Exhibit 99.3

|

Management’s Discussion and Analysis

|

|

TABLE OF CONTENTS

|

3

|

|

|

4

|

|

|

4

|

|

|

4

|

|

|

7

|

|

|

8

|

|

|

12

|

|

|

16

|

|

|

17

|

|

|

20

|

|

|

26

|

|

|

27

|

|

|

28

|

|

|

28

|

|

|

30

|

|

|

30

|

|

|

34

|

|

|

34

|

|

|

36

|

|

|

36

|

|

|

49

|

|

|

51

|

|

|

61

|

|

|

74

|

2

|

Management’s Discussion and Analysis

|

|

IM Cannabis Corp. (“IM Cannabis” or the “Company”) is a British Columbia company operating in the international medical

cannabis industry. The Company’s common shares (the “Common Shares”) trade under the ticker symbol “IMCC” on the NASDAQ Capital Market (“NASDAQ”) as of March 1, 2021.

This Management’s Discussion and Analysis (this “MD&A”) reports on the consolidated financial condition and operating results of IM Cannabis for the year

and three months ended March 31, 2026. Throughout this MD&A, unless otherwise specified, references to “we”, “us”, “our” or similar terms, as well as the “Company” and “IM Cannabis” refer to IM Cannabis Corp., together with its subsidiaries, on a

consolidated basis, and the “Group” refers to the Company, its subsidiaries, and Focus Medical Herbs Ltd.

This MD&A should be read in conjunction with the interim condensed consolidated financial statements of the Company and the notes thereto for the three months ended March 31, 2026 and 2025 (the “Interim Financial Statements”), and with the Company's audited annual consolidated financial statements and the notes thereto for the years ended December 31, 2025 and 2024 (the “Annual

Financial Statements”). References herein to “Q1 2026” and “Q1 2025” refer to the three months ended March 31, 2026 and March 31, 2025 respectively, and references to “2025” refer to the year ended December 31, 2025.

The Interim Financial Statements have been prepared by management in accordance with the International Financial Reporting Standards (“IFRS”) as issued by the

International Accounting Standards Board (“IASB”). IFRS requires management to make certain judgments, estimates and assumptions that affect the reported amount of assets and liabilities at the date of the

Interim Financial Statements and the amount of revenue and expenses incurred during the reporting period. The results of operations for the periods reflected herein are not necessarily indicative of results that may be expected for future periods.

The Interim Financial Statements for the three months ended March 31, 2026, include the accounts of the Group, which includes, among others, the following entities:

|

Legal Entity

|

Jurisdiction

|

Relationship with the Company

|

|

I.M.C. Holdings Ltd. (“IMC Holdings”)

|

Israel

|

Wholly-owned subsidiary

|

|

I.M.C. Pharma Ltd. (“IMC Pharma”)

|

Israel

|

Wholly-owned subsidiary of IMC Holdings

|

|

Focus Medical Herbs Ltd. (“Focus")

|

Israel

|

Wholly-owned subsidiary of IMC Holdings

|

|

R.A. Yarok Pharm Ltd. (“Pharm Yarok”)

|

Israel

|

Wholly-owned subsidiary of IMC Holdings

|

|

Rosen High Way Ltd. (“Rosen High Way”)

|

Israel

|

Wholly-owned subsidiary of IMC Holdings

|

|

Rivoly Trading and Marketing Ltd. d/b/a Vironna Pharm (“Vironna”)”

|

Israel

|

Subsidiary of IMC Holdings

|

|

Adjupharm GmbH (“Adjupharm”)

|

Germany

|

Subsidiary of IMC Holdings

|

|

Trichome Financial Corp. (“Trichome") (1)

|

Canada

|

Former wholly-owned subsidiary

|

|

Xinteza API Ltd (“Xinteza”)

|

Israel

|

Subsidiary of IMC Holdings

|

|

Shiran Societe Anonyme (“Greece”)

|

Greece

|

Subsidiary of IMC Holdings

|

|

IM Cannabis Holding NL B.V Netherlands (“IMC Holdings NL”)

|

Netherlands

|

Wholly-owned subsidiary of IMC Holdings

|

| (1) |

Discontinued operations.

|

In this MD&A, unless otherwise indicated, all references: (i) “Company Subsidiaries” are to the Israeli Subsidiaries and Adjupharm, (ii) “Israeli Operations” are to IMC Holdings and the Israeli

Subsidiaries as defined below, (iii) “Trichome” are to Trichome Financial Corp. and its subsidiaries. As of the date of this Interim Report “Israeli Subsidiaries” means

IMC Holdings, IMC Pharma, Focus, Pharm Yarok, Rosen High Way, Vironna and Xinteza.

All dollar figures in this MD&A are expressed in thousands of Canadian Dollars ($), except per share data and unless otherwise noted. All references to “NIS” are to New Israeli Shekels. All

references to “€” or to “Euros” are to Euros. All references to “US$” or to “U.S. Dollars” are to United States Dollars. The Company’s shares, options, units, prefunded warrants, warrants and prices are not expressed in thousands. Prices are not

expressed in thousands.

3

|

Management’s Discussion and Analysis

|

|

Certain non-IFRS financial measures are referenced in this MD&A that do not have any standardized meaning under IFRS, including “Gross Margin”, “EBITDA” and “Adjusted EBITDA”. The Company

believes that these non-IFRS financial measures and operational performance measures, in addition to conventional measures prepared in accordance with IFRS, enable readers to evaluate the Company’s operating results, underlying performance and

prospects in a similar manner to the Company’s management. For a reconciliation of these non-IFRS financial measures to the most comparable IFRS financial measures, as applicable, see the “Metrics and Non-IFRS

Financial Measures” section of the MD&A.

NOTE

REGARDING THE COMPANY’S ACCOUNTING PRACTICES

Unless otherwise indicated, all dollar figures are expressed in thousands and all references to: (i) “dollars” or “CAD”

or “$” are to Canadian dollars; (ii) “USD” or “US$” are to United States of America (“U.S.”

or “United States”) dollars; (iii) “NIS” are to New Israeli Shekels; and (iv) “€” or to “Euros”

are to Euros. All intercompany balances and transactions were eliminated on consolidation. Common shares, stock options, units, prefunded warrants, warrants, and prices, are not expressed in thousands. Our reporting currency and functional currency

is the Canadian dollar. The CAD to USD exchange rate as of March 31, 2026 was 0.71779.

EXECUTIVE

SUMMARY

OVERVIEW – CORPORATE

STRUCTURE

The Company was incorporated on March 7, 1980, under the name “Nirvana Oil & Gas Ltd.” pursuant to the Business Corporations Act (British Columbia). The Company's changed its name to “Nirvana

Industries Ltd.” on October 6, 1986; then to “Consolidated Nirvana Industries Ltd.” on February 22, 1989; then to “Navasota Resources Ltd.” on June 2, 1995, then to Anglo Aluminum Corp.” on January 25, 2010; then to Navasota Resources Inc. on July

12, 2013, and finally to its current name “IM Cannabis Corp.” on October 4, 2019.

The Common Shares began trading on the Canadian Securities Exchange (“CSE”) under the ticker symbol “IMCC” on November 5, 2019, and were subsequently listed on

the Nasdaq Capital Market under the same symbol effective March 1, 2021.

On May 28, 2025, the Company announced that it had applied for a voluntary delisting of its Common Shares from the CSE. The delisting became effective at the close of business on Monday, June 2,

2025, which marked the final trading day of the Company’s securities on the CSE.

The Company’s shares remain listed and continue to trade on Nasdaq under the ticker symbol “IMCC.”

4

|

Management’s Discussion and Analysis

|

|

On October 4, 2019, in connection with the reverse takeover transaction by IMC Holdings, the Company completed a consolidation of its Common Shares on a 2.83:1 basis, changed its name to “IM Cannabis

Corp.” and changed its business from mining to the international medical cannabis industry.

On February 12, 2021, in connection with its Nasdaq listing application, the Company completed a consolidation of its Common Shares on a 4:1 basis.

On November 17, 2022, in connection with regaining compliance with Nasdaq’s continued listing standards, the Company completed a 10:1 consolidation of its Common Shares, which was approved by

shareholders at the Company’s annual and special meetings of shareholders held on October 20, 2022.

On July 12, 2024, in connection with regaining compliance with Nasdaq’s continued listing standards, the Company completed a 6:1 consolidation of its Common Shares. The exercise price and/or

conversion price and number of Common Shares issuable under any of the Company's outstanding convertible securities were proportionately adjusted in connection with the July 2024 Consolidation.

OVERVIEW

– CURRENT OPERATIONS IN ISRAEL AND GERMANY

The Company operates in the medical cannabis sector in Israel and Germany. The Company’s activities in these jurisdictions include sourcing, importation, distribution and sale of medical cannabis

products in compliance with applicable regulatory requirements.

Israel

In Israel, the Company operates through IMC Holdings and its consolidated subsidiary Focus, which holds an IMCA license permitting the importation and supply of medical cannabis products. The

Company’s operations in Israel primarily consist of importing medical cannabis products from approved suppliers and distributing those products to pharmacies and patients in accordance with Israeli regulations. The Company does not currently operate

large-scale cultivation facilities in Israel and relies primarily on imported products that meet applicable quality and regulatory standards.

The Company’s Israeli operations include brand management, regulatory compliance, logistics coordination and relationships with pharmacies and prescribing physicians. Revenue in Israel is generated

from the sale of medical cannabis products to pharmacies and other authorized distributors.

Germany

In Germany, the Company operates through its German subsidiaries, which are authorized to import and distribute medical cannabis products under applicable German and European Union regulations. The

Company’s German operations focus on sourcing EU-GMP compliant medical cannabis products from approved suppliers and distributing such products to licensed pharmacies throughout Germany.

The German market is regulated by the BfArM, and the Company’s import volumes are subject to regulatory requirements, including compliance with applicable pharmaceutical standards. Revenue in Germany

is generated from the sale of imported medical cannabis products to pharmacies and other authorized customers.

The Company’s operations in both jurisdictions are subject to evolving regulatory frameworks, including changes in prescribing practices, import authorizations, product specifications and

distribution models, which may affect its revenues, margins and operating results.

5

|

Management’s Discussion and Analysis

|

|

Iron Swords War and other conflicts’ Effect on Gross Profit

On October 7, 2023, the State of Israel was attacked by the terrorist organization Hamas, and as a result, the State of Israel declared a state of war and a large-scale mobilization of reserves (the

“War”). At the same time, a front of fighting also developed in the northern border against the terrorist organization Hezbollah, which led to extensive evacuation of residents. The War is an exceptional event with security and economic implications

whose extent and outcomes are unpredictable. In response to the War, the State of Israel has taken significant steps to ensure the security of its residents, which have a considerable impact on economic and business activities in the country. The

events of the War have led to a reduction in business activity in the economy and a significant slowdown in economic activity, affecting the business operations of entities in various circles of influence, among others due to the closure of factories

in the south and north of the country, damage to infrastructure, long-term mobilization of reservists, and more. Potential fluctuations in commodity prices, foreign exchange rates, availability of materials, availability of manpower, local services,

and difficulties in accessing local resources have affected and are expected to continue to affect entities whose main operations are in Israel. In addition, the state of warfare also affects the activities of entities that rely on foreign workers or

on workers recruited for the purposes of the fighting, international trade, foreign companies in Israel, civil aviation, and more. As a result, the War has significant implications for the economy and imposes a considerable burden on the continuation

of business activity and the functional and operational continuity of the entities.

In November 2024, a ceasefire was reached with the terrorist organization Hezbollah in the north of the country, but the War continued in other areas.

On June 13, 2025, the State of Israel launched operation “Rising Lion” against military targets in Iran, with a focus on the Iranian nuclear project. As a result, a state of emergency was declared in

Israel, causing repercussions and restrictions on the Israeli economy, which included, inter alia, partial or complete closure of businesses, restrictions on gatherings in workplaces and in the education system, as well as a decrease in workforce due

to reserve enlistment and a reduction in number of foreign workers. During the operation, a targeted American strike was carried out against Iran, after which, on June 24, 2025, a ceasefire was reached between the parties.

Following the above, in October 2025 a ceasefire agreement was signed with terrorist organization Hamas in Gaza and as a result, the fighting subsided on most fronts.

On February 28, 2026, Israel and the United States launched a joint attack against Iranian government targets, following which Iran responded with missile fire towards Israel and other countries in

the region. As a result of the aforementioned, the Israeli government declared a special situation on the home front across the entire country, including restrictions on gatherings and a reduction in economic activity except for essential workplaces

until March 26, 2026.

The Company's management is continuously monitoring the developments regarding the War and is acting in accordance with the guidelines of the various authorities. The Company suffered a negative

impact from the War commencing the last quarter of 2023. The Company has experienced damage to its ability to function, affecting various aspects, including employees, supplies, imports, sales, and more.

6

|

Management’s Discussion and Analysis

|

|

OUR GOAL – DRIVE PROFITABLE

REVENUE GROWTH

Our primary goal is to sustainably increase revenue in each of our core markets, to accelerate our path to profitability and long-term shareholder value while actively managing costs and margins.

As part of its ongoing strategic review, the Company has also made a decision to explore the introduction of additional business activities, with the goal of enhancing long-term growth opportunities

and creating further shareholder value.

Given the evolving regulatory environment, particularly in Germany, the timing, scope, and impact of our plans are uncertain, and actual results may differ materially from current expectations.

HOW WE

PLAN TO ACHIEVE OUR GOAL – CORE STRATEGIES

Our strategy of sustainable and profitable growth consists of:

| • |

Develop and execute a long-term growth plan in Germany, based on the strong sourcing infrastructure in Israel which is powered by advanced product knowledge and regulatory expertise.

|

| • |

Optimize inventory to meet demand while managing INCB/BfArM import-estimate constraints and aligning products to Ph. Eur. 11.5 specifications. Diversify EU-GMP suppliers (Israel and other countries) to support availability.

|

| • |

Properly position brands with respect to target-market, price, potency and quality, such as our IMC brand in Israel and Germany.

|

| • |

Strong focus on efficiencies and synergies with domestic expertise in Israel and Germany.

|

| • |

High-quality, reliable supply to our customers and patients, leading to recurring sales.

|

| • |

Ongoing introduction of new Stock Keeping Units (“SKU”) to keep consumers and patients engaged.

|

| • |

Anticipate potential limits on telemedicine and mail-order by broadening local-pharmacy coverage, using pharmacy couriers where allowed, and supporting in-person prescribing with key physicians.

|

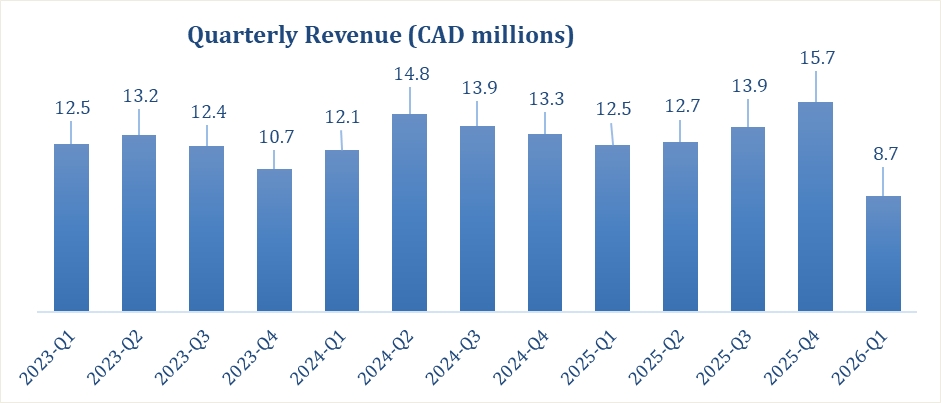

As reflected above, revenue fluctuated during the periods presented. In 2026, the quarterly revenues reflects a decrease compared to 2025, primarily driven by delays in shipments, variations in

product mix, pricing and volume, as well as reduced imports driven in part by cash flow constraints, which negatively impacted sales volumes.

7

|

Management’s Discussion and Analysis

|

|

GEOGRAPHIES AND NEW MARKETS

The Company is a medical cannabis company operating in Germany and Israel, two high-value markets, but highly challenging and rapidly evolving markets. In recent periods, the Company has faced

significant regulatory changes and uncertainty, increased competition, supply constraints, pricing pressures and adverse macro-economic conditions affecting the entire cannabis industry. In addition, geopolitical events and security-related

disruptions in Israel, including recent military operations, have adversely affected logistics, availability of products, patient behavior and the stability of the Israeli market. As a result, the Company's financial position and operating

performance have been negatively impacted, and substantial efforts, restructuring measures and strategic focus are required in order to stabilize and gradually rebuild its business.

With the April 2024 legalization in Germany, we pivoted our focus and resources to this market, leveraging our experience in product sourcing, quality assurance and regulatory compliance to capture

new growth opportunities. However, the German market is still in a formative stage, subject to ongoing regulatory developments and operational uncertainties, including licensing timelines, evolving distribution models and margin pressure. While we

view Germany as a key long-term growth driver, there can be no assurance that our efforts will offset the challenges faced in our legacy markets in the near term.

Israel

As one of the original eight Israeli cannabis pioneers, IMC has built a strong sourcing infrastructure in Israel. We have advanced product knowledge, regulatory expertise, and strong commercial

partnerships. Our extensive experience has made IMC a leading brand within the premium market segment.

We supply the Israeli medical cannabis market with our own IMC-branded products and exclusive ultra-premium Canadian cannabis brands, with which we have signed strategic licensing agreements.

The company also operates in the retail segment. The Company, through IMC Holdings, holds two licensed pharmacies, each selling medical cannabis products to patients: (i) Vironna, a leading pharmacy

in the Arab sector, and (ii) Pharm Yarok, the largest pharmacy in the Sharon Plain area and a big call center in the country (Vironna and Pharm Yarok collectively, the “Israeli Pharmacies”).

In addition, IMC, through IMC Holdings, operates a home delivery service, through a call center, effectively covering the entire country.

Germany

IMC has been operating through Adjupharm, its German subsidiary, since 2019, building the foundation needed to drive growth. We believe that our strong sourcing infrastructure in Israel, powered by

advanced product knowledge and regulatory expertise, gives the Company a competitive advantage in the growing German market. This is based on the premise that the German and Israeli markets share several common attributes such as robust commercial

infrastructure, highly developed digital capabilities, favourable demographics and customer preferences.

8

|

Management’s Discussion and Analysis

|

|

The Company’s focus in Germany is to import cannabis from its supply partners, which are then sold through our own IMC branded products, as well as exclusive ultra-premium Canadian cannabis brands,

with which we have signed strategic licensing agreements.

Our German operations are underpinned by a state-of-the-art warehouse and EU-GMP production facility in Germany (the “German Logistics Center”) with all the

necessary licenses to engage in additional production, cannabis testing, and release activities. Adjupharm can repackage bulk, perform stability studies, and offer such services to third parties.

Following the April 2024 implementation of Germany’s cannabis reform (CanG, comprising KCanG for consumer use and MedCanG for medical use), we have re-allocated resources to the German medical

channel while leveraging operating know-how from Israel. Medical cannabis now falls under MedCanG (with BfArM as the competent authority) rather than the BtMG. We continue to align product specifications with the European Pharmacopoeia 11.5 ‘Cannabis

flos’ monograph effective April 1, 20251.

In September 2025, BfArM temporarily paused new import approvals after Germany’s annual estimate of 122 tonnes for medical cannabis was reached; in late October 2025 authorities increased the

permissible volume (industry reports indicate a ~70-tonne uplift) and resumed approvals. Future adjustments to annual estimates could impact the timing of our import licences and inventory availability. In October 2025, the Federal Cabinet approved a

draft amendment to MedCanG proposing, among other items, an in-person physician visit requirement for prescribing cannabis flowers and a ban on mail-order pharmacy shipment. These proposals are not yet law; if enacted, they could affect patient

access patterns and our distribution mix. We will update our operating plan as the legislative process advances2.

We are updating QA/QC and labelling to Ph. Eur. 11.5, and reviewing licensing needs under MedCanG (import/trade authorisations, and, if pursued, domestic activities under the new cultivation

licensing framework). We are also stress-testing our pharmacy channel strategy to mitigate potential restrictions on telemedicine-origin prescriptions and mail-order fulfilment.

BRANDS

The IMC brand is well-known in the Israeli medical cannabis market, with reputable brands highly popular among Israeli consumers.

Israeli Medical Cannabis Business

The IMC brand has established its reputation in Israel for quality and consistency over the past 15 years and, more recently, with new high-end, ultra-premium strains that have made it to the

top-sellers list in pharmacies nationwide.

The Group maintains a portfolio of strains sold under the IMC umbrella from which popular medical cannabis dried flowers and full-spectrum cannabis extracts are produced.

1

https://www.skwschwarz.de/en/news/the-medical-cannabis-act-at-a-glance-legalization-with-conditions?utm_source=chatgpt.com

2

https://stratcann.com/news/germany-no-new-import-permits-for-dried-cannabis-in-2025/?utm_source=chatgpt.com

9

|

Management’s Discussion and Analysis

|

|

The IMC brand offers different products, leading with the highest-quality Canadian craft cannabis flower, which has established IMC as the leader of the super-premium segment in Israel.

Brands under the IMC Cannabis Portfolio:

The Craft Collection – IMC brand’s premium product line with indoor-grown, hand-dried and hand-trimmed high-THC cannabis flowers. The Craft Collection includes

exotic and unique cannabis strains such as Sup.S and PI.WI.

The Full Spectrum Extracts –IMC brand’s full spectrum, strain-specific cannabis extracts, includes high-THC Roma®T20 oil and OIL GLTO 33.

Roma® Product Portfolio – IMC's Roma® portfolio also includes oils. IMC’s Roma® strain is a high-THC medical cannabis

flower that offers a therapeutic continuum and is known for its strength and longevity of effect.

|

BLKMKT™, the Company’s second Canadian brand. It is a super-premium product line with indoor-grown, hand-dried and hand-trimmed high-THC cannabis

flowers. The BLKMKT™ includes BLK MLK, YA HEMI, PURPLE RAIN, JEALOUSY, Hemi GLTO, RAINBOW P, GUVA BOBA, Sunsets.rudel, Park fire OG, Up side down C and BACLTO.

|

|

LOT420 – this brand launched in Israel in Q2 2023, with super-premium

indoor-grown cannabis imported from Canada with high-THC. The LOT420 brand includes GLTO 33, Apps and Bans, O.C., and GLTO 33 oil. The Company ceased selling Atomic

APP.

The PICO collection (minis)- Under the BLKMKT™ and LOT420 brands, the Company launched in 2023 a new type of product (small flowers), which is a super-premium

indoor-grown cannabis imported from Canada with high-THC. The PICO collection includes the following products: PICO PURPLE RAIN, PICO YA HEMI, PICO JEALOUSY, Pico upside Down, PICO RAIN BOW, Pico California love, PICO BLK MLK and PICO Bacio Glto.

Flower – In Q2 2024, the Company launched a super-premium indoor-grown cannabis imported from Canada with high-THC. The Flower brand includes cannabis strains

called California love and Face Sherb.

Token - New Affordable Lifestyle Line. Launched in Israel and Germany in Q2 2025, TOKEN by IMC introduces a new lifestyle edition offering high-quality,

everyday cannabis at accessible prices such as KEYNAPZ and SIPER.

For more information, see “Strategy in Detail – Brands – New Product Offerings” section of the MD&A.

10

|

Management’s Discussion and Analysis

|

|

German Medical Cannabis Business

In Germany, IMC is positioned among the top cannabis companies. The Group’s competitive advantage in Germany lies in its track record, experience and brand reputation as a reliable partner for

medical cannabis for both pharmacies and patients.

In Germany, IMC initially focused on selling only IMC-branded products, both flowers and full-spectrum extracts, to increase brand awareness and build brand heritage among German healthcare

professionals.

In 2025, IMC expanded its portfolio to include a new mid-market brand “Token” by IMC as well as a new value brand “Mids” by IMC. These two brands join “Selected” by IMC, as well as BLKMKT™, an

ultra-premium Canadian brand.

The Company maintains a portfolio of strains sold under the IMC umbrella from which popular medical cannabis dried flowers and full-spectrum cannabis extracts

are produced.

HIGH-QUALITY,

RELIABLE SUPPLY:

Israel

The Company is concentrating on leveraging its skilled sourcing team and strategic alliances with Canadian suppliers as well as the import of medical cannabis from its Canadian Facilities. The

Company continues to import cannabis products and supply medical cannabis to patients through licensed pharmacies. To supplement growing demand, the Company continues its relationships with third-party cultivation facilities in Israel for the

propagation and cultivation of the Company’s existing proprietary genetics and for the development of new products.

In addition, the Company is operating through its subsidiaries who obtained a license from the IMCA to, among others, import cannabis products and supply medical cannabis to patients.

Pursuant to the applicable Israeli cannabis regulations, following the import of medical cannabis, medical cannabis products are then packaged by contracted GMP-licensed producers of medical

cannabis. The packaged medical cannabis products are then sold by the Group under the Company’s brands to local Israeli pharmacies directly or through contracted distributors.

Germany

The Company continues to expand its presence in the German market by forging partnerships with pharmacies and distributors across the country and developing Adjupharm and its German Logistics Center

as the Company’s European hub. Adjupharm sources its supply of medical cannabis for the German market and from various EU-GMP certified European and Canadian suppliers. The German Logistics Center is EU-GMP certified, upgrading Adjupharm production

technology and increasing its storage capacity to accommodate its anticipated growth. Adjupharm has a certification for primary repackaging, making it one of a handful of companies in Germany fully licenced to repack bulk.

Adjupharm currently holds wholesale, narcotics handling, manufacturing, procurement, storage, distribution, and import/export licenses granted to it by the applicable German regulatory authorities

(the “Adjupharm Licenses”).

11

|

Management’s Discussion and Analysis

|

|

KEY HIGHLIGHTS FOR THE

FIRST QUARTER OF 2026

In the first quarter of 2026, the Company continued to focus on efficiency operations, increasing sales and presence in German cannabis market resulting in accelerated growth in the region while

continuing its sales efforts in the Israeli market. The Company continues with its efforts to establish new supply chain processes and to improve its supplier base for the German market to support the year 2026 goal of profitability. The Company’s

key highlights and events for the first quarter ended March 31, 2026, include:

SUBSEQUENT EVENTS

April Capital Note

On April 6, 2026, the Company entered into a Note Purchase Agreement (the “April 2026 Purchase Agreement”) with the Investor, pursuant to which the Company issued to the Investor (A) a convertible

note (the “April 2026 Note”) in the principal amount of approximately US$250 thousand (approximately $340) (the “April 2026 Note’s Subscription Amount”), which is convertible into the Common Shares, no par value per share, at a purchase price equal

to 90% of the April 2026 Note’s Subscription Amount and (B) a warrant to purchase up to 272,861 Common Shares (the “April 2026 Warrant”), which is the number equal to thirty-three and one-third percent (331/3%) of the April 2026 Note’s Subscription Amount divided by an exercise price of $0.47 per Common Share. Such transaction

closed on April 6, 2026.

The April 2026 Note bears an interest rate of eight percent (8.0%) per annum accruing from its closing date (which shall increase to fourteen percent (14.0%) upon the occurrence of an Event of

Default (as defined in the April 2026 Note). The April 2026 Note is not repayable in cash and the Company’s obligations thereunder will be satisfied solely through the issuance of Common Shares upon conversion of the Note in accordance with its

terms.

The number of Common Shares issuable upon any conversion of the principal amount under the April 2026 Note is determined by dividing the applicable conversion amount by its conversion price. The

conversion price of the April 2026 Note is equal to the lower of (i) the fixed price, as defined in the April 2026 Note, or (ii) its variable price, which equals to ninety percent (90%) of the lowest daily volume-weighted average price of the Common

Shares during the twenty (20) consecutive trading days immediately preceding the conversion date, provided, however, that such variable price will not be lower than the floor price, as defined in the April 2026 Note. The fixed price set in the April

2026 Note is $0.339. The floor price set in the April 2026 Note is $0.07. No fractional Common Shares will be issued upon conversion, and any fractional amount will be rounded to the nearest $0.0001. Any fractional Common Shares will be rounded down

to the nearest whole share.

The April 2026 Warrant entitles its holder to purchase one Common Share (each, a “warrant share”) at an exercise price of $0.47 per such warrant share. The April 2026 Warrant became exercisable

immediately upon its issuance date, April 6, 2026, and will be exercisable for a period of five (5) years, until April 6, 2031. If the Warrant is not exercised by its termination date, April 6, 2031, the April 2026 Warrant will expire and be of no

further force or effect. The April 2026 Warrant and the warrant shares may not be traded for a period of four (4) months, unless permitted under applicable securities legislation.

The April 2026 Note includes customary limitations on conversion, including a beneficial ownership cap of 4.99% of the outstanding Common Shares after giving effect to such conversion.

12

|

Management’s Discussion and Analysis

|

|

The April 2026 Purchase Agreement include customary representations, warranties and covenants of the Company and the Investor, including the Company’s obligation to reserve sufficient Common Shares

for issuance upon conversion of the Notes and to file a resale Registration Statement with the SEC providing for the resale by the Investor of the Common Shares and the warrant shares issuable upon conversion of the April 2026 Note within thirty (30)

trading days after the applicable closing date. The Company has also agreed to use commercially reasonable efforts to cause the Registration Statement to become effective as soon as possible, but in no event later than the date which shall be the

earlier of: (x) in the event that the Registration Statement is not subject to a full review by the SEC, sixty (60) calendar days after the applicable closing date, or in the event that the Registration Statement is subject to a full review by the

SEC, ninety (90) calendar days after the applicable closing date, and (y) the fifth (5th) business day after the date on which the Company is notified (orally or in writing, whichever is earlier) by the SEC that such Registration Statement will not

be reviewed or will not be subject to further review.

May Capital Note

On May 7, 2026, entered into a Note Purchase Agreement (the “May 2026 Purchase Agreement”) with the Investor, pursuant to which the Company issued to the Investor (A) a convertible note (the “May

2026 Note”) in the principal amount of US$300,000 (the “May 2026 Subscription Amount”), which is convertible into the Common Shares, no par value per share, at a purchase price equal to ninety percent (90%) of the May 2026 Subscription Amount; and

(B) a warrant to purchase up to 1,127,820 Common Shares (the “May 2026 Warrant”), equal to a number of Common Shares determined by one hundred percent (100%) of the May 2026 Subscription Amount divided by an exercise price of $0.36 per Common Share.

Such offering closed on May 7, 2026. The Company intends to use the net proceeds of US$270,000 received from such offering for general corporate purposes.

The May 2026 Note bears an interest rate of eight percent (8.0%) per annum accruing from its closing date (which shall increase to fourteen percent (14.0%) upon the occurrence of an Event of Default

(as defined in the May 2026 Note). The May 2026 Note is not repayable in cash and the Company’s obligations thereunder will be satisfied solely through the issuance of Common Shares upon conversion of the May 2026 Note in accordance with its terms.

The number of Common Shares issuable upon any conversion of the principal amount under the May 2026 Note is determined by dividing the applicable conversion amount by its conversion price. The

conversion price is equal to the lower of (i) the fixed price, as defined in the May 2026 Note, or (ii) its variable price which equals to ninety percent (90%) of the lowest daily volume-weighted average price of the Common Shares during the twenty

(20) consecutive trading days immediately preceding the conversion date, provided, however, that such variable price will not be lower than the floor price, as defined in the May 2026 Note. The fixed price set in the May 2026 Note is $0.266. The

floor price set in the Note $0.05. No fractional Common Shares will be issued upon conversion, and any fractional amount will be rounded to the nearest $0.0001. Any fractional Common Shares will be rounded down to the nearest whole share.

The May 2026 Warrant entitles its holder to purchase one Common Share (each, a warrant share) at an exercise price of $0.36 per warrant share. The May 2026 Warrant became exercisable immediately upon

its issuance date, May 7, 2026, and will be exercisable for a period of five (5) years, until May 7, 2031. If the Warrant is not exercised by its termination date, May 7, 2031, the May 2026 Warrant will expire and be of no further force or effect.

The May 2026 Warrant and the warrant shares may not be traded for a period of four (4) months, unless permitted under applicable securities legislation.

The May 2026 Note includes customary limitations on conversion, including a beneficial ownership cap of 4.99% of the outstanding Common Shares after giving effect to such conversion.

13

|

Management’s Discussion and Analysis

|

|

The May 2026 Purchase Agreement include customary representations, warranties and covenants of the Company and the Investor, including the Company’s obligation to reserve sufficient Common Shares for issuance upon

conversion of the May 2026 Notes and to file a resale Registration Statement with the SEC providing for the resale by the Investor of the Common Shares and the warrant shares issuable upon conversion of the May 2026 Note within thirty (30)

trading days after the applicable closing date. The Company has also agreed to use commercially reasonable efforts to cause the Registration Statement to become effective as soon as possible, but in no event later than the date which shall be

the earlier of: (x) in the event that the Registration Statement is not subject to a full review by the SEC, sixty (60) calendar days after the applicable closing date , or in the event that the Registration Statement is subject to a full

review by the SEC, ninety (90) calendar days after the applicable closing date, and (y) the fifth (5th) business day after the date on which the Company is notified (orally or in writing, whichever is earlier) by the SEC that such Registration

Statement will not be reviewed or will not be subject to further review.

Other Loan Agreements

On April, 2026, IMC Holdings entered into a loan agreement with the Company's Chief Executive Officer and main shareholder, in the amount of NIS 725 thousand (approximately $333) which bears fixed

annual interest at the rate prescribed by the Income Tax Regulations for determining the interest rate under Section 3(i) of the Income Tax Ordinance and shall be repaid by August, 2026.

On April, 2026, IMC Holdings entered into loan agreements with a relative of one of the Company's main shareholders, in total amount of NIS 1,250 thousand (approximately $573). As of the date of this

report the loan terms have not yet been set.

Share Issuances

During the period between April 1 to May 13, 2026, the Company issued 2,793,216 Common Shares in respect of conversion of convertible notes in the amount of US$839 (approximately $1,141) at an

average exercise price of US$0.3004 per share.

14

|

Management’s Discussion and Analysis

|

|

REVIEW

OF FINANCIAL PERFORMANCE

FINANCIAL HIGHLIGHTS

Below is the analysis of the changes that occurred for the three months ended March 31, 2025, with further commentary provided below.

|

For the three months ended

March 31

|

For the year ended

December 31

|

|||||||||||

|

2026

|

2025

|

2025

|

||||||||||

|

Net Revenues

|

$

|

8,679

|

$

|

12,500

|

$

|

54,731

|

||||||

|

Gross profit before fair value impacts in cost of sales

|

$

|

1,419

|

$

|

3,448

|

$

|

9,686

|

||||||

|

Gross margin before fair value impacts in cost of sales (%)

|

16

|

%

|

28

|

%

|

18

|

%

|

||||||

|

Operating Profit (Loss)

|

$

|

(1,676

|

)

|

$

|

158

|

$

|

(11,587

|

)

|

||||

|

Net Profit (Loss)

|

$

|

(2,467

|

)

|

$

|

175

|

$

|

(11,750

|

)

|

||||

|

Loss per share attributable to equity holders of the Company – Basic (in CAD)

|

$

|

(0.38

|

)

|

$

|

0.09

|

$

|

(2.67

|

)

|

||||

|

Loss per share attributable to equity holders of the Company - Diluted (in CAD)

|

$

|

(0.38

|

)

|

$

|

0.09

|

$

|

(2.67

|

)

|

||||

The Overview of Financial Performance includes reference to “Gross Margin”, which is a non-IFRS financial measure that the Company defines as the difference between revenue and cost of revenues

divided by revenue (expressed as a percentage), prior to the effect of a fair value adjustment for inventory and biological assets. For more information on non-IFRS financial measures, see the “Non-IFRS Financial

Measures” and “Metrics and Non-IFRS Financial Measures” sections of the MD&A.

OPERATIONAL RESULTS

In each of the markets in which the Company operates, it must navigate evolving customer and patient trends to remain competitive with other suppliers of medical cannabis products.

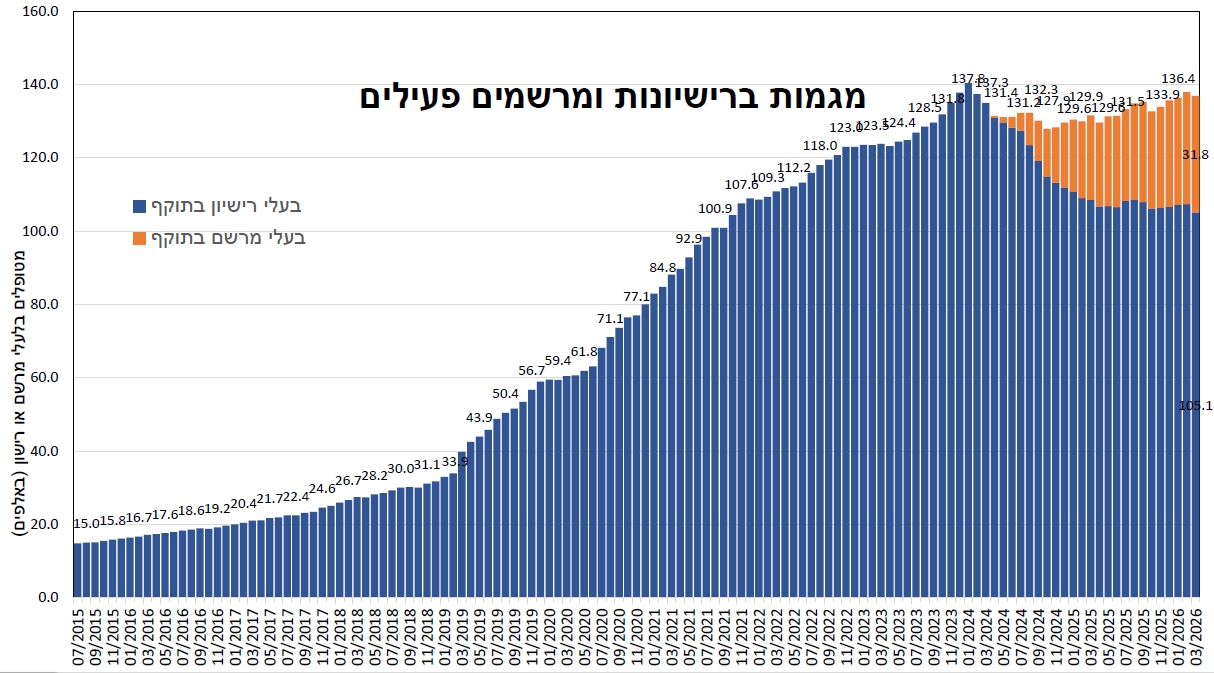

The Company believes several key factors create tailwinds to facilitate further industry growth. In Israel, the number of medical patients currently stands at 136,900 out of which – 105,100 with

licenses and 31,800 with prescriptions as of March 2026. This figure is expected to grow in the coming years and may further benefit from regulatory changes liberalizing the cannabis market in Israel. IM Cannabis is a large distributor of medical

cannabis in Israel.

|

Germany Region Revenue for the three months ended

|

||||||||||||||||||||

|

2026

|

2025

|

|||||||||||||||||||

|

March 31,

|

December 31,

|

September 30

|

June 30,

|

March 31,

|

||||||||||||||||

|

Revenue for the period

|

$

|

4,278

|

$

|

13,073

|

$

|

8,768

|

$

|

6,802

|

$

|

7,705

|

||||||||||

|

Q vs Q change%

|

(67

|

)%

|

49

|

%

|

29

|

%

|

(12

|

)%

|

-

|

|||||||||||

The Company's products are in high demand in the German market, and it is investing efforts in building a strong, high-volume supply chain to support its current operation and future growth in the

country. The decreased revenue in the three months ended March 31, 2026, compared to the three months ended December 31, 2025, is due to delays in shipments, variations in product mix, pricing and volume, as well as reduced imports driven in part by

cash flow constraints, which negatively impacted sales volumes.

15

|

Management’s Discussion and Analysis

|

|

REVENUES

The following table summarizes the Company’s revenues for the periods presented. The period-to-period comparison of results is not necessarily indicative of results for future periods.

For the three months ended March 31:

|

CAD in thousands

|

Israel

|

Germany

|

Adjustments

|

Total

|

||||||||||||||||||||||||||||

|

For the Three Months Ended

March 31,

|

For the Three Months Ended

March 31,

|

For the Three Months Ended

March 31,

|

For the Three Months Ended

March 31,

|

|||||||||||||||||||||||||||||

|

2026

|

2025

|

2026

|

2025

|

2026

|

2025

|

2026

|

2025

|

|||||||||||||||||||||||||

|

Revenue

|

$

|

4,401

|

$

|

4,795

|

$

|

4,278

|

$

|

7,705

|

$

|

-

|

$

|

-

|

$

|

8,679

|

$

|

12,500

|

||||||||||||||||

|

Segment income (loss)

|

$

|

(575

|

)

|

$

|

111

|

$

|

(720

|

)

|

$

|

577

|

$

|

-

|

$

|

-

|

$

|

(1,295

|

)

|

$

|

688

|

|||||||||||||

|

Unallocated corporate expenses

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

-

|

$

|

(381

|

)

|

$

|

(530

|

)

|

$

|

(381

|

)

|

$

|

(530

|

)

|

||||||||||||

|

Total operating income (loss)

|

$

|

(575

|

)

|

$

|

111

|

$

|

(720

|

)

|

$

|

577

|

$

|

(381

|

)

|

$

|

(530

|

)

|

$

|

(1,676

|

)

|

$

|

158

|

|||||||||||

|

Depreciation, amortization and impairment

|

$

|

442

|

$

|

439

|

$

|

55

|

$

|

24

|

$

|

-

|

$

|

-

|

$

|

497

|

$

|

463

|

||||||||||||||||

The Company’s consolidated revenues for the three months ended March 31, 2026, were attributed mostly to the sale of medical cannabis products in Israel and Germany. Revenue in Germany reflects

demand trends, product availability and import volumes during the periods presented.

Revenues for the three months ended March 31, 2026, and 2025 were $8,679 and $12,500, respectively, representing a decrease of $3,821, or 31%. The decrease was primarily attributable to a decrease in

revenue in Germany of $3,427 due to delays in shipments, and a decrease of $394 in revenue in Israel, reflecting variations in product mix, pricing and volume as well as reduced imports driven in part by cash flow constraints, which negatively

impacted sales volumes.

16

|

Management’s Discussion and Analysis

|

|

COST

OF REVENUES

The cost of revenues is comprised of the purchase of raw materials and finished goods, import costs, production costs, product laboratory testing, shipping, and salary expenses. When sold, inventory

is later expensed to the cost of sales. Direct production costs are also expensed through the cost of sales.

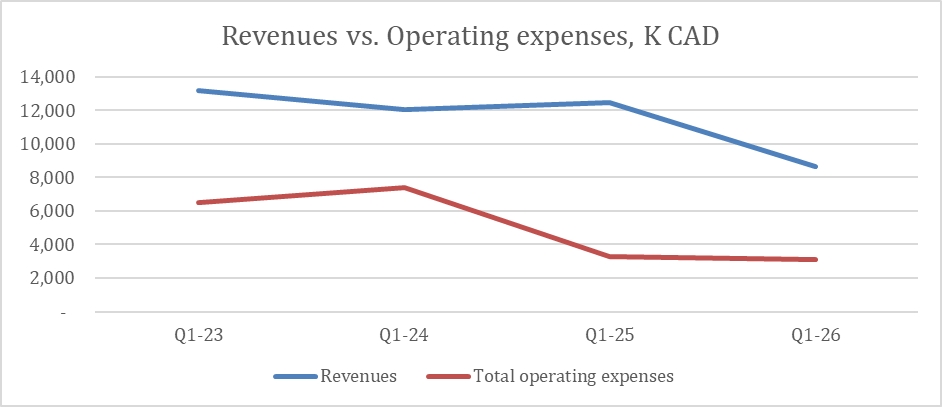

The cost of revenues for the three months ended March 31, 2026, and 2025 were $7,260 and $9,052, respectively, representing a decrease of $1,792, or 20%. The decrease was primarily attributable to

the decrease in revenues.

GROSS PROFIT

Gross profit for the three months ended March 31, 2026, and 2025 was $1,419 and $3,448, respectively, representing a decrease of $2,029, or 59%.

GENERAL AND ADMINISTRATIVE

General and administrative expenses for the three months ended March 31, 2026, and 2025 were $1,569 and $2,009, respectively, representing a decrease of $440 or 22%.

The decrease in general and administrative expenses for the three months ended March 31, 2026 was primarily attributable to lower insurance costs, reduced salaries and related expenses, and lower

other administrative expenses, partially offset by increased professional fees associated with financing activities, legal matters and corporate initiatives.

Insurance costs decreased by $423 to $(120) for the three months ended March 31, 2026, compared to $303 for the comparable prior-year period, due to a refund received. Salaries and related expenses

decreased by $165 to $411 for the three months ended March 31, 2026, compared to $576 for the comparable prior-year period. Other administrative expenses decreased by $88 to $467 for the three months ended March 31, 2026, compared to $555 for the

comparable prior-year period. These decreases were partially offset by an increase in professional fees of $233 to $696 for the three months ended March 31, 2026, compared to $463 for the comparable prior-year period.

SELLING AND MARKETING

Selling and marketing expenses for the three months ended March 31, 2026, and 2025 were $1,526 and $1,273, respectively, representing an increase of $253 or 20%.

The increase in sales and marketing expenses for the three months ended March 31, 2026 was primarily attributable to (i) an increase in selling and marketing expenses of $125 ($190 in 2026 compared

to $65 in 2025), and (ii) an increase in professional fees of $74 ($77 in 2026 compared to $3 in 2025).

OTHER

OPERATING EXPENSES

Other operating expenses for the three months ended March 31, 2026, and 2025 were $nil and $nil, respectively.

17

|

Management’s Discussion and Analysis

|

|

SHARE-BASED COMPENSATION

Share-based compensation expenses for the three months ended March 31, 2026, and 2025 were $nil and $8, respectively, representing a decrease of $8 or 100%.

OPERATING EFFICIENCY AND

OPERATING RATIO

The operating expense ratio for the three months ended March 31, 2026, and 2025, were 36% and 26% respectively, representing a decrease in efficiency of approximately 35%. The efficiency ratio

decline resulted from decreased revenues.

FINANCING

INCOME (EXPENSE), NET

Financing (expense) net for the three months ended March 31, 2026 and 2025 was $(832) and $(12) respectively, representing an increase in financing expense of $820.

NET

INCOME (LOSS) PER SHARE BASIC AND DILUTED

Net loss for the three months ended March 31, 2026 was $2,467 compared to a net income of $175 for the three months ended March 31, 2025, representing an increase in net loss of $2,642. The increase

in net loss primarily reflected lower revenues, reduced gross profit and increased financing expenses during the quarter.

Basic income or loss per share is calculated by dividing the net income attributable to holders of Common Shares by the weighted average number of Common Shares outstanding during the period. Diluted

income or loss per Common Share is calculated by adjusting the earnings and number of Common Shares for the effects of dilutive warrants and other potentially dilutive securities. The weighted average number of Common Shares used as the denominator

in calculating diluted income or loss per Common Share excludes unissued Common Shares related to Options as they are anti-dilutive.

18

|

Management’s Discussion and Analysis

|

|

Basic Income or (Loss) per Common Share for the three months ended March 31, 2026, and 2025 were $(0.38) and $0.09 per Common Share, respectively.

Diluted net Income or (Loss) per share for the three months ended March 31, 2026, and 2025 were $(0.38) and $0.09, respectively.

TOTAL ASSETS

Total assets as of March 31, 2026, and December 31, 2025 were $23,701 and $31,736, respectively, representing a decrease of $8,035 or 25%. The decrease is mainly attributed to a decrease in trade

receivables of $3,681, and to a decrease of $2,267 in inventory.

Investment in Xinetza

On December 26, 2019, IMC Holdings entered into a Share Purchase Agreement with Xinteza API Ltd. (“Xinteza”), under which IMC Holdings invested an aggregate amount of US$1,700 (approximately $2,468)

in exchange for the issuance of 38,082 preferred shares of Xinteza.

On February 24, 2022, IMC Holdings entered into a Simple Agreement for Future Equity with Xinteza, under which IMC Holdings invested US$100 (approximately $125), in exchange for additional future

shares of Xinteza.

As of December 31, 2025, IMC Holdings holds 25.32% of the voting rights of Xinteza and has the right for two members of the Board of Directors out of five. However, it was determined that the

economic interests of the preferred shares are not substantially identical to those of ordinary shares (due to such features as liquidation preference and redemption feature). Accordingly, since the preferred shares do not meet the ordinary equity

ownership interest criteria, the equity method is not applicable, and the investment in Xinteza is subject to the provisions of IFRS 9 and is accounted for as a financial asset measured at fair value through profit or loss categorized within Level 3

of the fair value hierarchy.

As of March 31, 2026, and December 31, 2025, the investment in an affiliate amounted to $1,819 and $1,776, respectively, due to an effect of foreign currency translation of $43.

TOTAL LIABILITIES

As of March 31, 2026, total liabilities were $28,825, compared to $35,351 as of December 31, 2025. The change was primarily attributable to changes in trade payables, bank borrowings, convertible

instruments and other financial liabilities.

As of March 31, 2026, total borrowings and credit from financial and non-financial institutions amounted to $11,495, compared to $15,269 as of December 31, 2025.

19

|

Management’s Discussion and Analysis

|

|

As of March 31, 2026 and December 31, 2025, the Company’s borrowings consisted of:

|

2026

|

2025

|

|||||||

|

Credit from bank institutions

|

$

|

1,109

|

$

|

1,067

|

||||

|

Credit from non-financial institutions

|

8,952

|

9,696

|

||||||

|

Check receivables

|

1,434

|

4,506

|

||||||

|

Total borrowings

|

$

|

11,495

|

$

|

15,269

|

||||

Since the Company’s inception through March 31, 2026, the Company has funded its operations through raising capital, inter alia, through public offering, non-broker private placement transactions and

credits from bank institutions and others.

The Company’s liquidity is affected by the timing of customer collections, inventory turnover and payment terms with suppliers.

As of March 31, 2026, the Company’s cash and restricted cash totaled $1,152 and the Company’s working capital deficit (current assets minus current liabilities) amounted to $12,602. For the three

months ended March 31, 2026, the Company had an operating loss of ($1,676) and cash flows used in operating activities of $186.

As of March 31, 2026, the Company’s financial liabilities were $28,825, which included trade payables, other payables and accrued expenses, borrowings and other financial liabilities, a substantial

portion of which had contractual maturities of less than one year.

The Company manages its liquidity risk by reviewing its capital requirements on an ongoing basis. Based on the Company’s working capital position on March 31, 2026, management considers liquidity

risk to be high. As of March 31, 2026, the Company has identified the following liquidity risks related to financial liabilities:

|

Less than one year

|

1 to 5 years

|

6 to 10 years

|

> 10 years

|

|||||||||||||

|

Contractual Obligations

|

$

|

10,949

|

$

|

860

|

$

|

-

|

$

|

-

|

||||||||

The maturity profile of the Company’s other financial liabilities (trade payables, other account payable and accrued expenses, and warrants) as of March 31, 2026, are less than one year.

|

Payments Due by Period

|

||||||||||||||||||||

|

Contractual Obligations

|

Total

|

Less than one year

|

1 to 3 years

|

4 to 5 years

|

After 5 years

|

|||||||||||||||

|

Debt

|

$

|

11,495

|

$

|

10,710

|

$

|

785

|

$

|

-

|

$

|

-

|

||||||||||

|

Finance Lease Obligations

|

$

|

314

|

$

|

239

|

$

|

75

|

$

|

-

|

$

|

-

|

||||||||||

|

Total Contractual Obligations

|

$

|

11,809

|

$

|

10,949

|

$

|

860

|

$

|

-

|

$

|

-

|

||||||||||

20

|

Management’s Discussion and Analysis

|

|

As of December 31, 2026 and 2025, the Company’s financial liabilities were $28,825 and $35,351, respectively.

As of March 31, 2026 and December 31, 2025, the Company did not have any distributions or cash dividends declared per-share for the outstanding Common Shares.

The Company’s current operating budget includes various assumptions concerning the level and timing of cash receipts from sales and cash outflows for operating expenses and capital expenditures,

including cost saving plans. In 2023, the Board approved a cost saving plan, to allow the Company to continue its operations and meet its cash obligations. The cost saving plan entailed reducing costs through efficiencies and synergies primarily

involving the following measures: discontinuing loss-making activities, reducing payroll and headcount, reduction in compensation paid to key management personnel (including layoffs of key executives), operational efficiencies and reduced capital

expenditures. These actions resulted in cost savings during 2024 and 2025, and the Company will continue its efforts for efficiency operations also during 2026.

The projected cash flow for the rest of 2026 indicates that there is uncertainty regarding whether the Company will generate sufficient funds to continue its operations and meet its obligations as

they become due. The Company continues to evaluate additional sources of capital and financing. However, there is no assurance that additional capital and or financing will be available to the Group, and even if available, whether it will be on terms

acceptable to the Group or in amounts required.

These conditions raise substantial doubt about the Company’s ability to continue as a going concern. The interim consolidated financial statements included do not include any adjustments relating to

the recoverability and classification of assets or liabilities that might be necessary should the Company be unable to continue as a going concern.

The interim consolidated financial statements included have been prepared on the basis of accounting principles applicable to a going concern, which assumes that the Company will continue in

operation for the foreseeable future and will be able to realize its assets and discharge its liabilities in the normal course of operations. The interim consolidated financial statements do not include any adjustments to the amounts and

classification of assets and liabilities that would be necessary should the Company be unable to continue as a going concern. Such adjustments could be material.

SOURCES

OF LIQUIDITY AND FINANCING ARRANGEMENTS

The Company’s primary sources of liquidity consist of cash generated from operations, borrowings under credit facilities, private placements of equity securities and convertible instruments, and

short-term financing arrangements with financial and non-financial institutions.

As of March 31, 2026, the Company had cash and restricted cash of $1,152. The Company continues to rely on external financing arrangements to support working capital needs and to fund operations.

and capital resources.

21

|

Management’s Discussion and Analysis

|

|

Revolving Credit Facility with Bank Mizrahi

On March 23, 2022, Focus entered into a revolving credit facility with an Israeli bank, Bank Mizrahi (the “Mizrahi Facility”). The Mizrahi Facility is

guaranteed by Focus assets. Advances from the Mizrahi Facility were used for working capital needs. The Mizrahi Facility had a total commitment of up to NIS 15,000 (approximately $6,000) and had a one-year term for on-going needs and 6 months term

for imports and purchases needs. The Mizrahi Facility is renewable upon mutual agreement by the parties. The borrowing base available for draw at any time throughout the Mizrahi Facility and is subject to several covenants to be measured on a

quarterly basis. The Mizrahi Facility bears interest at the Israeli Prime interest rate plus 1.5%.

On May 17, 2023, the Company and Bank Mizrahi entered into a new credit facility with total commitment of up to NIS 10,000 (approximately $3,600) (the “New Mizrahi

Facility”). The New Mizrahi Facility consists of NIS 5,000 credit line and NIS 5,000 loan to be settled with twenty-four (24) monthly installments from May 17, 2023. This loan bears interest at the Israeli Prime interest rate plus 2.9%.

On August 1, 2024, the credit line of approximately NIS 1,825 related to the New Mizrahi Facility was converted into a six-month short-term loan, bearing an annual variable interest rate of P+1.9%

(with the Israel Prime interest rate as of the submission date being 6%).

As of December 31, 2024, Focus had a short-term loan of $2,586 in respect of the new Mizrahi facility. The New Credit facility is also subject to several covenants to be measured on a quarterly basis

which were not met as of December 31, 2024.

As of March 20, 2025, Mizrahi Bank has been extending the short-term loan on a weekly basis; however, on March 20, 2025, the bank and the company signed an agreement modifying the New Mizrahi

Facility terms as follows:

| • |

$1,560 (NIS 4 million) was extended as a loan with a six-month grace period, after which repayment will be made in 31 monthly installments commencing on September 10, 2025. The principal loan will not require a personal guarantee and will

bear an interest at a rate of P+2.9% to be paid monthly, commencing on April 20, 2025.

|

| • |

The remaining $390 (NIS 1 million) was extended as a credit line from March 19, 2025, to March 12, 2026. As of the date of this report, the credit line has been extended to September 25, 2026.

|

Mr. Oren Shuster, the Company’s Chief Executive Officer and director provided the bank with a personal guarantee for the outstanding borrowed amount, allowing the New Mizrahi Facility to remain

effective.

On June 29, 2025, the Mizrahi Facility approved to postpone by one month the first loan installment of the principal amount (only and not the interest) from September 21, 2025, to October 21, 2025,

which was paid in full on time.

On April 29, 2025, IMC Holdings entered into a short-term loan agreement with a non-financial institution in the amount of NIS 1,000 (approximately $375). This loan bears interest at an annual rate

of 17% and matures 12 months from the date of signing the loan agreement.

22

|

Management’s Discussion and Analysis

|

|

Loan and Repayment to ADI

On October 11, 2022, IMC Holdings entered into a loan agreement with A.D.I. Car Alarms Stereo Systems Ltd (“ADI” and the “ADI

Agreement”), to borrow a principal amount of NIS 10,500 (approximately $4 million) at an annual interest of 15% (the “ADI Loan”), which was to be repaid within 12 months of the date of the ADI

Agreement. The ADI Loan was secured by a second rank land charge on the German Logistics Center. In addition, Mr. Oren Shuster, the Company’s Chief Executive Officer and director, provided a personal guarantee to ADI should the security not be

sufficient to cover the repayment of the ADI Loan.

On October 25, 2023, IMC Holdings and ADI signed an amendment to the ADI Agreement, extending the loan period by an additional 3 months. During this extended period, the interest rate was 15%, with

associated fees and commissions of 3% per annum for the application fee and an origination fee of 3% per annum. On February 26, 2024, IMC Holdings and ADI signed an additional amendment to the ADI Agreement, extending the loan period until April 15,

2024, with the same terms as the first amendment, as specified above.

On March 5, 2025, IMC Holdings and ADI signed an amendment postponing the repayment of the remaining ADI Loan to June 30, 2025. The Company repaid NIS 6 million (approximately $2,575) of the

outstanding balance of the ADI Loan by using the proceeds from the November 2024 Offering (defined below). The parties are currently in discussions about the repayment of the outstanding balance of the ADI Loan.

April 2024 Loan Agreement

On April 17, 2024, Pharm Yarok entered into a loan agreement with a non-financial institution in the amount of NIS 3,000 (approximately $1,082) (the “April 2024 Loan”).

The April 2024 Loan bore an annual interest rate of 15% and matured 12 months from the date of issuance. The April 2024 Loan was secured by the following collaterals and guarantees: (a) a first-ranking floating charge over the assets of Pharm Yarok

(b) a first-ranking fixed charge over the holdings (23.3%) of its subsidiary, IMC Holdings, of Xinteza; (c) a personal guarantee by Mr. Oren Shuster, the Company’s Chief Executive Officer and director; and (D) a guarantee by the Company.

On January 30, 2025, Pharm Yarok and the lender signed an amendment to the April 2024 Loan pursuant to which Pharm Yarok paid NIS 1,000 (approximately $393) on January 31, 2025, and the remaining

loan principal amount of NIS 2,000 (approximately $844) was extended until June 30, 2026.

May 2024 Convertible Debenture Offering

On May 26, 2024, the Company closed a non-brokered private placement (the “May 2024 Private Placement”) of secured convertible debentures (each, a “May 2024 Debentures”) for aggregate proceeds of $2,092. The May 2024 Debentures were issued to holders of short-term loans and obligations owed by the Company or its wholly owned subsidiaries and were inclusive of

a 10% extension fee in full settlement of such debt to the holders. The May 2024 Debentures matured on May 26, 2025 and have not incurred interest. The May 2024 Debentures were convertible into Common Shares at a conversion price of $5.1 per Common

Share (following the July 2024 Consolidation). The Company was entitled through the term of the May 2024 Debentures to early repayment of the May 2024 Debentures for cash amount of $2,092. Mr. Oren Shuster, the Company’s Chief Executive Officer and

director, subscribed for an aggregate of $237 of May 2024 Debentures in the May 2024 Private Placement.

Effective May 26, 2025, following the shareholders' approval, the Company and the creditors agreed to extend the term of the May 2024 Debentures until May 25, 2026, subject to extension fee of

additional 10%, such that upon maturity of the May 2024 Debentures, the principal to be paid will be $2,301. The conversion price was determined as $2.61 per Common Share and the Company was entitled to through the term of the May 2024 Debentures to

early repayment of the May 2024 Debentures for cash amount of $2,301.

23

|

Management’s Discussion and Analysis

|

|

July 2024 Short-term Loan Agreement

On July 1, 2024, IMC Holdings entered into a short-term loan agreement with a non-financial institution in the amount of NIS 3,000 (approximately $1,113). Such loan bore interest at an annual rate of

12% and originally matured 62 days from the date of signing the loan agreement. IMC Holdings and the lender executed amendments to the loan agreement, each extending the maturity date, thereby postponing the

maturity date to February 28, 2026, under the same terms and conditions. The loan, including the accrued interest, was fully paid by February 28, 2026.

Payment schedule with third party

On July 30, 2024, the Company entered into an acknowledgment and payment schedule agreement with a third party regarding unpaid fees, charges, and disbursements for services rendered to us. According

to the terms of the agreement, we shall pay $54,000 on the first business day of each month for twenty-four (24) months, with the first payment due on November 1, 2024.

April 2025 Short-Term Loan Agreement

On April 29, 2025, IMC Holdings entered into a short-term loan agreement with a non-financial institution in the amount of NIS 1,000 (approximately $375). The loan bears interest at an annual rate of

17% and matures 12 months from the date of signing the loan agreement.

May 2025 Short-Term Loan Agreement

On May 25, 2025, IMC Holdings entered into a short-term loan agreement with a non-financial institution in the amount of NIS 350 (approximately $131). This loan bears interest at an annual rate of

17% and matures on June 25, 2025. The parties extended the maturity date to June 25, 2026.

July 2025 Loan Agreement

On July 6, 2025, the Company entered into a loan agreement with L.I.A. Pure Capital Ltd. (the “Lender”) for an aggregate amount of US$2 million. Pursuant to

the Loan Agreement, the Company received an amount of US$1 million (the “First Loan Tranche”) and may receive an additional amount of US$1 million (the “Second Loan Tranche”)

no later than 60 days from signing the Loan Agreement, subject to satisfying certain conditions. Pursuant to the Loan Agreement, the Lender has a right to recommend a director to be appointed to the Company’s Board.

The loan bears annual interest at a rate of 8% (plus VAT) and is repayable in full, including accrued interest, by June 30, 2026. In the event of non-repayment by that date, default interest at a

rate of 15% per annum (plus VAT) will apply. The loan is secured by a pledge over 100% of the shares of IMC Holdings Ltd., the Company’s wholly owned subsidiary, with the pledged shares held directly by us.

The Company has also committed to raise at least US$ 3 million in capital within 60 days of signing the Loan Agreement, through a public offering underwritten or distributed by Aegis Capital Corp. If

the Company raises US$4 million or more, the Lender will not be obligated to provide the second loan tranche. In the event that the Company raises US$5 million or more, the Lender may exercise an acceleration right, requiring the Company to repay the

outstanding loan within 45 business days of written notice.

24

|

Management’s Discussion and Analysis

|

|

July 2025 Short-Term Loan Agreement

On July 16, 2025, Rosen High Way entered into a short-term loan agreement, with a non-financial institution in the amount of NIS 500 (approximately $202). This loan bears interest at an annual rate

of 17% and matures on July 16, 2026.

October 2025 Short-Term Loan Agreement

On October 5, 2025, IMC Holdings entered into a short-term loan agreement with a non-financial institution in the amount of NIS 500 (approximately $211). This loan bears interest at an annual rate of

17% and matured on November 13, 2025. The Company is currently in discussions with the lender regarding a potential extension of the loan.

January 2026 Note Purchase Agreements, Convertible Notes and Warrants

On January 7, 2026, the Company entered into a Note Purchase Agreement (the “Purchase Agreement”) with an institutional investor (the “Investor”), pursuant to which the Company issued to the Investor: (A) a convertible note (the “Note”) in the principal amount of US$1,710 (the “Subscription Amount”), which is convertible into the Company’s Common Shares at a price equal to ninety percent (90%) of the Subscription Amount and (B) a warrant to purchase up to 228,150 Common Shares, which is the number equal to

thirty-three and one-third percent (33⅓%) of the Subscription Amount divided by an exercise price of $3.45 per Common Share (the “First Transaction”). The First Transaction closed on January 20, 2026.

In addition, on January 20, 2026, the Company entered into an additional Note Purchase Agreement (the “Additional Purchase Agreement” and, together with the

Purchase Agreement, the “Purchase Agreements”) with the Investor, pursuant to which the Company issued to the Investor: (A) a convertible note (the “Second Note” and,

together with the Note, the “Notes”) in the principal amount of US$703 (the “Additional Subscription Amount” and, together with the Subscription Amount, the “Subscription Amounts”) which is convertible into Common Shares at a price equal to 90% of the Additional Subscription Amount and (B) a warrant to purchase up to 93,671 Common Shares, which is the number equal to

thirty-three and one-third percent (33⅓%) of the Additional Subscription Amount divided by an exercise price of $3.45 per Common Share (the “Second Transaction” and, together with the First Transaction, the “Offerings”). The Second Transaction closed on January 21, 2026.

The Company intends to use the net proceeds of $2,172 received from the Offerings for debt repayment and general corporate purposes.

25

|

Management’s Discussion and Analysis

|

|

Each Note bears an interest rate of 8.0% per annum accruing from the closing date of the First Transaction and the Second Transaction, as applicable, (which shall increase to 14.0% upon the

occurrence of an Event of Default, as defined in the Notes). The Notes are not repayable in cash and the Company’s obligations thereunder will be satisfied solely through the issuance of the Company’s Common Shares upon conversion of the Notes in

accordance with their terms.

The number of Common Shares issuable upon any conversion of principal amount under the Notes is determined by dividing the applicable conversion amount by the conversion price (the “January 2026 Notes Conversion Price”). The January 2026 Notes Conversion Price is equal to the lower of (i) the Fixed Price, as

defined in each of the Notes, or (ii) 90% of the lowest daily volume-weighted average price of the Common Shares during the 20 consecutive trading days immediately preceding the conversion date, (the “January 2026

Notes Variable Price”), provided, however, that the January 2026 Notes Variable Price will not be lower than the Floor Price, as defined in each of the Notes.

The Fixed Price in the Note and in the Second Note is $0.29 and $1.38, respectively. The Floor Price in the Note and in the Second Note is $0.29 and $0.275, respectively.

The warrants entitle their holder to purchase one Common Share at an exercise price of $3.45 per warrant share. The warrants are exercisable immediately upon their issuance date, January 21, 2026,

for a period of 5 years, until January 21, 2031. If the warrants are not exercised by their applicable expiry date, they will expire and be of no further force or effect. The warrants and the warrant shares may not be traded for a period of four

months, unless permitted under applicable securities legislation.

The Notes include customary limitations on conversion, including a beneficial ownership cap of 4.99% of the outstanding Common Shares following the conversion.

The Company’s authorized share capital as of March 31, 2026, consists of an unlimited number of Common shares without a par value of 6,223,323. The Common Shares confer upon their holders the right

to participate in the general meeting, with each Common Share carrying the right to one vote on all matters. The Common Shares also allow holders to receive dividends if declared and to participate in the distribution of surplus assets in the case of

liquidation of the Company.

OTHER SECURITIES

As of March 31, 2026, the Company also has the following outstanding securities that are convertible into, exercisable or exchangeable for, voting or equity securities of the Company: 28,269 Options,