IM Cannabis Corp.

Management’s Discussion and Analysis

For the

Three and Nine Months Ended September 30, 2021

November

15, 2021

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

IM Cannabis Corp.

Management’s Discussion and Analysis

For the Three and Nine Months Ended September 30, 2021 and

2020

This

Management’s Discussion and Analysis (“MD&A”)

reports on the consolidated financial condition and operating

results of IM Cannabis Corp. (the “Company” or

“IMCC”) for the three and nine months ended September

30, 2021 and 2020. Throughout this MD&A, unless otherwise

specified, references to “we”, “us”,

“our” or similar terms, as well as the

“Company” and “IMCC” refer to IM Cannabis

Corp., together with its subsidiaries, on a consolidated basis, and

the “Group” refers to the Company, its subsidiaries and

Focus Medical Herbs Ltd.

This

MD&A should be read in conjunction with the Company’s

interim condensed consolidated financial statements for the three

and nine months ended September 30, 2021 (the “Interim

Financial Statements”) and with the Company’s annual

financial statements as of December 31, 2020, and for the year then

ended and accompanying notes (“Annual Financial

Statements”).

The

Interim Financial Statements have been prepared by management in

accordance with the International Financial Reporting Standards

(“IFRS”) as issued by the International Accounting

Standards Board (“IASB”). IFRS requires management to

make certain judgments, estimates and assumptions that affect the

reported amount of assets and liabilities at the date of the

financial statements and the amount of revenue and expenses

incurred during the reporting period. The results of operations for

the periods reflected herein are not necessarily indicative of

results that may be expected for future periods.

The

Interim Financial Statements include the accounts of the Company,

and the following entities:

|

Legal Entity:

|

Relationship with the Company:

|

|

IMC

Holdings Ltd. (“IMC Holdings”)

|

Wholly-owned

subsidiary

|

|

Adjupharm

GmbH (“Adjupharm”)

|

Subsidiary

of IMC Holdings

|

|

IMC

Ventures Ltd.

|

Subsidiary

of IMC Holdings

|

|

I.M.C

Farms Israel Ltd.

|

Wholly-owned

subsidiary of IMC Holdings

|

|

I.M.C.

– International Medical Cannabis Portugal Unipessoal,

Lda.

|

Wholly-owned

subsidiary of IMC Holdings

|

|

Focus

Medical Herbs Ltd. (“Focus”)

|

Private

company over which IMC Holdings exercises “de facto

control” under IFRS 10, as further described under the

“Risk Factors” section below

|

|

R.A.

Yarok Pharm Ltd. (“Pharm Yarok”)

|

Private

company over which IMC Holdings exercises control under accounting

principles, as further described under the “Overview of the Company– The

Group and Consolidated Entities – The Consolidated

Entities” section below

|

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

|

Rosen

High Way Ltd. (“Rosen High Way”)

|

Private

company over which IMC Holdings exercises control under accounting

principles, as further described under the “Overview of the Company– The

Group and Consolidated Entities – The Consolidated

Entities” section below

|

|

High

Way Shinua Ltd. (“HW Shinua”)

|

Private

company over which IMC Holdings exercises control under accounting

principles, as further described under the “Overview of the Company– The

Group and Consolidated Entities – The Consolidated

Entities” section below

|

|

Revoly

Trading and Marketing Ltd. dba Vironna Pharm

(“Vironna”)

|

Private

company over which IMC Holdings exercises control under accounting

principles, as further described under the “Overview of the Company– The

Group and Consolidated Entities – The Consolidated

Entities” section below

|

|

Trichome

Financial Corp. (“Trichome”)

|

Wholly-owned

subsidiary

|

|

Trichome

Financial Cannabis GP Inc.

|

Wholly-owned

subsidiary of Trichome

|

|

Trichome

Financial Cannabis Manager Inc.

|

Wholly-owned

subsidiary of Trichome

|

|

Trichome

Financial Cannabis Private Credit LP (the

“Fund”)

|

Limited

partnership, equity accounted investee

|

|

Trichome

Asset Funding Corp.

|

Wholly-owned

subsidiary of Trichome

|

|

Trichome

JWC Acquisition Corp. (“TJAC”)

|

Wholly-owned

subsidiary of Trichome

|

|

Trichome

Retail Corp.

|

Wholly-owned

subsidiary of Trichome

|

|

MYM

Nutraceuticals Inc. (“MYM”)

|

Wholly-owned

subsidiary of Trichome

|

|

SublimeCulture

Inc.

|

Wholly-owned

subsidiary of MYM

|

|

CannaCanada

Inc.

|

Wholly-owned

subsidiary of MYM

|

|

MYM

International Brands Inc.

|

Wholly-owned

subsidiary of MYM

|

|

Highland

Grow Inc.

|

Wholly-owned

subsidiary of MYM International Brands Inc.

|

All

intercompany balances and transactions were eliminated on

consolidation.

All

amounts in this MD&A are expressed in Canadian Dollars ($) in

thousands, unless otherwise noted. Certain amounts are shown in New

Israeli Shekel (“NIS”), Euro (“€”),

United States Dollars (“US$”) as$”), in

thousands, unless otherwise noted.

CAUTION CONCERNING FORWARD-LOOKING STATEMENTS

Certain

statements in this MD&A may contain “forward-looking

statements” or “forward-looking information,”

within the meaning of applicable securities legislation

(collectively referred to herein as “forward-looking

statements” or “forward-looking information”).

All statements other than statements of fact may be deemed to be

forward-looking statements, including statements with regard to

expected financial performance, strategy and business conditions.

The words “believe”, “plan”,

“intend”, “estimate”, “expect”,

“anticipate”, “continue”, or

“potential”, and similar expressions, as well as future

or conditional verbs such as “will”,

“should”, “would”, and “could”

often identify forward-looking statements. These statements reflect

management’s current expectations and plans with respect to

future events and are based on information currently available to

management including based on reasonable assumptions, estimates,

internal and external analysis and opinions of management

considering its experience, perception of trends, current

conditions and expected developments as well as other factors that

management believes to be relevant as at the date such

statements are

made.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

Without

limitation, this MD&A contains forward-looking statements

pertaining to:

●

the Company’s

business objectives and milestones and the anticipated timing of

execution;

●

the performance of

the Company’s business and operations;

●

the intention to

expand the business, operations and potential activities of the

Company;

●

expectations

relating to the number of patients in Israel licensed by the

Israeli Ministry of Health (“MOH”) to consume medical

cannabis;

●

expectations of

Focus, TJAC and MYM on variations of net cost of sales based on the

number of pre-harvest plants, after harvest plants, the strains

being grown and technological progress in the trimming

machines;

●

the future product

portfolios of the Group and the Company’s ability to export

its products, strains and genetics from Canada to Israel and

Germany;

●

the competitive

conditions of the cannabis industry and the growth of medical or

recreational cannabis markets in the jurisdictions in which the

Company operates;

●

the growth of the

Company’s brands in the respective

jurisdictions;

●

the Company’s

retail presence, distribution capabilities and data-driven

insights;

●

cannabis licensing

in Israel, Germany and Canada, including the anticipated

decriminalization or legalization of recreational cannabis in

Israel;

●

expectations

regarding the renewal and/or extension of the Group’s

licenses;

●

the Group’s

anticipated operating cash requirements and future financing

needs;

●

the Group’s

expectations regarding its revenue, expenses, profit margins and

operations;

●

future

opportunities for the Company in Canada, particularly in the

premium and ultra-premium segments;

●

future

opportunities for the Company in Israel, particularly in the retail

and distribution segments of the cannabis market; and

●

contractual

obligations and commitments.

With

respect to the forward looking-statements contained in this

MD&A, the Company has made assumptions regarding, among other

things:

●

the anticipated

increase in demand for medical and recreational cannabis in the

markets in which the Company operates;

●

the Company’s

satisfaction of international demand for its products;

●

the effectiveness

of its products for medical cannabis patients and recreational

consumers;

●

future cannabis

pricing and input costs;

●

cannabis production

yields;

●

the Company being

able to continue to drive organic growth from Canadian operations;

and

●

the Company’s

ability to market its brands and services successfully to its

anticipated customers.

Readers

are cautioned that the above lists of forward-looking statements

and assumptions are not exhaustive. Since forward-looking

statements address future events and conditions, by their very

nature they involve inherent risks and uncertainties. Actual

results may differ materially from those currently anticipated or

implied by such forward-looking statements due to a number of

factors and risks. These include:

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

●

general business

risk and liability, including claims or complaints in the normal

course of business;

●

any failure of the

Company to maintain “de facto” control over Focus in

accordance with IFRS 10 Consolidated Financial Statements

(“IFRS 10”);

●

regulatory

authorities in Israel viewing the Company as the deemed owner of

more than 5% of Focus in contravention of Israeli

regulations;

●

limitations on

stockholdings of the Company in connection with its potential

direct engagement in the Israeli medical cannabis

market;

●

the ability and/or

need to obtain additional financing for continued

operations;

●

the lack of control

over the Company’s investees;

●

the failure of the

Company to comply with applicable regulatory requirements in a

highly regulated industry;

●

unexpected changes

in governmental policies and regulations affecting the production,

distribution, manufacture or use of medial cannabis in Israel,

Germany, Canada, Portugal, Greece, or any jurisdictions in which

the Company intends to operate;

●

the Company’s

ability to continue to meet the listing requirements of the

Canadian Securities Exchange (“CSE”) and the NASDAQ

Capital Market (“NASDAQ”);

●

the Israeli

government deciding to abandon the decriminalization or

legalization of recreational cannabis;

●

any change in the

political environment which would negatively affect the prospect of

decriminalization or legalization of recreational cannabis in

Israel;

●

any unexpected

failure of Focus to maintain in good standing or renew any of the

licenses granted by the Israeli Medical Cannabis Agency (the

“IMCA”), administered by the MOH, to propagate and

cultivate medical cannabis in Israel (the “Focus

Licenses”);

●

Focus’

reliance on the Focus Facility (as defined herein) to conduct

medical cannabis activities in Israel;

●

any unexpected

failure of Focus to maintain the Focus Facility in good standing

with all state and municipal Israeli regulations, including all

required licenses and permits and under the Focus

Leases;

●

any adverse outcome

of the Construction Proceedings (as defined herein);

●

any unexpected

failure of Adjupharm to maintain in good standing or renew any of

its wholesale, narcotics handling, manufacturing, procurement,

storage and distribution, or import/export licenses, permits,

certificates or approvals granted to Adjupharm by German regulatory

authorities (the “Adjupharm Licenses”);

●

any unexpected

failure of TJAC to maintain in good standing or renew any of the

Canadian licenses held by TJAC to produce, process, and sell

cannabis products in the adult-use recreational cannabis market

(the “TJAC Licenses”) or the Canadian licenses held by

MYM to cultivate, process, and sell cannabis products in the

adult-use recreational cannabis market (the “MYM

Licenses”);

●

the reliance by

TJAC and MYM on their facilities to conduct medical cannabis

activities;

●

any unexpected

failure of TJAC and/or MYM to maintain their facilities in good

standing with all applicable regulations, including all required

licenses and permits and under the TJAC Leases and the Sublime

Lease;

●

the Group’s

ability to maintain ancillary business licenses, permits and

approvals required to operate effectively;

●

the ability to

complete the Company’s acquisition of certain trading house

and in-house pharmacy assets from Panaxia Pharmaceutical Industries

Israel Ltd. and Panaxia Logistics Ltd., part of the Panaxia Labs

Israel, Ltd. group of companies (“Panaxia”) (the

“Panaxia Transaction”) in a timely manner or at all,

including (i) the receipt of requisite MOH approval in connection

with the transfer of Panaxia’s IMC-GDP license (the

“Panaxia IMC-GDP License”); (ii) any exercise of the

Company’s option (the “Panaxia Option”) to

acquire Panaxia’s pharmacy and its licenses to dispense and

sell medical cannabis to licensed medical cannabis patients (the

“Panaxia Pharmacy Licenses”); and (iii) the timing of

each instalment of the share consideration component of the Panaxia

Transaction purchase price (“Panaxia Consideration

Shares”);

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

●

the ability to

complete the acquisition of the outstanding ordinary shares of

Pharm Yarok, Rosen High Way and HW Shinua (Collectively, the

“Pharm Yarok Group”) (the “Pharm Yarok

Transaction”), including the receipt of MOH approval in

connection with the change of control under their respective

licenses of cannabis activity in Israel following the Pharm Yarok

Transaction;

●

the ability to

complete the acquisition of 51% of the outstanding ordinary shares

of Vironna (the “Vironna Transaction”), including the

receipt of MOH approval in connection with the change of control

under its licenses to dispense and sell medical cannabis to

licensed medical cannabis patients;

●

the ability of the

Company, following the Trichome Transaction, the MYM Transaction

(as defined herein), the Panaxia Transaction, the Pharm Yarok

Transaction and the Vironna Transaction to integrate each entity

into the Company’s operations and realize the anticipated

benefits and synergies of each such transaction and the timing

thereof and the focus of management on such

integration;

●

any potential

undisclosed liabilities of Trichome, MYM, Pharm Yarok, Vironna or

other entities acquired by the Company that were unidentified

during the due diligence process;

●

the interpretation

of Company’s acquisitions of companies or assets by tax

authorities or regulatory bodies, including but not limited to the

change of control of licensed entities;

●

the failure to

negotiate and execute a definitive agreement with cbdMD, Inc.

(“cbdMD”) satisfactory to the respective

parties;

●

the ability of the

Group to deliver on their sales commitments or growth

objectives;

●

the Group’s

reliance on third-party supply agreements and its ability to enter

into additional supply agreements to provide sufficient quantities

of medical cannabis to fulfil the Group’s

obligations;

●

the Group’s

possible exposure to liability, the perceived level of risk related

thereto, and the anticipated results of any litigation or other

similar disputes or legal proceedings involving the Group,

including but not limited to the Construction Proceedings, the MOH

Allegations (each as defined herein) and the class action

proceedings described herein;

●

the impact of

increasing competition;

●

any lack of merger

and acquisition opportunities;

●

inconsistent public

opinion and perception regarding the use of cannabis;

●

engaging in

activities considered illegal under US federal law related to

cannabis;

●

political

instability and conflict in the Middle East;

●

adverse market

conditions;

●

unexpected

disruptions to the operations and businesses of the Group as a

result of the COVID-19 global pandemic or other disease outbreaks

including a resurgence in the cases of COVID-19;

●

the inherent

uncertainty of production quantities, qualities and cost estimates

and the potential for unexpected costs and expenses;

●

the Group’s

ability to sell its products

●

any change in

accounting practices or treatment affecting the consolidation of

financial results;

●

reliance on

management; and

●

the loss of key

management and/or employees.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

Readers

are cautioned that the foregoing list of risk factors is not

exhaustive. Additional information on these and other factors that

could affect the business, operations or financial results of the

Company are detailed under the headings “Risks Factors”

and “Contingent Liabilities and Commitments” of this

MD&A. The Company and management caution readers not to place

undue reliance on any forward-looking statements, which speak only

as of the date made. Although the Company believes that the

expectations reflected in the forward-looking statements are

reasonable, it can give no assurance that such expectations will

prove to have been correct. The Company and management assume no

obligation to update or revise them to reflect new events or

circumstances except as required by applicable securities

laws.

FINANCIAL OUTLOOK

The

forward-looking information in this MD&A contain statements in

respect of estimated revenues. The Company and its management

believe that the estimated revenues are reasonable as of the date

hereof and are based on management’s current views,

strategies, expectations, assumptions and forecasts, and have been

calculated using accounting policies that are generally consistent

with the Company’s current accounting policies. These

estimates are considered financial outlooks under applicable

securities legislation. These estimates and any other financial

outlooks or future-oriented financial information included herein

have been approved by management of the Company as of the date

hereof. Such financial outlooks or future-oriented financial

information are provided for the purposes of presenting information

about management’s current expectations and goals relating to

the sales agreements described in the “Corporate

Developments” section of this MD&A and other previously

announced Focus sales agreements and the future business of the

Company. The Company disclaims any intention or obligation to

update or revise any future-oriented financial information, whether

as a result of new information, future events or otherwise, except

as required by securities legislation. Readers are cautioned that

actual results may vary materially as a result of a number of

risks, uncertainties, and other factors, many of which are beyond

the Group’s control. See the risks and uncertainties

discussed in the “Risk Factors” section and elsewhere

in this MD&A and other risks detailed from time to time in the

publicly filed disclosure documents of the Company which can be

viewed online under the Company’s profile on the System for

Electronic Document Analysis and Retrieval (“SEDAR”) at

www.sedar.com.

NON-IFRS FINANCIAL MEASURES

Certain

financial measures used in this MD&A do not have any

standardized meaning under IFRS, including “Gross

Margin”, “EBITDA” and “Adjusted

EBITDA”. For a reconciliation of these non-IFRS financial

measures to the most comparable IFRS financial measures, as

applicable, see the “Metrics and Non-IFRS Financial

Measures” section of the MD&A.

OVERVIEW

OF THE COMPANY

Company Background

The

Company was incorporated pursuant to the Business Corporations Act (British

Columbia) on March 7, 1980, under the name “Nirvana Oil &

Gas Ltd.” On July 12, 2013, in connection with a share

consolidation, the Company changed its name to “Navasota

Resources Inc.”. On June 22, 2018, the Company completed a

consolidation of its common shares (“Common Shares”) on

the basis of one post-consolidation Common Share for every five

pre-consolidation Common Shares. On October 4, 2019, in connection

with the Reverse Takeover Transaction (as defined below), the

Company effected a consolidation of its Common Shares on the basis

of one (1) post-consolidation Common Share for every 2.83

pre-consolidation Common Shares and changed its name to “IM

Cannabis Corp.”. On October 11, 2019, the Company completed

the Reverse Takeover Transaction and changed its business from

mining to the international medical cannabis industry.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

On

February 12, 2021, in connection with its NASDAQ listing

application, the Company effected a consolidation of its Common

Shares on the basis of one (1) post-consolidation Common Share for

every four (4) pre-consolidation Common Shares.

IMCC is

a multi-country operator in the medical and recreational cannabis

sector headquartered in Israel with operations in Israel, Europe,

and Canada.

Israel

In

Israel, IMC Holdings built the IMC brand of premium medical

cannabis products which have been cultivated over the last decade

by Focus, an Israeli licensed cultivator over which IMC Holdings

exercises “de facto control” under IFRS 10, and its

cultivation partners, and sold by Focus in the Israeli

market.

Focus

holds the Focus Licenses, granted by the MOH, to propagate and

cultivate medical cannabis in the State of Israel, valid until

January 3, 2022s. Focus is one of the eight medical cannabis

producers initially licensed by Israeli regulatory authorities and

has over 10 years of experience in growing high quality medical

cannabis products for the Israeli market.

As part

of its core Israeli business, IMC Holdings offers intellectual

property-related services to the medical cannabis industry based on

proprietary processes and technologies it developed for the

production of medical cannabis. The Company offers its intellectual

property and consulting services to Focus pursuant to certain

commercial agreements and receives as consideration for such

services a share of Focus’ revenues resulting from the sale

of medical cannabis products under the IMC brand. The Company has

started entering, through its subsidiaries, the distribution and

retail segments of the Israeli medical cannabis market, by entering

into each of the Panaxia Transaction, the Pharm Yarok Transaction,

and the Vironna Transaction and by attracting acquisitions of

synergistic targets in Israel. Following such vertical integration,

IMCC expects to increase its revenues from its Israeli medical

cannabis market activities, diversify its business opportunities

and gain direct access to medical cannabis patients.

Europe

In

Europe, IMCC operates through Adjupharm, a German-based subsidiary

acquired by IMC Holdings on March 15, 2019. Adjupharm is an EU-GMP

certified medical cannabis producer and distributor with the

Adjupharm Licenses that allow, among other capabilities, for the

import/export of medical cannabis with requisite permits. Adjupharm

serves as the Company’s flagship European outpost for sales

and distribution.

Adjupharm

currently manufactures and distributes IMC-branded medical cannabis

products, in addition to other branded medical cannabis products,

to pharmacies and distribution partners in Germany pursuant to

sales and distribution agreements. Adjupharm sources its medical

cannabis products from strategic partners, including various EU-GMP

standard European and Canadian suppliers. While the Company does

not currently distribute products in European countries other than

Germany, the Company intends to leverage the platform established

by Adjupharm in Germany and its network of distribution partners to

expand to other jurisdictions across the continent in which medical

cannabis is legal.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

Canada

IMCC

expanded operations to Canada through the acquisition of Trichome

on March 18, 2021 with the objective of securing premium indoor

cannabis for the Israeli medical market as well as to compete in

the premium segment of Canada’s adult-use recreational

market. Trichome’s wholly-owned subsidiary, TJAC holds the

TJAC Licenses. TJAC’s flagship facility, located near

Toronto, cultivates high-quality indoor cannabis using roughly

47,000 square feet of cultivation space. The Company intends to

operate Trichome with a focus on acquiring, integrating and

managing related assets in Canada that complement IMCC’s

international strategic objectives.

On July

9, 2021, IMCC, through Trichome, completed the acquisition of MYM

(the “MYM Transaction”). MYM is a Canadian cultivator,

processor, and distributor of premium cannabis through its two

wholly-owned subsidiaries: SublimeCulture Inc.

(“Sublime”), which is located near Montreal, Quebec,

and Highland Grow Inc. (“Highland”), which is in

Antigonish, Nova Scotia. MYM’s flagship brand, Highland, is

an ultra-premium brand sold in most provinces and territories

throughout Canada.

The

consolidated revenues of the Group for the three and nine months

ended September 30, 2021, was generated mainly from the sale of

medical cannabis products in Israel and Germany, and since March

18, 2021, the sale of adult-use recreational cannabis in Canada.

..

The

Group does not engage in any U.S. cannabis-related activities as

defined in Canadian Securities Administrators Staff Notice 51-352

(Revised) – Issuers with U.S. Marijuana-Related

Activities.

The Group and Consolidated Entities

The Group

As of

September 30, 2021, the Company’s major Israeli assets

include the Commercial Agreements and the Focus Agreement (as

defined herein), the respective definitive agreements with each of

the Consolidated Entities (as defined herein), as well as its

holdings in Xinteza API Ltd. (“Xinteza”).

As of

September 30, 2021, the Company’s major international assets

include Trichome, TJAC and MYM in Canada, and 90.02% of Adjupharm

in Germany.

As of

September 30, 2021, neither the Company nor any of its subsidiaries

currently hold, directly or indirectly, any licenses to engage in

the propagation, cultivation, production, processing, distribution

or sale of medical cannabis products in Israel as required by local

legislation. However, under IFRS 10, the Company is required to

consolidate the results of Focus, a licensed propagator and

cultivator of medical cannabis products under the current Israeli

regulatory regime. As such, all financial information in this

MD&A is presented on a consolidated basis reflecting the

results of the Group. While, as of the date of this report, IMCC

does not hold any of the Israeli licenses mentioned above and does

not own Focus, it derives a significant portion of its consolidated

revenues from Focus’ revenue, which is primarily earned from

sales of medical cannabis by Focus to pharmacies in Israel.

Furthermore, the Company has an option under the Focus Agreement

(as defined herein) to re-acquire 74% ownership of Focus. For more

information, please see the “Risk Factors” section

below.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

The Consolidated Entities

On July

28, 2021, IMC Holdings entered into a definitive agreement in

respect of the Pharm Yarok Transaction, whereby it will acquire all

of the outstanding ordinary shares of Pharm Yarok Group, subject to

MOH approval.

On

August 18, 2021, IMC Holdings entered into a definitive agreement

in respect of the Vironna Transaction, whereby it will acquire 51%

of the outstanding ordinary shares of Vironna, subject to MOH

approval.

Although

IMC Holdings has entered into definitive agreements in respect of

each of the Pharm Yarok Transaction and the Vironna Transaction, it

has not yet completed the foregoing acquisitions. As such, IMC

Holdings does not own any of Pharm Yarok Group or Vironna

(collectively, the “Consolidated Entities”) or their

respective licenses to conduct cannabis-related activities in

Israel. However, the respective definitive agreements with each of

the Consolidated Entities, provides the Company with the power to

unilaterally make all decisions regarding the financial and

operating policies of each of the Consolidated Entities and the

rights to obtain all related economic benefits. Accordingly, under

IFRS, the Company consolidates the financial results of the

Consolidated Entities in the Interim Financial Statements

commencing on the date of signing of each of the respective

definitive agreements and, accordingly, the relevant financial

information in this MD&A is presented on a consolidated basis

reflecting the results of the Group and the Consolidated Entities.

For more information, please see the “Risk Factors”

section below.

Company Products

Israel

‘IMC’

is a well-known medical cannabis brand in Israel. Leveraging its

long-term success in the Israeli market, the Company launched the

IMC brand in Germany in 2020. The Company believes that the IMC

brand has become synonymous with quality and consistency in the

Israeli medical cannabis market. In August 2020, a survey of

licensed medical cannabis patients showed that the IMC brand is one

of the top four most popular medical cannabis brands in

Israel.1

In

association with Focus, the Company maintains a brand portfolio

that includes popular medical cannabis dried flowers such as Roma,

DQ, London, and Tel Aviv, as well as full-spectrum cannabis

extracts.

All

Company products are tested in certified labs in accordance with

MOH standards and are certified before being packaged and labelled

with detailed information regarding the THC, CBD and CBN content of

each product.2

_____________

1 According to a survey carried out by Cannabis

Magazine among 519 patients licensed by the MOH to consume medical

cannabis (Aug 2020, Israel).

2 The actual percentages of THC and CBD content are

determined by certified laboratory inspections and disclosed on the

label of each IMC-branded medical cannabis product sold in Israel.

Depending on such THC and CBD content, each IMC-branded medical

cannabis product is labelled based on the following categories, in

accordance with MOH regulations: (a) ‘T20/C4’ (THC

16-24% and CBD 0-7%); (b) ‘T15/C3’ (THC 11-19% and CBD

0-5.5%); (c) ‘T10/C2’ (THC 6-14% and CBD 0-3.8%); (d)

‘T10/C10’ (THC 6-14% and CBD 6-14%); (e)

‘T5/C5’ (THC 1-9% and CBD 1-9%); (f)

‘T0/C24’ (THC 0-0.5% and CBD 20-28%); (g)

‘T1/C20’ (THC 0-2.5% and CBD 16-24%); (h)

‘T3/C15’ (THC 0.5-5.5% and CBD 11-19%); and (i)

‘T5/C10’ (THC 2.5-7.5% and CBD 6-14%). The stated THC

and CBD percentage ranges for the IMC branded strains are expected

ranges; the actual percentages, as labelled on product packaging

under the IMC brand may vary or deviate from such ranges. The CBN

content is lower than 1.5% in all products sold in

Israel.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

The

following graphic highlights key products sold under the IMC brand

in Israel:

Europe

In

Germany, the Company sells IMC-branded dried flower products. The

medical cannabis products sold in the German market are branded

generically as “IMC” so as to rely on the

Company’s brand recognition in establishing a foothold with

German healthcare professionals.

Canada

In

Canada, the Company’s product portfolio consists of dried

flowers, pre-rolled cannabis, pressed hash, and kief offerings sold

by TJAC under the WAGNERS brand into the Canadian adult-use

recreational cannabis market (rebranded from ‘JWC’ to

‘WAGNERS’ in May 2021). The WAGNERS brand competes in

the premium segment of the market. Dried flower is sold primarily

in 3.5 gram, 7 gram and 28 gram formats, pre-rolls are sold in a 3

x 0.5 gram format, and both hash and kief are sold in 1, 2 and 4

gram formats. Historically, TJAC sold cannabis on a

business-to-business basis to other Canadian licensed cannabis

producers. Recently, TJAC has shifted its focus to higher margin

business-to-consumer sales. With the acquisition of MYM, TJAC

expects to optimize the cultivation and brand footprint of both

WAGNERS and Highland Grow. IMCC intends to export premium cannabis

strains from TJAC and MYM as well as selected genetics from their

ultra-premium strains to the Israeli market for further fulfillment

of its global cultivation and distribution platform.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

The

following graphic highlights key products sold under the WAGNERS

brand:

On July

9, 2021, the Company closed the MYM Transaction. Through this

acquisition, the Company acquired the rights to the Highland Grow

brand, a well-known, widely-available ultra-premium cannabis brand

in Canada. Highland Grow products include dried flower and

pre-rolled cannabis, with dried flower potency typically above 25%

THC. In addition to the proven track record of the Highland Grow

brand, MYM holds over 150 strains in its product portfolio that the

Company plans to selectively release to market.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

The

following graphic highlights key products sold under the Highland

Grow brand:

Corporate

Developments

(i) the

Reverse Takeover Transaction and Liquidity Events

On

October 11, 2019, the Company completed a business combination with

IMC Holdings resulting in a reverse takeover of the Company by

shareholders of IMC Holdings (the “Reverse Takeover

Transaction”). The Reverse Takeover Transaction was effected

by way of a “triangular merger” between the Company,

IMC Holdings and a wholly-owned subsidiary of the Company pursuant

to Israeli statutory law.

In

connection with the Reverse Takeover Transaction, the Company

completed a private placement offering of 19,460,527 (on a

pre-Share Consolidation (as defined below) basis) subscription

receipts (each a “Subscription Receipt”) of a

wholly-owned subsidiary of the Company (“Finco”) at a

price of $1.05 per Subscription Receipt for aggregate gross

proceeds of $20,433 (the “Financing”). Upon the

satisfaction or waiver of, among other things, all of the condition

precedents to the completion of the Reverse Takeover Transaction,

each Subscription Receipt was exchanged for one unit of Finco (a

“Finco Unit”) with each Finco Unit being comprised of

one (1) common share of Finco (a “Finco Share”) and

one-half of one (1/2) Finco Share purchase warrant (each whole

warrant, a “Finco Warrant”). Each whole Finco Warrant

was exercisable for one Finco Share at an exercise price of $1.30

until October 11, 2021. Upon closing of the Reverse Takeover

Transaction, the Finco Shares and Finco Warrants were exchanged on

a 1:1 basis for Common Shares and Common Share purchase warrants

(“Listed Warrants”) on economically equivalent terms. A

total of 9,730,258 Listed Warrants were issued and listed for

trading on the CSE under the ticker “IMCC.WT”. The

Listed Warrants expired on October 11, 2021.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

In

connection with the Financing, IMC Holdings granted to the agents

who acted on its behalf, options to acquire 1,199,326 compensation

units (the “2019 Compensation Units”) at an exercise

price of $1.05 per 2019 Compensation Unit. Upon completion of the

Reverse Takeover Transaction, the 2019 Compensation Units were

exchanged for compensation options of the Company (the “2019

Compensation Options”). Each 2019 Compensation Option

consists of one (1) Common Share and one-half of one (1/2) Common

Share purchase warrant (the “Unlisted Warrants” and

together with the Listed Warrants, the “Warrants”) with

each whole Unlisted Warrant exercisable for one (1) Common Share at

an exercise price of $1.30 until August 30, 2022, with such

Unlisted Warrants issued as a result of exercises of 2019

Compensation Options and not listed for trading on any

exchanges.

Upon

the completion of the Reverse Takeover Transaction, the former

holders of IMC Holdings held approximately 84.28% of the issued and

outstanding Common Shares and the previous holders of Subscription

Receipts held approximately 13.35% of the Common Shares, in each

case, on a non-diluted basis.

On

November 5, 2019, the Common Shares began trading on the CSE under

the ticker symbol “IMCC”.

On

February 12, 2021, the Company’s shareholders approved at a

special meeting the consolidation of all the Company’s issued

and outstanding Common Shares on a four (4) to one (1) basis (the

“Share Consolidation”). Following the Share

Consolidation, the number of Listed Warrants, Unlisted Warrants,

and 2019 Compensation Options outstanding was not altered; however,

the exercise terms were adjusted such that four Listed Warrants

were required to be exercised to purchase one Common Share

following at an adjusted exercise price of $5.20, four (4) Unlisted

Warrants are required to be exercised to purchase one (1) Common

Share at an adjusted exercise price of $5.20, and four 2019

Compensation Options are required to be exercised to purchase one

(1) unit at an adjusted exercise price of $4.20, with each unit

exercisable into one (1) Common Share and one-half of one (1/2)

Unlisted Warrant, with each whole Unlisted Warrant expiring on

August 30, 2022 and exercisable to purchase one (1) Common Share at

an exercise price of $5.20. The consolidated financial statements

give effect to the Share Consolidation for all periods

presented.

On

March 1, 2021, the Common Shares commenced trading on NASDAQ under

the ticker symbol “IMCC”, making the Company the first

Israeli medical cannabis operator to list its shares on

NASDAQ.

As of

September 30, 2021, and 2020, there were 7,362,762 and 9,729,735

Listed Warrants outstanding, respectively, re-measured by the

Company, according to their trading price in the market, in the

amount of $74 and $2,432, respectively. For the nine months ended

September 30, 2021 and 2020, the Company recognized a revaluation

gain (loss) of $15,856 and $(2,432), respectively. For the three

months ended September 30, 2021 and 2020, the Company recognized a

revaluation gain (loss) of $3,154 and $(973) in the consolidated

statement of profit or loss and other comprehensive income, in

which the unrealized gain is included in finance income

(expense).

As of

September 30, 2021, and 2020, there were 3,043,478 and nil Unlisted

Warrants outstanding, respectively, re-measured by the Company,

using the Black-Scholes pricing model, in the amount of $6,451 and

$nil, respectively. For the nine months ended September 30, 2021

and 2020, the Company recognized a revaluation gain (loss) of

$5,381 and $nil, respectively. For the three months ended September

30, 2021 and 2020, the Company recognized a revaluation gain (loss)

of $4,965 and $nil in the consolidated statement of profit or loss

and other comprehensive income, in which the unrealized gain is

included in finance income (expense).

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

During

the nine months ended September 30, 2021, a total of 2,366,496

Listed Warrants were exercised for 591,624 Common Shares at an

adjusted exercise price of $5.20 per Common Share. As a

result, the Company received a total amount of $3,075.

During

the nine months ended September 30, 2021, a total of 194,992

Unlisted Warrants were exercised for 48,748 Common Shares at an

adjusted exercise price of $5.20 per Common Share. As a

result, the Company received a total amount of $255.

During

the nine months ended September 30, 2021, a total of 197,632 2019

Compensation Options were exercised for 49,408 Common Shares and

24,703 Unlisted Warrants. Consequently, the Company received an

aggregate adjusted exercise amount of $208.

(ii) Restructuring

Current

Israeli law requires prior approval by the IMCA, a unit of the MOH,

of the identity of any shareholder owning 5% or more of an Israeli

company licensed by the IMCA to engage in cannabis-related

activities in Israel. For a number of reasons, including the

opportunity to leverage a network of multiple Israeli licensed

producers cultivating under the IMC brand, and in contemplation of

a “go-public transaction” to geographically diversify

the Company’s share ownership, IMC Holdings restructured its

organization on April 2, 2019 (the “IMC Restructuring”)

resulting in the divestiture to Oren Shuster and Rafael Gabay of

its interest in Focus, which is licensed by the IMCA to propagate

and cultivate medical cannabis in Israel.

IMC

Holdings retains an option with Messrs. Shuster and Gabay to

re-acquire the sold interest in Focus at its sole discretion and in

accordance with Israeli cannabis regulations, within 10 years of

the date of the IMC Restructuring (the “Focus

Agreement”). The Focus Agreement sets an aggregate exercise

price equal to NIS 765.67 per share of Focus for a total

consideration of NIS 2,756,500, that being equal to the price

paid by Messrs. Shuster and Gabay for the acquired interests in

Focus at the time of the IMC Restructuring.

As part

of the IMC Restructuring, IMC Holdings and Focus entered into an

agreement in which Focus shall use the IMC brand on an exclusive

basis for the sale of any cannabis plant and/or cannabis product

produced by Focus, either alone or together with other

sub-contractors engaged by Focus (the “IP Agreement”).

Focus is also obligated to exclusively use IMC Holdings for certain

management and consulting services including: (a) business

development services; (b) marketing services;

(c) strategic advisory services; (d) locating potential

collaborations on a worldwide basis; and (e) financial

analysis services (the “Services Agreement” and

collectively with the IP Agreement, the “Commercial

Agreements”).

Under

the IP Agreement, IMC Holdings charges Focus an amount equal to 25%

of its revenues on a quarterly basis, which shall not be changed

without the consent of IMC Holdings, as consideration for

Focus’ use of certain trademarks, know-how, technology and

maintenance services provided by IMC Holdings.

Under

the Services Agreement, IMC Holdings charges Focus an amount equal

to IMC Holdings’ cost of providing certain services to Focus

plus a 25% mark-up, which shall not be changed without the consent

of IMC Holdings, as consideration for the provision of such

services.

Subsequent

to the IMC Restructuring, according to accounting criteria in IFRS

10, the Company is still viewed as effectively exercising control

over Focus, and therefore, the accounts of Focus continue to be

consolidated with those of the Company.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

As a

result of the IMC Restructuring, IMCC derives revenue from the

Commercial Agreements. IMCC does not directly hold any licenses to

engage in the cultivation, production, processing, distribution or

sale of medical cannabis in Israel.

(iii) Regulatory

Changes in Israel

Changes under the MOH Regulations

Until

September 2019, patients licensed for consumption of medical

cannabis products by the IMCA received all of their medical

cannabis products authorized under their respective licenses at a

fixed monthly price of NIS 370, regardless of each

patient’s authorized amount. As an example, a patient who was

to receive 20 grams of medical cannabis products per month would

pay the same monthly fee of NIS 370 as a patient who received

180 grams per month. In addition, IMCA assigned patients to a

particular licensed medical cannabis producer, from which each

patient would exclusively receive their medical cannabis products.

Under the previous medical cannabis regulations, Focus distributed

approximately 80% of its medical cannabis products via home

delivery and the remaining 20% via an IMCA-established distribution

outlet.

Under

the MOH’s new regulations, medical cannabis products are

delivered from a licensed producer to a manufacturer, which then

delivers to a distributor to distribute to pharmacies. In addition,

patients licensed for consumption of medical cannabis products are

no longer exclusively assigned to medical cannabis producers and

may purchase medical cannabis products from authorized pharmacies

at a range of price points without any MOH-regulated price

controls.

In

light of the MOH’s new regulations, some medical cannabis

patient licenses granted under the previous regime are still valid.

The medical cannabis patient licenses set to expire during the

period from February 1, 2019 to July 31, 2019 were extended by

order of the Israeli Supreme Court until further notice by the

Court. While these licenses remain valid, the patients who hold

these licenses are entitled to receive medical cannabis products

pursuant to the price controls and supplier restrictions of the

former regime. Additional information on the proceedings pursuant

to which the above-referenced order was granted can be found under

“Legal Proceedings and Regulatory Actions – Legal

Proceedings – Supreme Court of Justice

2335/19”.

Following

the implementation of the above MOH’s new regulations, the

Group believes that the Israeli medical cannabis market will

continue to benefit from price stability of the premium and super

premium medical cannabis products, an increase to the number of

physicians certified by the IMCA to prescribe medical cannabis and

thus, an increase in the number of licensed medical cannabis

patients.

Medical Cannabis Imports

In

October 2020, the IMCA issued an updated procedure, titled

“Guidelines for Approval of Applications for Importation of

Dangerous Drug of Cannabis Type for Medical Use and for

Research” (“Procedure 109”), describing the

application requirements for cannabis import licenses for medical

and research purposes. According to Procedure 109, the following

permits and licenses are required to receive a cannabis import

license: (1) License to possess medical cannabis and operate

in the medical cannabis industry; (2) License to import plant

material; (3) Permit to import narcotic drugs; and

(4) License to import a dangerous drug.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

Medical Cannabis Exports

In

October 2020, the MOH launched a new pilot program under which

medical cannabis producers would be authorized to export medical

cannabis products, subject to the requirement that certain products

be made available at a fixed price of NIS 14 per gram to

patients in Israel over the age of 21 and NIS 10 per gram to

patients under the age of 21 (the “Pilot Program”).

Products bearing the IMC brand were offered as part of the Pilot

Program during the first and second quarter of 2021. The Pilot

Program expired at the end of Q1 2021 and was not extended by the

MOH.

In

December 2020, the IMCA published guidelines for the medical

cannabis export permit application process,3 pursuant to which an

export permit will only be granted to an applicant if

(i) sufficient domestic supply has been secured by such

applicant in the variety and quantity that will meet the Israeli

level of demand; (ii) the delivery of medical cannabis is made

from approved sites; (iii) the applicant has a valid IMC-GDP

certification and business license from the IMCA; and (iv) an

import permit from the importing country is obtained and attached

to the export application.

Legalization of Adult-Use Recreational Cannabis in

Israel

As of

the date of this MD&A, adult-use recreational cannabis use in

Israel is illegal. In November 2020, an Israeli government

committee responsible for advancing the cannabis market reform

published a report supporting and recommending the legalization of

adult-use recreational cannabis in Israel (the

“Report”). Based on the Report, the Israeli Ministry of

Justice was expected to formulate a bill to begin the legislative

process towards the legalization of adult-use recreational

cannabis. The government committee made its recommendation for

legalization based on the increasing demand for adult-use

recreational cannabis in Israel, the importance of maintaining

quality standards and limiting uncontrolled products, the need for

increased access to cannabis by medical patients and the objective

of decreasing the size of the illegal market. The model proposed by

the government committee in the Report is similar in nature to the

model adopted in Canada, whereby the sale of adult-use recreational

cannabis would be channeled through government-licensed

dispensaries.

In

December 2020, the governing Israeli parliament dissolved and the

then-existing draft bill regarding the proposed legalization of

adult-use recreational cannabis became defunct. However, the new

government, formed on June 13, 2021, declared and settled in the

coalition agreement, its commitment to legalization of adult-use

recreational cannabis. Since the formation of the new government,

several legislative initiatives were filed, including for the

decriminalization of the possession of cannabis for individual

recreational adult-use and the legalization of CBD for non-medical

use. These initiatives were not accepted, however they are viewed

as first steps towards more comprehensive legislation towards the

legalization of adult-use recreational cannabis. Members of the

Israeli government continue to affirm their commitment to the

legalization of adult-use recreational cannabis.

(iv) Israeli

Market

The

Israeli medical cannabis market has shown dramatic growth over the

past several years. It is projected that this growth will continue

and according to MOH estimates, the number of patients in Israel

licensed by the MOH to consume medical cannabis is expected to

reach approximately 120,000 by the end of 2021.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

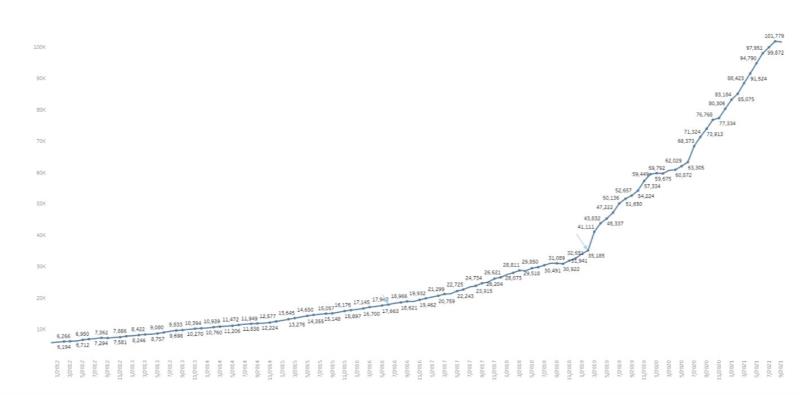

Israeli Market Development 2011-2021

According

to MOH monthly publication, as of September 2021, there are 101,779

licensed patients in Israel, and a monthly prescription of

3,861,000 and 2,848,000 grams of cannabis were recorded in

September 2021 and December 2020, respectively.3

The

below reflects the number of licensed medical cannabis patients in

Israel over the year 2011 to September 2021:4

(v) Canadian

Market

On

October 17, 2018, the Cannabis

Act came into effect in Canada, regulating both medical and

recreational cannabis. Under this legislation, cannabis cultivators

and processors are licenced by Health Canada to cultivate, produce

or sell cannabis products for medical and recreational consumption.

Retail activities in the Canadian cannabis industry are licensed by

the relevant provincial or territorial government. Consumers do not

require a licence to purchase cannabis. In 2020, roughly 27% of

Canadians surveyed by Statistics Canada had consumed cannabis in

the past 12 months.5 From October 2018 to

August 2021, sales of legal recreational cannabis increased by

roughly 750%, to nearly $360,000,000 per month, and 20% from March

2021 to August 2021 alone.6 While the Canadian

market remains in its infancy, growth has been significant, due

partially to the increasing availability of retail cannabis stores.

As of October 2021, there were an estimated 2,500 cannabis stores

in Canada.7

________________

4 Ministry of Health – licensed

patients’ data as of September 2021 - https://www.health.gov.il/Subjects/cannabis/Documents/licenses-status-September-2021.pdf

5 Canadian Cannabis Survey 2020:

Summary. https://www.canada.ca/en/health-canada/services/drugs-medication/cannabis/research-data/canadian-cannabis-survey-2020-summary.html#a2

6 Retail trade sales by province and

territory. https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=2010000801&pickMembers%5B0%5D=2.30&pickMembers%5B1%5D=3.1&cubeTimeFrame.startMonth=10&cubeTimeFrame.startYear=2018&cubeTimeFrame.endMonth=12&cubeTimeFrame.endYear=2021&referencePeriods=20181001%2C20211201

7 Looking back from 2020, how

cannabis use and related behaviours changed in Canada.

https://www.cannabisbenchmarks.com/report-category/Canada/

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

(vi) European

Activity and the German Market

The

Company’s European strategy is centered in Germany, whose

medical cannabis market is currently considered the largest in

Europe.8

To develop its operations in Germany, on March 15, 2019, IMC

Holdings acquired 100% of the outstanding shares of Adjupharm (the

“Adjupharm Shares”), a licensed EU-GMP certified

medical cannabis producer and distributor, for approximately $1,400

(€924 as of the acquisition date) with additional obligations

to the sellers including repayment of bank loans of up to $1,030

(€680 as of the acquisition date). These bank loans were

repaid by IMC Holdings in May 2019. The Company, through IMC

Holdings, currently owns 90.02% of Adjupharm, with the balance

owned by Adjupharm’s Chief Executive Officer.

The

Company continues to develop Adjupharm as its European hub and to

expand its presence in the German market by forging partnerships

with pharmacies and distributors across the country. The

Company’s objective is to capture a significant market share

in Germany by working directly with pharmacies and with

distributors to increase market reach for products bearing the IMC

brand. The Company currently has approximately 8,000 square feet of

warehousing and GMP Standard production capacity in Germany,

following the recent completion of an expansion process of its

facility to a new, state-of-the-art logistics centre, upgrading its

production technology and increasing its storage capacity to seven

tons of cannabis.

Adjupharm

sources its supply of medical cannabis for the German market from

various EU-GMP standard European and Canadian suppliers, and is

actively seeking additional supply partners to diversify its source

of supply of premium and super premium cannabis products and

minimize the risks inherent in the supply chain.

Adjupharm

relies on its sales and distribution agreements to supply and

distribute IMC-branded products to distribution partners or

directly to German pharmacies. There are approximately 19,000

community pharmacies in Germany, each of which is permitted to

create and dispense medications, including medical cannabis,

pursuant to physician prescriptions.9 In the first quarter

of 2021, Adjupharm completed the expansion of its internal and

external sales department and is focused on increasing physician

awareness and engagement to drive sales of IMC-branded medical

cannabis products. In July 2021, Adjupharm was recognized by the

German Brand Institute with the “German Brand Award

2021”, recognizing its excellence in brand strategy and

creation, communication and integrated marketing. The competitive

advantage in Germany also lies in the Group’s track record

and brand reputation in Israel and proprietary data supporting the

effectiveness of medical cannabis for the treatment of a variety of

conditions.

The

Company has also engaged in exploratory operations to expand to

Portugal and Greece, by establishing a wholly-owned subsidiary in

Portugal in October 2018, and a joint venture in Greece (25% owned

by IMCC), however it has deferred any further investment in these

jurisdictions indefinitely in light of the uncertainty related to

COVID-19.

_______________

8 Health Europa, June 23, 2020. https://www.healtheuropa.eu/exploring-growth-in-the-european-medical-cannabis-market/100849/

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

Due to

the impact of the COVID-19 pandemic on Germany in the first quarter

of 2021, the Company, through Adjupharm, leveraged its established

distribution platform to enter into several reseller agreements of

COVID-19 antigen test kits. Such engagement of Adjupharm facilitate

and further enhance its business relationship with pharmacies in

Germany and support its distribution platform for medical cannabis.

Due to the evolving impact of COVID-19 worldwide, and in light of

the uncertainty related to the demand for COVID-19 test kits in

Germany, the Company is examining the potential demand for such

test kits in Israel. For more information, please see “Strategic

Developments”.

(vii) Investment

in Xinteza

On

December 26, 2019, IMC Holdings entered into a share purchase

agreement with Xinteza, a company with a unique biosynthesis

technology, whereby the Company acquired, on an as-converted and

fully diluted basis, 25.37% of Xinteza’s outstanding share

capital, for consideration of US$1,700 (approximately $2,300 as of

September 30, 2021) paid in several installments (the

“Xinteza SPA”). As of September 30, 2021, the Company

has paid all outstanding installments pertaining to the Xinteza SPA

and currently holds 23.35% of the outstanding share capital of

Xinteza on an as-converted and fully diluted basis.

Under

an exclusive license from Yeda Research & Development Company

Ltd., the commercial division of the Weizmann Institute of Science,

and based on disruptive plant genetics and metabolomics research

led by Professor Asaph Aharoni, Xinteza has been developing

advanced proprietary technologies relating to the production of

cannabinoid-based active pharmaceutical ingredients for the

pharmaceutical and food industries using biosynthesis and

bio-extraction technologies.

(viii) Strategic

Developments:

1.

On July 9, 2021,

the Company closed the MYM Transaction, implemented in accordance

with the terms and conditions of the arrangement agreement dated

March 31, 2021, between IMCC, MYM and Trichome, which resulted in

the acquisition by IMCC of all of the issued and outstanding shares

of MYM (the “MYM Shares”) in exchange for 0.022 of a

Common Share for each MYM Share. In connection with the MYM

Transaction, a total of 10,073,437 Common Shares have been issued

to the former holders of MYM Shares, resulting in former MYM

shareholders holding approximately 15% of the total number of

Common Shares at the time of issuance (based on 67,156,470 Common

Shares issued and outstanding immediately after

closing).

2.

On July 28, 2021,

IMC Holdings entered into a definitive agreement in respect of the

Pharm Yarok Transaction. The aggregate consideration for the Pharm

Yarok Transaction is NIS 11,900 (approximately $4,600), of which

NIS 3,500 (approximately $1,300) shall be invested in the Company

at closing by the shareholders of Pharm Yarok Group in exchange for

Common Shares. Closing of the Pharm Yarok Transaction is

conditional upon receipt of all requisite approvals, including from

the MOH. Pharm Yarok is a leading medical cannabis pharmacy and

trade company located in central Israel; Rosen High Way is a trade

and distribution centre providing medical cannabis storage,

distribution services and logistics solutions for cannabis

companies and pharmacies in Israel; and HW Shinua is an applicant

for a medical cannabis transportation license from the IMCA, the

receipt of which would permit HW Shinua to transport large

quantities of medical cannabis to and from Pharm Yarok’s

pharmacy and Rosen High Way’s distribution centre and to and

from third parties in the medical cannabis sector, including

medical cannabis growing facilities, pharmacies, manufacturers and

distribution centres across Israel.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

3.

On July 30, 2021,

in connection with the Panaxia Transaction, the Company issued the

first installment of 142,007 Panaxia Consideration Shares at a

price of US$5.009 (approximately $6.24) per Panaxia Consideration

Share, representing an aggregate value equal to approximately

US$711 (approximately $889), with up to four additional

installments to follow. The issue price of the Panaxia

Consideration Shares was calculated based on the average closing

price of the Common Shares on NASDAQ over the 10 trading day period

immediately preceding July 30, 2021.

4.

On August 3, 2021,

IMC Holdings and cbdMD executed a binding letter of intent that

will grant IMC Holdings an exclusive right to import, sell,

distribute and market cbdMD products in Israel using the cbdMD

brand name and trademark, subject to the legalization of

hemp-derived CBD for non-medical purposes in Israel.

5.

On August 16, 2021,

IMC Holdings entered into definitive agreement with Vironna in

connection with the Vironna Transaction to acquire 51% of the

issued and outstanding ordinary shares of Vironna for aggregate

consideration of NIS 8,500 (approximately $3,300), comprised of NIS

5,000 (approximately $1,950) in cash and NIS 3,500 (approximately

$1,350) in Common Shares to be issued at closing date (the

“Vironna Share Consideration”). Closing of the Vironna

Transaction is conditional upon receipt of all requisite approvals,

including from the MOH. To satisfy the Vironna Share Consideration,

the Company will issue number of Common Shares calculated based on

the average closing price of the Common Share on NASDAQ over the 14

trading day period immediately preceding the date of issuance.

Vironna is a leading pharmacy licensed to dispense and sell medical

cannabis to licensed medical cannabis patients, located in central

Israel and is one of the leading pharmacies serving patients among

the Arab population in Israel.

6.

On August 19, 2021,

Focus Medical Herbs Ltd., issued its first purchase order for

approximately 220 kilograms of medical cannabis purchased from The

Flowr Corporation (“Flowr”), under a three-year supply

agreement entered into by Focus and Flowr on June 24, 2021. This

order is expected to be exported to Israel in Q4 2021, subject to

the satisfaction of applicable regulatory and import requirements.

Flowr is a Canadian licensed producer of ultra-premium adult-use

recreational and medical cannabis products.

7.

On September 1,

2021, the Issuer issued the second instalment of 246,007 Panaxia

Consideration Shares at a price of US$3.68 (approximately $4.64)

per Panaxia Consideration Share, representing an aggregate value of

US$905 (approximately $1,141). The issue price of the Panaxia

Consideration Shares was calculated based on the average closing

price of the Common Shares on NASDAQ over the 10 trading day period

immediately preceding September 1, 2021.

8.

On September 17,

2021, Adjupharm signed a five-year exclusive supply agreement for

the German market with Zelira Therapeutics Ltd.

(“Zelira”). Pursuant to the agreement, Adjupharm will

distribute Zelira’s Zenivol product in Germany. Zenivol is a

proprietary cannabinoid-based medicinal product for treatment of

chronic insomnia, supported by clinical data.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

9.

On September 23,

2021, TJAC increased the limit on the revolving credit facility

entered into with a private Canadian creditor on May 17, 2021 (the

“Facility”) from $5,000 to $7,500. The increase will be

used to finance TJAC’s receivables in order to manage the

timing of its cash flows. The revised commitment from the private

Canadian creditor is $7,500, with an initial term of 12 months that

can be extended upon the mutual agreement of both parties. Per

annum interest is equal to the greater of (i) 9.75% and, (ii) the

Toronto Dominion Bank prime rate, plus 7.30%. The Facility has a

standby fee of 2.40% per annum, which is charged against the unused

portion. Advanced amounts are secured against the assets of TJAC

and Trichome, with Trichome providing a guarantee for the

Facility. To maintain

the Facility, TJAC must abide by certain financial covenants, such

as the maintenance of a tangible net worth greater than $5 million

and a debt service coverage ratio of 2:1.

Subsequent Events

1.

On October 15,

2021, the Issuer issued the third instalment of 248,212 Panaxia

Consideration Shares at a price of US$3.225 (approximately $4.01)

per Panaxia Consideration Share, representing an aggregate value

equal to US$800 (approximately $996). The issue price of the

Panaxia Consideration Shares was calculated based on the average

closing price of the Common Shares on NASDAQ over the 10-trading

day period immediately preceding October 1, 2021.

Company Outlook

Israel

In

Israel, the Company, through the Commercial Agreements, continues

to expand the IMC brand recognition, and, in association with

Focus, supply the growing Israeli medical cannabis market with

products bearing the IMC brand. With the expected high growth of

the Israeli medical cannabis market, the Company is well positioned

to benefit from its long-term presence and strong brand

recognition, expecting a continued increase in revenues and

profitability. In addition, the Company intends to enter, through

its subsidiaries, additional segments of the medical cannabis

market in Israel, including the distribution and retail segments,

by completing the Panaxia Transaction, the Pharm Yarok Transaction,

and the Vironna Transaction. Following the completion of the

foregoing transactions, the Company expects vertical integration to

increase its revenue and margins from its Israeli medical cannabis

market activities, diversify its business opportunities and gain

direct access to medical cannabis patients to benefit from market

knowledge and trends. Furthermore, the Group is focused on

diversifying its product portfolio with premium and super premium

medical cannabis products, leveraging its Canadian cultivation

facilities that are expected to provide additional opportunities to

export premium cannabis products to Israel and

Germany.

Europe

The

Company’s objective within Europe is to capitalize on the

increasing demand for medical cannabis products and to bring the

well-established IMC brand and its product portfolio to European

patients. The Company’s operating track record, accumulation

of data and brand reputation in Israel is a competitive advantage

in gaining traction within the German and European markets and

building support among physicians who prescribe medical cannabis

products.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

Canada

Following

the successful completion of the acquisition of Trichome on March

18, 2021 (the “Trichome Transaction”) and the MYM

Transaction on July 9, 2021, IMCC plans to integrate and manage its

assets in Canada with a goal of maximizing Company-wide revenue and

margins.

Additionally,

the Company will continue to drive organic growth from Canadian

operations through active portfolio management of its products,

additional SKU launches, boosting cultivation efficiency, and

adding to the number of points of distribution across the country.

The Company expects to continue to drive meaningful revenue growth

in the near-term by diversifying its product portfolio under the

WAGNERS and Highland Grow brands, including the introduction of new

dried flower, pre-rolled, and hash SKUs in key Canadian

markets.

Overview of Financial Performance

|

|

For the nine

months ended

September

30,

|

For the three months ended

September 30,

|

For the Year ended December 31,

|

|

|

|

|

|

|

|

|

Net

Revenues

|

$34,272

|

$10,990

|

$14,393

|

$5,893

|

$15,890

|

|

Gross profit before

fair value impacts in cost of sales

|

$8,109

|

$6,018

|

$2,880

|

$3,362

|

$8,809

|

|

Gross margin before

fair value impacts in cost of sales (%)

|

24%

|

55%

|

20%

|

57%

|

55%

|

|

Operating

Loss

|

$(26,667)

|

$(1,862)

|

$(14,245)

|

$(671)

|

$(8,245)

|

|

Loss

|

$(6,030)

|

$(8,758)

|

$(5,656)

|

$738

|

$(28,734)

|

|

Loss per share

attributable to equity holders of the Company - Basic

|

$(0.10)

|

$(0.06 (

|

$(0.06 (

|

$0.004

|

$(0.74)

|

|

Loss per share

attributable to equity holders of the Company - Diluted (in

CAD)

|

$(0.51)

|

$(0.06 (

|

$(0.18 (

|

$0.004

|

$(0.74)

|

The

Overview of Financial Performance includes reference to

“gross margin”, which is a non-IFRS financial measure.

Non-IFRS measures are not recognized measures under IFRS, do not

have a standardized meaning prescribed by IFRS and are therefore

unlikely to be comparable to similar measures presented by other

companies. The Company defines gross margin as the difference

between revenue and cost of revenues divided by revenue (expressed

as a percentage), prior to the effect of a fair value adjustment

for inventory and biological assets.

IM

Cannabis Corp.

Management’s Discussion and Analysis (Canadian dollars, in

thousands)

Operational Results - Medical Cannabis

|

|

For the Nine

Months Ended

September

30,

|

For the Three months ended

September 30,

|

For the Year ended December 31,

|

|

|

|

|

|

|

|

|

Average net selling

price of dried flower (per Gram)

|

$4.56

|

$5.50

|

$4.85

|

$5.49

|

$5.75

|

|

Average net selling

price of other cannabis products (per Gram)1