property, plant and equipment.

As of December 31, 2025, total borrowings and credit from financial and non-financial institutions amounted to $15,269, compared to $15,611 as of December 31, 2024.

Outstanding Borrowings

As of December 31, 2025 and 2024, the Company’s borrowings consisted of:

|

|

December 31,

|

|||||||

|

|

2025

|

2024

|

||||||

|

Credit from bank institutions

|

$

|

1,067

|

$

|

2,586

|

||||

|

Credit from non-financial institutions

|

9,696

|

6,384

|

||||||

|

Check receivables

|

4,506

|

6,641

|

||||||

|

Total borrowings

|

$

|

15,269

|

$

|

15,611

|

||||

Cash Flows

The Company’s primary recurring uses of cash include funding operating expenses, inventory purchases and other working capital needs.

The table below presents the Company’s cash flows for the periods indicated (in thousands):

|

|

For the Year Ended

December 31,

|

|||||||

|

2025

|

2024

|

|||||||

|

Net cash provided by (used in):

|

||||||||

|

Operating activities

|

$

|

4,716

|

$

|

(1,077

|

)

|

|||

|

Investing activities

|

$

|

(531

|

)

|

$

|

(470

|

)

|

||

|

Financing activities

|

$

|

1,146

|

$

|

3,825

|

||||

|

Effect of foreign exchange

|

$

|

(3,467

|

)

|

$

|

(3,228

|

)

|

||

|

Increase (decrease) in cash

|

$

|

1,864

|

$

|

(950

|

)

|

|||

Operating Activities

Operating activities provided cash of $4,716 and used cash of $1,077 for the years ended December 31, 2025 and 2024, respectively. Net cash provided by operating activities primarily reflects the Company’s operating

loss, changes in working capital and non-cash items. The year-over-year change was primarily driven by changes in trade receivables, inventory and trade payables.

Investing Activities

Investing activities used cash of $531 and $470 for the year ended December 31, 2025, and 2024, respectively, primarily driven by changes in restricted cash.

Financing Activities

Financing activities provided cash of $1,146 and $3,825 for the years ended December 31, 2025 and 2024, respectively. Financing cash flows during 2025 primarily reflected proceeds from the issuance of share capital,

borrowings and repayments under credit facilities, offset by proceeds from discounted checks and cash paid for interest.

Off-Balance Sheet Arrangements

The Company had no off-balance sheet arrangements as of December 31, 2025.

Sources of Liquidity and Financing Arrangements

The Company’s primary sources of liquidity consist of cash generated from operations, borrowings under credit facilities, private placements of equity securities and convertible instruments, and

short-term financing arrangements with financial and non-financial institutions.

As of December 31, 2025, the Company had cash and restricted cash of $3,309. The Company continues to rely on external financing arrangements to support working capital needs and to fund operations.

Investment in Xinetza

On December 26, 2019, IMC Holdings entered into a Share Purchase Agreement with Xinteza API Ltd. (“Xinteza”), under which IMC Holdings invested an aggregate

amount of US$1,700 (approximately $2,468) in exchange for the issuance of 38,082 preferred shares of Xinteza.

On February 24, 2022, IMC Holdings entered into a Simple Agreement for Future Equity with Xinteza, under which IMC Holdings invested US$100 (approximately $125), in exchange for additional future

shares of Xinteza.

As of December 31, 2025, IMC Holdings holds 25.32% of the voting rights of Xinteza and has the right for two members of the Board of Directors out of five. However, it was determined that the

economic interests of the preferred shares are not substantially identical to those of ordinary shares (due to such features as liquidation preference and redemption feature). Accordingly, since the preferred shares do not meet the ordinary equity

ownership interest criteria, the equity method is not applicable, and the investment in Xinteza is subject to the provisions of IFRS 9 and is accounted for as a financial asset measured at fair value through profit or loss categorized within Level 3

of the fair value hierarchy.

As of December 31, 2025, and 2024, the investment in an affiliate amounted to $1,776 and $1,631, respectively, due to an effect of foreign currency translation of $145.

Revolving Credit Facility with Bank Mizrahi

On March 23, 2022, Focus entered into a revolving credit facility with an Israeli bank, Bank Mizrahi (the “Mizrahi Facility”). The Mizrahi Facility is

guaranteed by Focus assets. Advances from the Mizrahi Facility were used for working capital needs. The Mizrahi Facility had a total commitment of up to NIS 15,000 (approximately $6,000) and had a one-year term for on-going needs and 6 months term

for imports and purchases needs. The Mizrahi Facility is renewable upon mutual agreement by the parties. The borrowing base available for draw at any time throughout the Mizrahi Facility and is subject to several covenants to be measured on a

quarterly basis. The Mizrahi Facility bears interest at the Israeli Prime interest rate plus 1.5%.

On May 17, 2023, the Company and Bank Mizrahi entered into a new credit facility with total commitment of up to NIS 10,000 (approximately $3,600) (the “New Mizrahi

Facility”). The New Mizrahi Facility consists of NIS 5,000 credit line and NIS 5,000 loan to be settled with twenty-four (24) monthly installments from May 17, 2023. This loan bears interest at the Israeli Prime interest rate plus 2.9%.

On August 1, 2024, the credit line of approximately NIS 1,825 related to the New Mizrahi Facility was converted into a six-month short-term loan, bearing an annual variable interest rate of P+1.9%

(with the Israel Prime interest rate as of the submission date being 6%).

As of December 31, 2024, Focus had a short-term loan of $2,586 in respect of the new Mizrahi facility. The New Credit facility is also subject to several covenants to be measured on a quarterly basis

which were not met as of December 31, 2024.

As of March 20, 2025, Mizrahi Bank has been extending the short-term loan on a weekly basis, however,

on March 20, 2025, the bank and the company signed an agreement modifying the New Mizrahi Facility terms as follows:

|

•

|

$1,560 (NIS 4 million) was extended as a loan with a six-month grace period, after which repayment will be made in 31 monthly installments

commencing on September 10, 2025. The principal loan will not require a personal guarantee and will bear an interest at a rate of P+2.9% to be paid monthly, commencing on April 20, 2025.

|

|

•

|

The remaining $390 (NIS 1 million) was extended as a credit line from March 19, 2025, to March 12, 2026. As of the date of this report, the credit

line has been extended to September 25, 2026.

|

Mr. Oren Shuster, the Company’s Chief Executive Officer and director provided the bank with a personal guarantee for the outstanding borrowed amount, allowing the New Mizrahi Facility to remain effective.

On June 29, 2025, the Mizrahi Facility approved to postpone by one month the first loan installment of the principal amount (only and not the interest) from September 21, 2025, to October 21, 2025,

which was paid in full on time.

On April 29, 2025, IMC Holdings entered into a short-term loan agreement with a non-financial institution in the amount of NIS 1,000 (approximately $375). This loan bears interest at an annual rate

of 17% and matures 12 months from the date of signing the loan agreement.

Loan to Telecana

On November 29, 2022, the Company’s subsidiary, IMC Holdings entered into a convertible loan agreement (the “Telecana Loan Agreement”) with Telecana Ltd. (“Telecana”) and the sole shareholder of Telecana, whereby IMC Holdings loaned NIS 1,545 (approximately $605) to Telecana according to the following advance schedule: NIS 45 on January 15, 2023 (approximately $18);

NIS 250 on January 31, 2023 (approximately $98); NIS 500 (approximately $196) on February 28, 2023; NIS 500 (approximately $196) on April 5, 2023; and NIS 250 (approximately $98) on May 5, 2023. Telecana opened a pharmacy and obtained from the IMCA a

license to dispense medical cannabis products. Pursuant to the Telecana Loan Agreement, subject to IMCA approval, the loan can be converted into 51% of the share capital of Telecana, with such conversion to occur at the earlier: (i) upon receipt of a

preliminary license from the IMCA; and (ii) at any time at the sole discretion of IMC Holdings.

On January 5, 2025, IMC Holdings entered into an agreement with a third party under which it sold all of its contractual rights under the Telecana Loan Agreement for a total consideration of NIS 350

(approximately $138).

Loan and Repayment to ADI

On October 11, 2022, IMC Holdings entered into a loan agreement with A.D.I. Car Alarms Stereo Systems Ltd (“ADI” and the “ADI

Agreement”), to borrow a principal amount of NIS 10,500 (approximately $4 million) at an annual interest of 15% (the “ADI Loan”), which was to be repaid within 12 months of the date of the ADI

Agreement. The ADI Loan was secured by a second rank land charge on the German Logistics Center. In addition, Mr. Oren Shuster, the Company’s Chief Executive Officer and director, provided a personal guarantee to ADI should the security not be

sufficient to cover the repayment of the ADI Loan.

On October 25, 2023, IMC Holdings and ADI signed an amendment to the ADI Agreement, extending the loan period by an additional 3 months. During this extended period, the interest rate was 15%, with

associated fees and commissions of 3% per annum for the application fee and an origination fee of 3% per annum. On February 26, 2024, IMC Holdings and ADI signed an additional amendment to the ADI Agreement, extending the loan period until April 15,

2024, with the same terms as the first amendment, as specified above.

On March 5, 2025, IMC Holdings and ADI signed an amendment postponing the repayment of the remaining ADI Loan to June 30, 2025. The Company repaid NIS 6 million (CAD 2,575) of the outstanding balance

of the ADI Loan by using the proceeds from the November 2024 Offering (defined below). The parties are currently in discussions about the repayment of the outstanding balance of the ADI Loan.

Life Offering

In January and February of 2023, the Company issued an aggregate of 2,828,248 units (each a “Life Unit”) at a price of US$1.25 per Life Unit for aggregate

gross proceeds of US$3,535 in a series of closings pursuant to a non-brokered private placement offering to purchasers resident in Canada (except the Province of Quebec) and/or other qualifying jurisdictions relying on the listed issuer financing

exempt under Part 5A of National Instrument 45-106 - Prospectus Exemptions (the “LIFE Offering”). Each Life Unit consisted of one common share, no par value per share of the Company (“Common Shares”) and one Common Share purchase warrant (each a “Life Warrant”), with each Life Warrant entitling the holder thereof to purchase one additional Common Share at an exercise price of

US$1.50 for a period of 36 months from the date of issue.

In addition, a non-independent director of the Company subscribed for an aggregate of 131,700 Life Units under the LIFE Offering at an aggregate subscription price of US$165. The director’s

subscription price was satisfied by the settlement of US$165 in debt owed by the Company to the director for certain consulting services previously rendered.

In connection with the LIFE Offering, the Company and Odyssey Trust Company entered a series of warrant indentures on January 30, 2023 (the “First LIFE Warrant

Indenture”), February 7, 2023 (the “Second LIFE Warrant Indenture”) and February 16, 2024 (the “Third LIFE Warrant Indenture”) to govern the terms and conditions

of the Life Warrants.

Concurrent with the LIFE Offering, the Company issued an aggregate of 2,317,171 units on a non-brokered private placement basis for US$1.25 per unit for aggregate gross proceeds of US$2,897 (the “Concurrent Offering”). The Concurrent Offering was led by the Company’s insiders. The units offered under the Concurrent Offering were sold under similar terms as the Life Offering and were offered for sale to

purchasers in all provinces and territories of Canada and jurisdictions outside Canada pursuant to available prospectus exemptions other than for the LIFE Offering exemption. All units issued under the Concurrent Offering were subject to a

statutory hold period of four months and one day in accordance with applicable Canadian securities laws.

October 2023 Short-term Loan Agreement

On October 17, 2023, IMC Holdings entered into a short-term loan agreement with a non-financial institution in the amount of NIS 1,800 (approximately $660). Such loan bears interest at an annual rate

of 18% and originally matured six months from the date of issuance along with the associated fees and commissions of 4% per annum for application fee and an origination fee of 4% per annum. On April 17, 2024, IMC Holdings and the lender signed an

amendment to extend the loan period until April 18, 2025, with an annual interest rate of 17% with no additional fees associated as in the initial loan period. On January 16, 2025, the lender and IMC Holdings signed a second amendment extending the

loan period until May 16, 2025. As part of the extension, IMC Holdings agreed to pay an additional fee of NIS 150 (approximately $61). The lender is entitled to request the immediate repayment of EUR 35 at any time by submitting a written request. As

of the date of this Annual Report, the principal amount of the loan and the accrued interest were fully paid.

April 2024 Loan Agreement

On April 17, 2024, Pharm Yarok entered into a loan agreement with a non-financial institution in the amount of NIS 3,000 (approximately $1,082) (the “April 2024 Loan”).

The April 2024 Loan bore an annual interest rate of 15% and matured 12 months from the date of issuance. The April 2024 Loan was secured by the following collaterals and guarantees: (a) a first-ranking floating charge over the assets of Pharm Yarok

(b) a first-ranking fixed charge over the holdings (23.3%) of its subsidiary, IMC Holdings, of Xinteza; (c) a personal guarantee by Mr. Oren Shuster, the Company’s Chief Executive Officer and director; and (D) a guarantee by us.

On January 30, 2025, Pharm Yarok and the lender signed an amendment to the April 2024 Loan pursuant to which Pharm Yarok paid NIS 1,000 (approximately $393) on January 31, 2025, and the remaining

loan principal amount of NIS 2,000 (approximately $844) was extended until June 30, 2026.

May 2024 Convertible Debenture Offering

On May 26, 2024, the Company closed a non-brokered private placement (the “May 2024 Private Placement”) of secured convertible debentures (each, a “May 2024 Debentures”) for aggregate proceeds of $2,092. The May 2024 Debentures were issued to holders of short-term loans and obligations owed by the Company or its wholly owned subsidiaries and were inclusive of a 10% extension

fee in full settlement of such debt to the holders. The May 2024 Debentures matured on May 26, 2025 and have not incurred interest. The May 2024 Debentures were convertible into Common Shares at a conversion price of $5.1 per Common Share

(following the July 2024 Consolidation). The Company was entitled through the term of the May 2024 Debentures to early repayment of the May 2024 Debentures for cash amount of $2,092. Mr. Oren Shuster, the Company’s Chief Executive Officer and

director, subscribed for an aggregate of $237 of May 2024 Debentures in the May 2024 Private Placement.

Effective May 26, 2025, following the shareholders' approval, the Company and the creditors agreed to extend the term of the May 2024 Debentures until May 25, 2026, subject to extension fee of

additional 10%, such that upon maturity of the May 2024 Debentures, the principal to be paid will be $2,301. The conversion price was determined as $2.61 per Common Share and the Company was entitled to through the term of the May 2024 Debentures to

early repayment of the May 2024 Debentures for cash amount of $2,301.

July 2024 Short-term Loan Agreement

On July 1, 2024, IMC Holdings entered into a short-term loan agreement with a non-financial institution in the amount of NIS 3,000 (approximately $1,113). Such loan bore interest at an annual rate of

12% and originally matured 62 days from the date of signing the loan agreement. IMC Holdings and the lender executed amendments to the loan agreement, each extending the maturity date, thereby postponing the

maturity date to February 28, 2026, under the same terms and conditions. The loan, including the accrued interest, was fully paid by February 28, 2026.

Payment schedule with third party

On July 30, 2024, the Company entered into an acknowledgment and payment schedule agreement with a third party regarding unpaid fees, charges, and disbursements for services rendered to us. According

to the terms of the agreement, we shall pay $54,000 on the first business day of each month for twenty-four (24) months, with the first payment due on November 1, 2024.

November 2024 Debt Settlement and Loan Bonus

On November 12, 2024, the Company completed a debt settlement (the “November 2024 Debt Settlement”) in the amount of US$560,000 with Mr. Oren Shuster, the

Company’s Chief Executive Officer and director. Since October 2022, the Company, through its subsidiaries, had borrowed more than US$8,000,000 (together, the “Loans”) from various groups. As required by the

lenders, Mr. Shuster personally guaranteed the Loans. The independent members of the Board commissioned a valuation to determine the value of Mr. Shuster’s personal guarantees, which ascribes the benefit to the Company to be approximately US$560,000

(the “Shuster Benefit”). To repay Mr. Shuster in connection with the Shuster Benefit, and to preserve the Company’s cash for working capital, the Company issued Mr. Shuster 110,576 Common Shares and 152,701

pre-funded Common Share purchase warrants (each, a “Pre-Funded November 2024 Warrant”) at a deemed price of $2.88 per share.

November 2024 Private Placement of Units and Warrants Amendments

On November 12, 2024, the Company closed a non-brokered private placement offering (the “November 2024 Offering”) through the issuance of 742,517 units (each,

a “November 2024 Unit”) at a purchase price of $2.88 per November 2024 Unit, for gross proceeds of $2,138. The November 2024 Unit price was calculated on the basis of the deemed price per Common Share equal to

the 10-day volume weighted average price of the Common Shares on the Exchange ending on the trading day preceding October 3, 2024, and consisted of one Common Share and one warrant (the “November 2024 Private

Placement Warrant”).

Mr. Oren Shuster, the Company’s Chief Executive Officer and director, Mr. Shmulik Arbel, the Company’s director, and Mr. Rafael Gabay, an insider, (together, the “Participating

Insiders”) each participated in the November 2024 Offering.

Mr. Shuster acquired 194,109 November 2024 Units, 110,576 Common Shares in connection with the November 2024 Debt Settlement, and 152,701 pre-funded warrants. Mr. Arbel acquired 48,348 November 2024

Units. Mr. Gabay acquired 194,087 November 2024 Units.

The November 2024 Transactions were approved by the members of the Board who are independent for the purposes of the November 2024 Transactions. No special committee was established in connection

with the November 2024 Transactions; however, the independent members of the Board commissioned a third-party valuator to determine the Shuster Benefit. The Company also used the proceeds from the November 2024 Offering for the repayment of the ADI

Loan (as defined herein).

On August 13, 2025, the Company entered into agreements with the holders of the November 2024 Private Placement Warrant. Prior to such amendments, the November 2024 Private Placement Warrants were

exercisable immediately upon issuance at an exercise price of C$4.32 per common share and had a termination date of November 12, 2026. Pursuant to the amendments, the Company reduced the exercise price of each November 2024 Private Placement Warrant

from C$4.32 per common share to C$3.43 per common share and extended the expiration date of each November 2024 Private Placement Warrant from November 12, 2026 to July 31, 2030. Except as set forth above, all other terms of the Warrants remain

unchanged and in full force and effect.

April 2025 Short-Term Loan Agreement

On April 29, 2025, IMC Holdings entered into a short-term loan agreement with a non-financial institution in the amount of NIS 1,000 (approximately $375). The loan bears interest at an annual rate of

17% and matures 12 months from the date of signing the loan agreement.

April 2025 Loan from the Company’s Chief Executive Officer

On April 29, 2025, Mr. Oren Shuster, the Company’s Chief Executive Officer and director, loaned NIS 1,000 (approximately $375) to IMC Holdings. The loan bears fixed annual interest at the rate prescribed by the Income

Tax Regulations for determining the interest rate under Section 3(i) of the Israeli Income Tax Ordinance, from the date the loan is provided until the repayment date and shall be paid together with applicable VAT as required by law. The

participation of the Mr. Shuster constituted a “related party transaction”, as such term is defined in Multilateral Instrument 61-101 0 Protection of Minority Security Holders in Special Transactions (“MI 61-101”) and would require the Company to

receive minority shareholder approval for and obtain a formal valuation for the subject matter of, the transaction in accordance with MI 61-101, prior to the completion of such transaction. However, in completing the loan, the Company has relied on

exemptions from the formal valuation and minority shareholder approval requirements of MI 61-101, in each case on the basis that the fair market value of the loan did not exceed 25% of the Company’s market capitalization, as determined in

accordance with MI 61-101.

May 2025 Short-Term Loan Agreement

On May 25, 2025, IMC Holdings entered into a short-term loan agreement with a non-financial institution in the amount of NIS 350 (approximately $131). This loan bears interest at an annual rate of

17% and matures on June 25, 2025. The parties extended the maturity date to June 25, 2026.

July 2025 Loan Agreement

On July 6, 2025, the Company entered into a loan agreement with L.I.A. Pure Capital Ltd. (the “Lender”) for an aggregate amount of US$2 million. Pursuant to

the Loan Agreement, the Company received an amount of US$1 million (the “First Loan Tranche”) and may receive an additional amount of US$1 million (the “Second Loan Tranche”)

no later than 60 days from signing the Loan Agreement, subject to satisfying certain conditions. Pursuant to the Loan Agreement, the Lender has a right to recommend a director to be appointed to the Company’s Board.

The loan bears annual interest at a rate of 8% (plus VAT) and is repayable in full, including accrued interest, by June 30, 2026. In the event of non-repayment by that date, default interest at a

rate of 15% per annum (plus VAT) will apply. The loan is secured by a pledge over 100% of the shares of IMC Holdings Ltd., the Company’s wholly owned subsidiary, with the pledged shares held directly by us.

The Company has also committed to raise at least USD 3 million in capital within 60 days of signing the Loan Agreement, through a public offering underwritten or distributed by Aegis Capital Corp. If

the Company raises US $4 million or more, the Lender will not be obligated to provide the second loan tranche. In the event that the Company raises US $5 million or more, the Lender may exercise an acceleration right, requiring the Company to repay

the outstanding loan within 45 business days of written notice.

July 2025 Private Placement Offering

On July 30, 2025, the Company entered into subscription agreements (the “Subscription Agreements”) for a private placement financing with certain investors.

Under the Subscription Agreements, the investors have agreed to purchase an aggregate of 2,050,000 units (each a “July 2025 Unit”, and collectively, the “July 2025 Units”)

at a purchase price of $2.74 per July 2025 Unit. Each July 2025 Unit consists of one Common Share of, or one common share pre-funded warrant in lieu thereof, and one common share purchase warrant.

The offering amount and July 2025 Unit price were calculated based on the official exchange rate as of July 21, 2025, of 1 USD = 1.3713 CAD (USD/ILS = 3.3550; CAD/ILS = 2.4465) as published on the

website of the Bank of Israel.

Each warrant entitles its holder to purchase one Common Share at an exercise price of $3.43 per warrant share, became exercisable immediately upon issuance and for a period of sixty (60) months from

its issuance. If the warrants are not exercised by the applicable expiry date, the warrants will expire and be of no further force or effect. The warrants and the warrant Shares may not be traded for a period of four (4) months, unless permitted

under applicable securities legislation.

Each pre-funded warrant entitles its holder to purchase one Common Share at a price of $0.00001 per pre-funded share, became exercisable immediately upon issuance and may be exercised at any time

until exercised in full. The pre-funded warrants and the pre-funded warrant Shares may not be traded for a period of 4 months, unless permitted under applicable securities legislation.

The offering resulted in gross proceeds to the Company of $5,622, which the Company intends to use for general working capital, repayment of existing indebtedness and general corporate purposes. The

offering closed on July 30, 2025.

In connection with the offering, on July 31, 2025, the Company entered into a Consulting Agreement (the “Consulting Agreement”) with Pure Equity Ltd. (“Pure Equity”), pursuant to which Pure Equity provided the Company with consulting services related to the offering. In consideration of the consulting services, the Company issued to Pure Equity a warrant (the “Finder’s Warrant”) to purchase up to 140,000 common shares of the Company (the “Finder’s Warrant Shares”). In addition, pursuant to the Consulting Agreement, Pure Equity

shall be entitled to a one-time cash payment of $260,000 plus applicable taxes.

The Finder’s Warrant has an exercise price of US$2.50 per Finder’s Warrant Share, became exercisable immediately upon issuance and for a period of 60 months following its issuance. The Finder’s

Warrant and the Finder’s Warrant Share were not to trade for a period of 4 months, unless permitted under applicable securities legislation.

July 2025 Short-Term Loan Agreement

On July 16, 2025, Rosen High Way entered into a short-term loan agreement, with a non-financial institution in the amount of NIS 500 (approximately $202). This loan bears interest at an annual rate

of 17% and matures on July 16, 2026.

October 2025 Short-Term Loan Agreement

On October 5, 2025, IMC Holdings entered into a short-term loan agreement with a non-financial institution in the amount of NIS 500 (approximately $211). This loan bears interest at an annual rate of 17% and matured on

November 13, 2025. The Company is currently in discussions with the lender regarding a potential extension of the loan.

Note Purchase Agreements, Convertible Notes and Warrants

On January 7, 2026, the Company entered into a Note Purchase Agreement (the “Purchase Agreement”) with an institutional investor (the “Investor”), pursuant to which the Company issued to the Investor: (A) a convertible note (the “Note”) in the principal amount of US$1,710 (the “Subscription Amount”), which is convertible into the Company’s Common Shares at a price equal to ninety percent (90%) of the Subscription Amount and (B) a warrant to purchase up to 228,150 Common Shares, which is the number equal to

thirty-three and one-third percent (33⅓%) of the Subscription Amount divided by an exercise price of $3.45 per Common Share (the “First Transaction”). The First Transaction closed on January 20, 2026.

In addition, on January 20, 2026, the Company entered into an additional Note Purchase Agreement (the “Additional Purchase Agreement” and, together with the

Purchase Agreement, the “Purchase Agreements”) with the Investor, pursuant to which the Company issued to the Investor: (A) a convertible note (the “Second Note” and,

together with the Note, the “Notes”) in the principal amount of US$703 (the “Additional Subscription Amount” and, together with the Subscription Amount, the “Subscription Amounts”) which is convertible into Common Shares at a price equal to 90% of the Additional Subscription Amount and (B) a warrant to purchase up to 93,671 Common Shares, which is the number equal to

thirty-three and one-third percent (33⅓%) of the Additional Subscription Amount divided by an exercise price of $3.45 per Common Share (the “Second Transaction” and, together with the First Transaction, the “Offerings”). The Second Transaction closed on January 21, 2026.

The Company intends to use the net proceeds of $2,172 received from the Offerings for debt repayment and general corporate purposes.

Each Note bears an interest rate of 8.0% per annum accruing from the closing date of the First Transaction and the Second Transaction, as applicable, (which shall increase to 14.0% upon the

occurrence of an Event of Default, as defined in the Notes). The Notes are not repayable in cash and the Company’s obligations thereunder will be satisfied solely through the issuance of the Company’s Common Shares upon conversion of the Notes in

accordance with their terms.

The number of Common Shares issuable upon any conversion of principal amount under the Notes is determined by dividing the applicable conversion amount by the conversion price (the “Conversion Price”). The Conversion Price is equal to the lower of (i) the Fixed Price, as defined in each of the Notes, or (ii) 90% of the lowest daily volume-weighted average price of the Common Shares during the

20 consecutive trading days immediately preceding the conversion date, (the “Variable Price”), provided, however, that the Variable Price will not be lower than the Floor Price, as defined in each of the Notes.

The Fixed Price in the Note and in the Second Note is $0.29 and $1.38, respectively. The Floor Price in the Note and in the Second Note is $0.29 and $0.275, respectively.

The warrants entitle their holder to purchase one Common Share at an exercise price of $3.45 per warrant share. The warrants are exercisable immediately upon their issuance date, January 21, 2026,

for a period of 5 years, until January 21, 2031. If the warrants are not exercised by their applicable expiry date, they will expire and be of no further force or effect. The warrants and the warrant shares may not be traded for a period of four

months, unless permitted under applicable securities legislation.

The Notes include customary limitations on conversion, including a beneficial ownership cap of 4.99% of the outstanding Common Shares following the conversion.

Transactions with Related Parties

Approval of Related Party Transactions

All related party transactions are reviewed and approved by our Board of Directors or an independent committee thereof in accordance with applicable corporate governance requirements and, where

applicable, MI 61-101. Unless applicable exemptions from the requirements of MI 61-101 apply, related party transactions are subject to formal valuation and minority shareholder approval. Minority shareholder approval excludes the votes of any

interested party or related parties of an interest party from the votes counted in the shareholder approval.

Employment and Management Agreements

We have entered into written employment or service agreements with certain of our executive officers. These agreements contain customary provisions regarding confidentiality, assignment of

inventions and, where applicable, non-competition, subject to applicable law. We have also entered into indemnification agreements with our directors and officers and maintain directors’ and officers’ liability insurance.

Effective January 15, 2018, we and Ewave entered into a management services agreement (the “Shuster Agreement”) pursuant to which Oren Shuster provides

services as our Chief Executive Officer. Mr. Shuster is employed and compensated by Ewave. Pursuant to the Shuster Agreement, Ewave charges a monthly fee of NIS 108,350 plus VAT (approximately $43,900 plus tax per month). Either party may terminate

the agreement upon three months’ prior notice, during which payments continue. We may terminate the agreement immediately for cause without notice. Ewave, which is jointly owned by Mr. Shuster and Rafael Gabay, is a related party to us.

Equity Compensation

See Item 6B in the Company’s Annual Report– “Compensation” for a description of our Securities-Based Compensation Arrangements.

Transactions Since January 1, 2023

For purposes of this section, related parties include (i) our directors and executive officers; (ii) beneficial owners of 10% or more of our voting power; (iii) entities controlled by such persons;

and (iv) other persons or entities meeting the definition of a related party under applicable securities laws and IFRS.

IMC Holdings leases a 358 square-meter facility in Kibutz Glil Yam for administrative activities. Since August 2024, IMC Holdings sub leases the facility to Ewave Nadlan International Investments

Ltd, a subsidiary of Ewave Group owned by Mr. Oren Shuater and Refael Gabay, pursuant to a sublease arrangement.

On April 2, 2019, IMC Holdings and Focus entered into t the Focus Agreement, pursuant to which IMC Holdings obtained an option to acquire all ordinary shares of Focus held by Messrs. Shuster and

Gabay. Following IMCA approval on February 26, 2024, IMC Holdings acquired 74% of Focus. On September 2024, the Board engaged an independent third-party valuator to determine the purchase price of the remaining 26% interest. The purchase price was

determined to be NIS 818,740 (the “Focus Purchase Price”). To preserve cash, we agreed to settle the Focus Purchase Price through the issuance of 128,818 Common Shares at a deemed price of C$2.44 per share,

equal to the ten-day VWAP on the CSE prior to shareholder approval. The shares were subject to a four-month and one-day hold period and applicable U.S. Securities Act legends.

Certain insiders participated in tranches of the LIFE Concurrent Offering and LIFE Offering in 2023. These transactions constituted related party transactions under MI 61-101, and we relied on

applicable exemptions based on the relative size of insider participation.

On October 12, 2023, Mr. Shuster loaned NIS 500 (approximately $170) to IMC Holdings. The transaction constituted a related party transaction under MI 61-101. We relied on available exemptions

based on the size of the transaction relative to our market capitalization.

On November 12, 2024, we completed a debt settlement in the amount of US$560,000 with Mr. Shuster in connection with personal guarantees he had provided for certain of our loan obligations. The

independent members of our Board obtained an independent valuation of the benefit derived from such guarantees. To settle this amount and preserve cash, we issued 110,576 Common Shares and 152,701 pre-funded warrants at a deemed price of C$2.88.

The warrants were subsequently exercised following disinterested shareholder approval for Mr. Shuster to become a Control Person.

On May 27, 2025, we completed a non-brokered private placement of secured convertible debentures for aggregate proceeds of C$2,301,174.70. The debentures mature on May 26, 2026 and are convertible

at C$2.61 per Common Share.

Mr. Shuster and Rafael Gabay participated in the offering, subscribing for C$260,935.40 and C$260,278.70, respectively.

We are party to indemnification arrangements with certain directors and officers in connection with prior acquisitions.

Other than the transactions described above and compensation paid in the ordinary course to key management personnel, we had no other material related party transactions during the period covered

by the Company’s Annual Report.

Current Outlook

For the year ended December 31, 2025, the Company generated revenue of $54,731 and incurred a net loss of $11,750. Cash flows provided by operating activities were $4,716.

As of December 31, 2025, the Company had cash and restricted cash of $3,309 and working capital deficit of $11,265.

Based on current cash resources, operating forecasts and existing financing arrangements, management believes that the Company does not have sufficient liquidity to fund its planned operations for at

least twelve months from the issuance date of these consolidated financial statements.

These conditions raise substantial doubt about the Company’s ability to continue as a going concern. The consolidated financial statements have been prepared on a going concern basis and do not

include any adjustments that might result from the outcome of this uncertainty. If the Company is unable to continue as a going concern, adjustments to the carrying amounts and classification of assets and liabilities may be required, and such

adjustments could be material.

Management is pursuing additional financing alternatives, including equity issuances, convertible instruments and debt arrangements. There can be no assurance that additional capital will be

available on acceptable terms, or at all.

The Company’s future capital requirements will depend on numerous factors, including:

| • |

Revenue growth and gross margin performance in Israel and Germany

|

| • |

Working capital requirements and inventory turnover

|

| • |

The timing and extent of regulatory developments

|

| • |

The availability and terms of refinancing of existing indebtedness

|

| • |

Compliance with financial covenants under credit facilities

|

| • |

Market conditions affecting access to equity and debt capital

|

| • |

Potential strategic transactions

|

Until the Company achieves sustained profitability and positive operating cash flows, it expects to continue relying on debt and equity financings to fund operations. If additional capital is not available when required,

the Company may be required to delay or reduce operating activities and capital expenditures.